After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: A guiding hand to 2023’s ad-supported models

Wednesday

With the likes of Netflix and Disney+ adopting ad-supported tiers, Omdia’s Adam Thomas sets out some key recommendations to help media and entertainment companies make the most of their new business models in the coming year

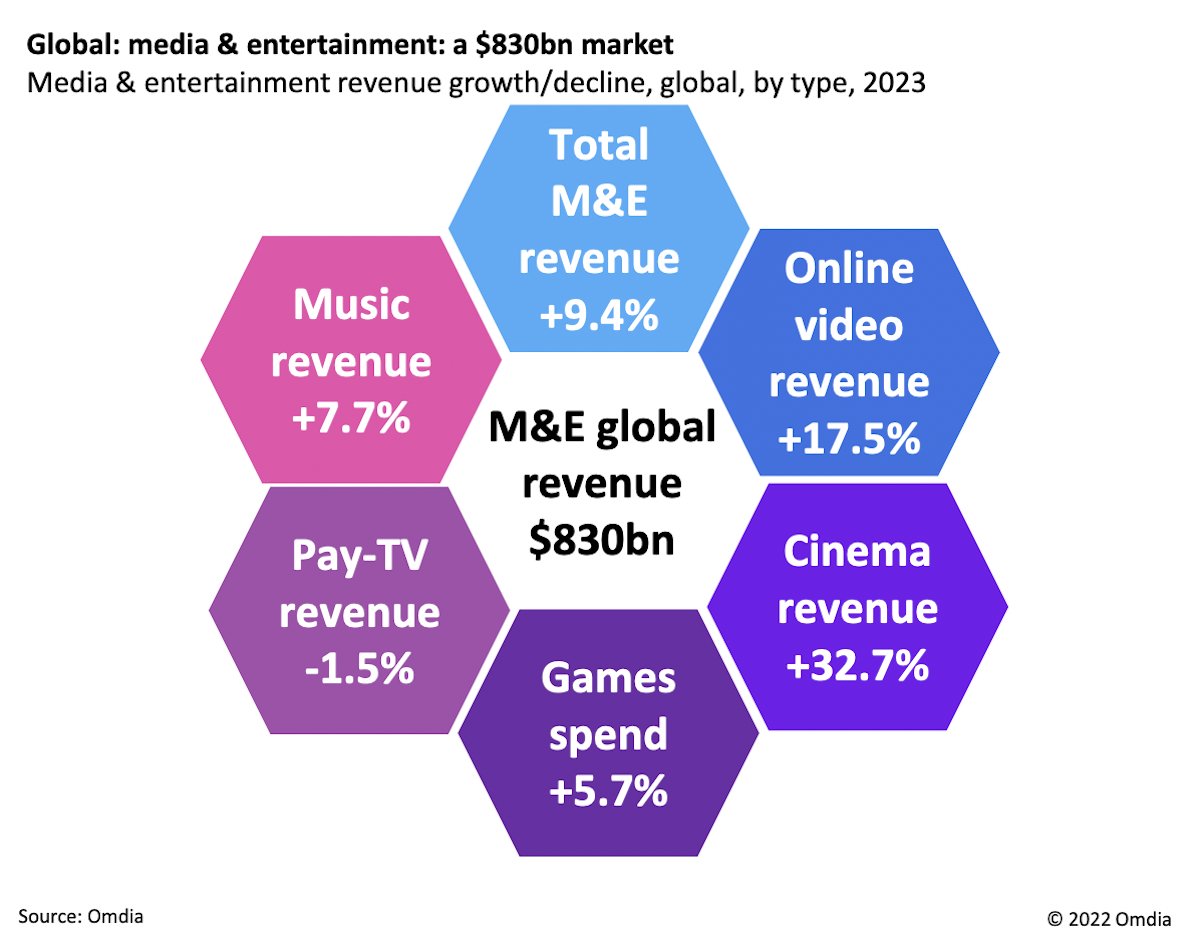

Omdia expects the value of the global media & entertainment (M&E) business to grow from $758.4bn in 2022 to $830.1bn in 2023, up 9.4%. The M&E sector does not, of course, operate in a vacuum, so the global economic headwinds expected in 2023 need to be acknowledged, although Omdia does not expect the macro-financial situation to seriously impact M&E growth.

During the last global recession (2007–2009), most media sectors continued to flourish with their revenue growing steadily. Since then, media markets have changed significantly – the rise of digital distribution has transformed the business. But these changes will, if anything, make the media sector even more resilient.

In 2007, YouTube was in its infancy and Wednesday streamer Netflix was still focused on its physical DVD operation. As we saw during the pandemic, most media (with cinema the obvious exception) continues to be able to thrive in difficult times. In periods of economic downturn, people (as per the pandemic) tend to stay at home more, spending extra time with their in-home entertainment options.

Having used the pandemic period to reassess their options, 2023 will see the result of that situation bear fruit with M&E companies adopting new business models, particularly featuring advertising, but also making other changes as necessary.

Advertising revenue is set for a significant spike in 2023. Even before the cost–of–living crisis, subscription revenue in some media segments was coming under pressure. With tough economic times expected for 2023, this will create an environment where advertising will thrive.

New hybrid business models are expected to emerge to embrace changing market dynamics. Media & entertainment services are learning the importance of not only acquiring customers but also retaining them. Rolling out new tiered access models, including free/ad–funded, is an important next step.

Meanwhile, the growth of connected device numbers is a key component driving the media & entertainment business by offering a crucial gateway to revenue generation.

Click to expand

Key 2023 recommendations

• Use non-intrusive formats as one way to limit ad loads. As companies make a shift toward advertising, they need to be wary of getting the balance right between generating necessary ad revenue while also providing a suitable consumer experience. Non-intrusive ad formats such as sponsored content and product placement are attractive options in this scenario as they can lift ARPU by bringing in more revenue without increasing the number of interruptive ads.

• Make the most of the connected TV (CTV) opportunity. A crucial element in the move toward ad model use is the rise of CTV, which has been central to consumer migration from traditional TV to online video; as apps became a critical driver of SVOD adoption. This creates a significant opportunity to tap into new revenue as advertisers follow consumers into CTV. Unlike environments in which big tech will dominate, with CTV, broadcasters and channel groups are well placed to benefit.

• Fine-tune offerings so the legacy element of the service can also benefit. Customers are going to face an array of new services and tiers to consider and navigate. It is important that these are all seen as being attractive and compelling. But some content should remain at least partly behind a paywall to prevent cannibalization of premium tiers. Thus, additional income from hybrid models will help to make the subscription model itself more profitable. This move will also help recoup revenue previously associated with legacy services, formats and models.

The excerpt above is taken from the report, ‘2023 Trends to Watch: Media & Entertainment Super Themes’, available here, by Adam Thomas, senior principal analyst for TV & online video at Omdia, which like TBI, is part of Informa.