After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: Exploring MENA’s booming content market

Hell’s Gate

MENA’s streaming potential is being tapped across AVOD and SVOD, but who are the main players and what’s happening on the content front? Omdia analysts Constantinos Papavassilopoulos and Marija Masalskis tell TBI what’s next for this fast-growing region.

The Online Video (OTT) market in the MENA region is experiencing a healthy growth trajectory, both in ad-funded (AVOD) and the subscription-funded (SVOD) segments of the market.

In 2020, some 37 Arabic original titles were produced by OTT players, including Netflix – this figure is expected to jump to more than 70 in 2022

AVOD is dominated by Meta (Facebook) and YouTube, while SVoD is more balanced, lacking a dominant leader. Omdia data shows the SVOD and AVOD markets in MENA have grown between 2016 and 2021 at a CAGR (compound annual growth rate) of 47% and 32%, respectively. During the same period, pay-TV shrunk by 1%.

OTT subscriptions overtook pay-TV in 2020, partly helped by Covid-19 lockdowns. The trend favouring OTT over pay-TV is clear and strong, and was expected to happen, even without the coronavirus impact, in around 2022–23.

Delays & growth

At end-2021, OTT subscriptions were at more than 7.2 million with growth supported by a young demographic (more than 65% of people are 35 years old and younger) and their preference to consume content on the go; monthly contracts; the fact that OTT content is considered more liberal than traditional TV, covering a broader range of topics; and the fact that expats residing in MENA seek OTT content as a method of connecting with their homelands.

On the other hand, the large free-to-air (FTA) offer, the high levels of piracy, and lack of a culture of protecting IP together with high pricing, lack of telecom infrastructure, and the meagre amount of Arabic original content up to 2020, have been among the most serious factors delaying the growth of the OTT market.

OTT has an uneven footprint across the whole region: the Gulf states are experiencing much higher number of subscriptions and subsequently revenues than the rest of the Middle East. A similar pattern exists in the pay-TV market as well, with higher penetration in the Gulf countries.

A variety of reasons explain this clear trend, including the much higher average income levels in the Gulf, the better telecom infrastructure and the presence of large swaths of ex-pats. A crucial factor that can act as an accelerator of OTT growth is related with payment systems and solutions, making online transactions easy and convenient.

Changing content consumption

Changing content consumption

Until recently, subscribers of OTT services in MENA were primarily served with foreign (mainly US-originating) content, which was the norm at least until early 2020.

Arabic content was primarily library content, in some cases more than four decades old, and had often first been broadcast in one of the many FTA TV channels thriving in the MENA market. Investment in Arabic original content was skimpy and the output of Arabic originals was just a handful of titles between 2014 and 2018.

A turning point for original Arabic content production for OTT platforms came in January 2020, when MBC totally revamped its own OTT service, Shahid.

The SVOD service of Shahid, Shahid VIP, offers a rich tranche of Arabic originals, most produced internally at MBC Studios. Arabic originals will be also coproduced or commissioned by MBC, while the MENA media group approached other producers in the region for content acquisition.

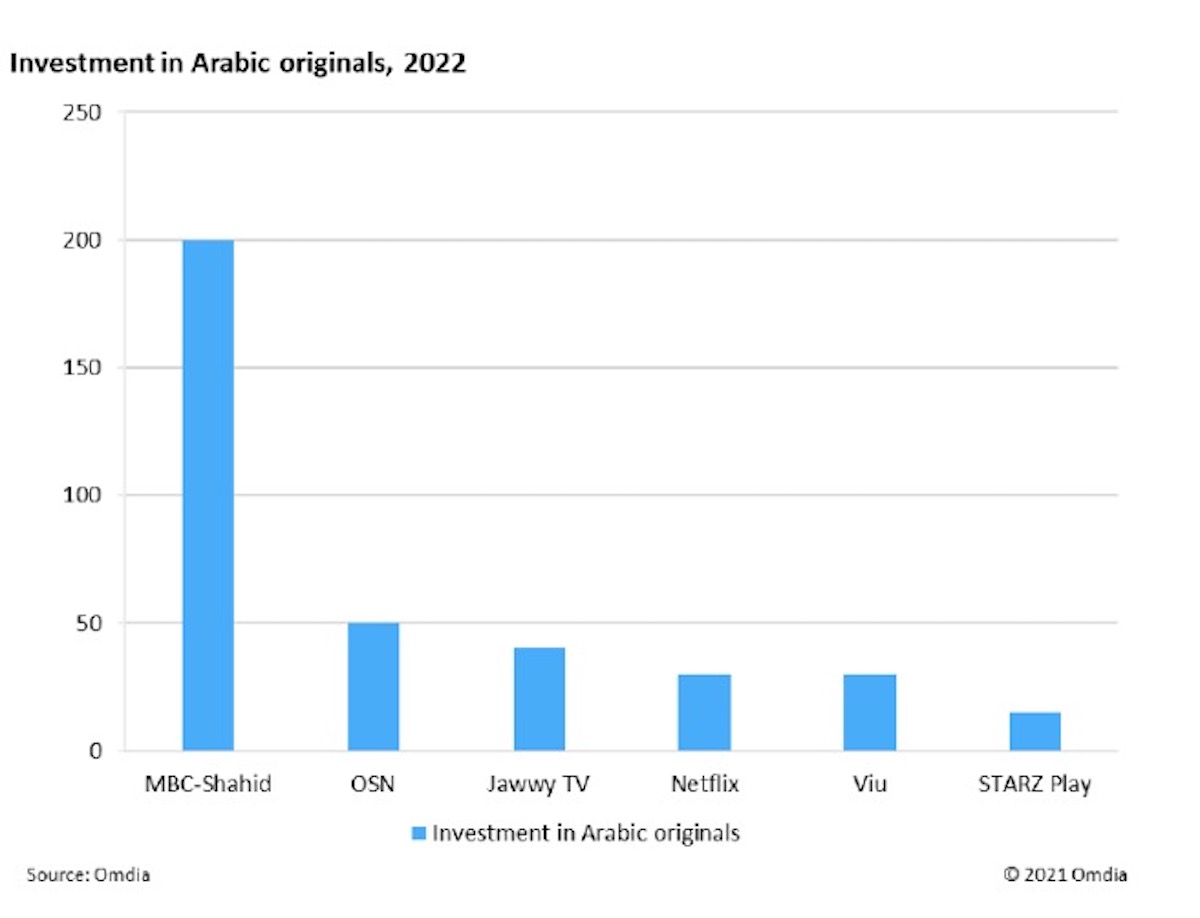

Omdia estimates that MBC is spending between $120m and $150m each year for content produced internally and is spending another $50m on acquisitions.

Other OTT services are following the paradigm of MBC with OSN, Jawwy TV, and StarzPlay Arabia all dedicating considerable parts of their budgets to Arabic originals.

Omdia estimates that in 2020 some 37 Arabic original titles were produced by OTT players, including Netflix. This figure is expected to rise to 50–55 titles in 2021 and jump to more than 70 in 2022.

The excerpt above is from the MENA Online Video Report – December 2021, available here. Constantinos Papavassilopoulos is Omdia’s principal analyst for TV & Online Video and Marija Masalskis is senior principal analyst for TV, online video & advertising. Omdia, like TBI, is part of Informa.