After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: What’s ahead for Turkey’s resilient TV market

Yargi (Source: Ay Yapim)

Turkey’s pay-TV and online video markets have faced substantial challenges over the past five years, including poor rural connectivity and 2023’s deadly earthquake, compounded by several years of rampant inflation. Here, Omdia’s Daoud Jackson explores what the coming months hold for the country.

In the face of substantial challenges, Turkey’s market has shown substantial resilience: pay-TV subscription numbers are generally growing and online video subscriptions continue to increase.

This resilience has been supported by two key pillars: a continued pipeline of high-quality content, which has now been exported globally, and the patience of providers, which have shown a willingness to delay price rises in the short term in the hope of recouping ARPU over the long term. As this pricing challenge gathers pace, the need for the right content, platforms, and packages has never been greater.

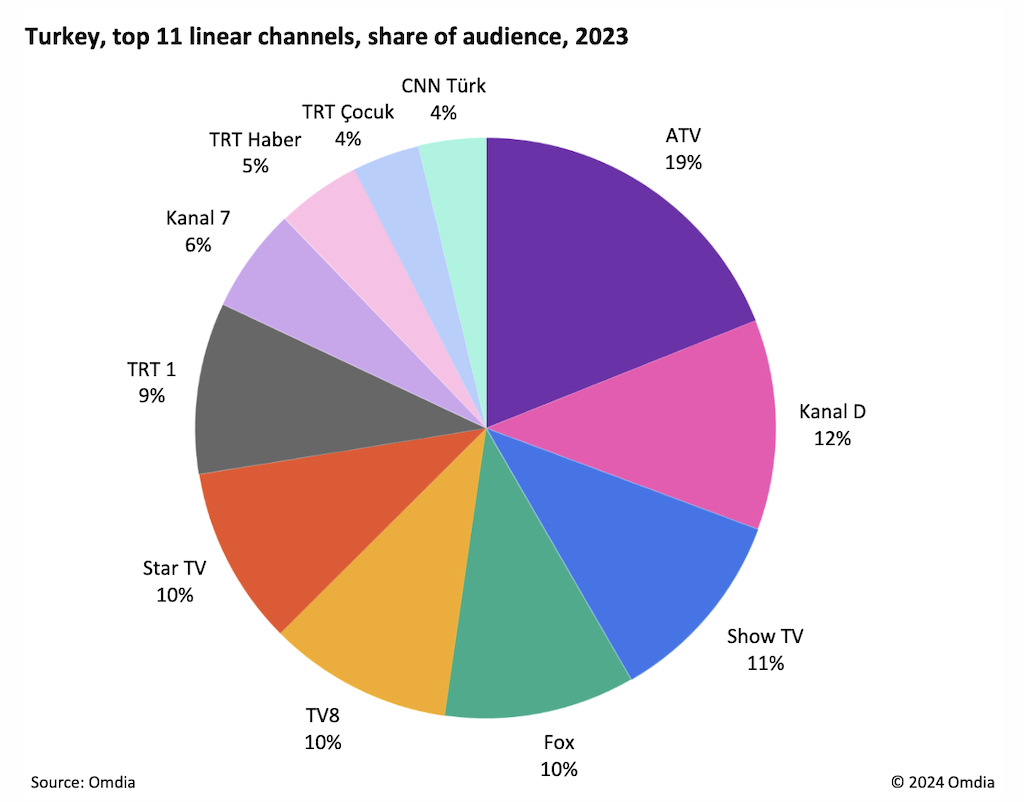

Overall, Turkey’s linear TV channel landscape is changing, but these changes are taking place slowly. Major general entertainment broadcasters such as ATV, Kanal D, and Show TV continue to dominate ratings, and though their audience shares are dropping by 1–2 percentage points a year, they continue to hold most of their audience. The decline of linear TV in Turkey is therefore happening slowly.

The market share of the 11 leading channels has consistently decreased. In 2019 these channels accounted for 62% of all viewing, but by 2023 this had fallen to 55% of the market as viewers watch an increasingly diverse range of channels and peak audiences fall.

These falls in viewership are seen in primetime and across income brackets. Turkey’s linear TV advertising market has remained relatively stable in the face of these challenges, and operators such as Yargi broadcaster Kanal D have sought to expand their distribution networks globally through new linear and free ad-supported streaming TV (FAST) channels in Latin America and Spain.

Turkey’s pay-TV outlook

At the end of 2023, Turkey had 7.6 million pay-TV subscriptions. Pay-TV penetration in the country is relatively high as a result of the slow rollout of free DTT options, and despite a slight fall in 2019, the market has consistently grown YoY.

Digiturk, a satellite-based provider with an emphasis on premium sports content, is owned by the beIN Media group and is the country’s largest pay-TV provider, while Turkcell TV+’s IPTV solution is the country’s fastest-growing provider and now has 1.3 million subscriptions.

Home broadband penetration continues to grow in Turkey and is a key driver of subscriptions as operators look to bundle pay TV with broadband with the aim of decreasing churn for both services.

However, the drive to increase broadband penetration and the persistent challenge of exchange rates have caused pay-TV ARPUs to shrink: all operators have a lower ARPU in US dollar terms in 2023 than they did in 2017.

Following Turkey’s 2023 elections and substantial disruption caused by a devastating earthquake in eastern Turkey, operators have been able to raise prices above inflation in 2023, recouping some of the exchange rate depreciation. Maintaining their subscription bases while restoring ARPU will be a persistent theme across Turkey’s pay-TV landscape in 2024 and onward.

Turkey’s regional inequality of infrastructure and income is persistently high, so operators will continue to offer low-cost or low-connectivity packages alongside those that will provide increased revenue.

The excerpt above comes from Omdia’s ‘Pay-TV & Online Video Report: Turkey – 2024’, by Daoud Jackson, senior analyst, media and entertainment, which can be read in full here (with a subscription). Omdia and TBI are both part of Informa Tech.