After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: Making sense of North America’s pay-TV & streaming landscape

Stranger Things S4

North America’s pay-TV & streaming landscape is shifting fast. Sarah Henschel, principal analyst at Omdia, puts recent events into context and outlines four key trends to watch.

Over the past two years, direct-to-consumer services in North America have grown significantly. With so many “must have” streaming services saturating the market, consumers began exhibiting “churn and return” behavior where users subscribe in and out of streaming services depending on content-release schedules.

In tandem with consumer self-bundling, corporate owners realised that saturation of services potentially limits subscription uptake and began consolidating services. Consolidation came in the form of online channel mergers, acquisitions and bundling.

Hybrid tiers and online linear TV (FAST channels and simulcasts) became more widely available on device platforms, SVOD services, and premium AVOD service throughout 2022.

While 2020 and 2021 saw the creation of PVOD and premium economic sell-through (PEST) windows as well as high value content going straight to owned and operated streaming services, studios and licensors pushed windows back to more pre-pandemic windowing strategies in 2022. With normalcy returning across windows, higher revenue can be earned at the title level.

Inflation fears and cost-of-living crises set in across global markets in 2022. Pressures on discretional consumer spending grew and saturated services like Stranger Things streamer Netflix and Loki provider Disney+ saw some quarters of stagnant subscription growth. Cord-cutting also accelerated as consumers continue to weigh the value of pay TV against self-bundling streaming services.

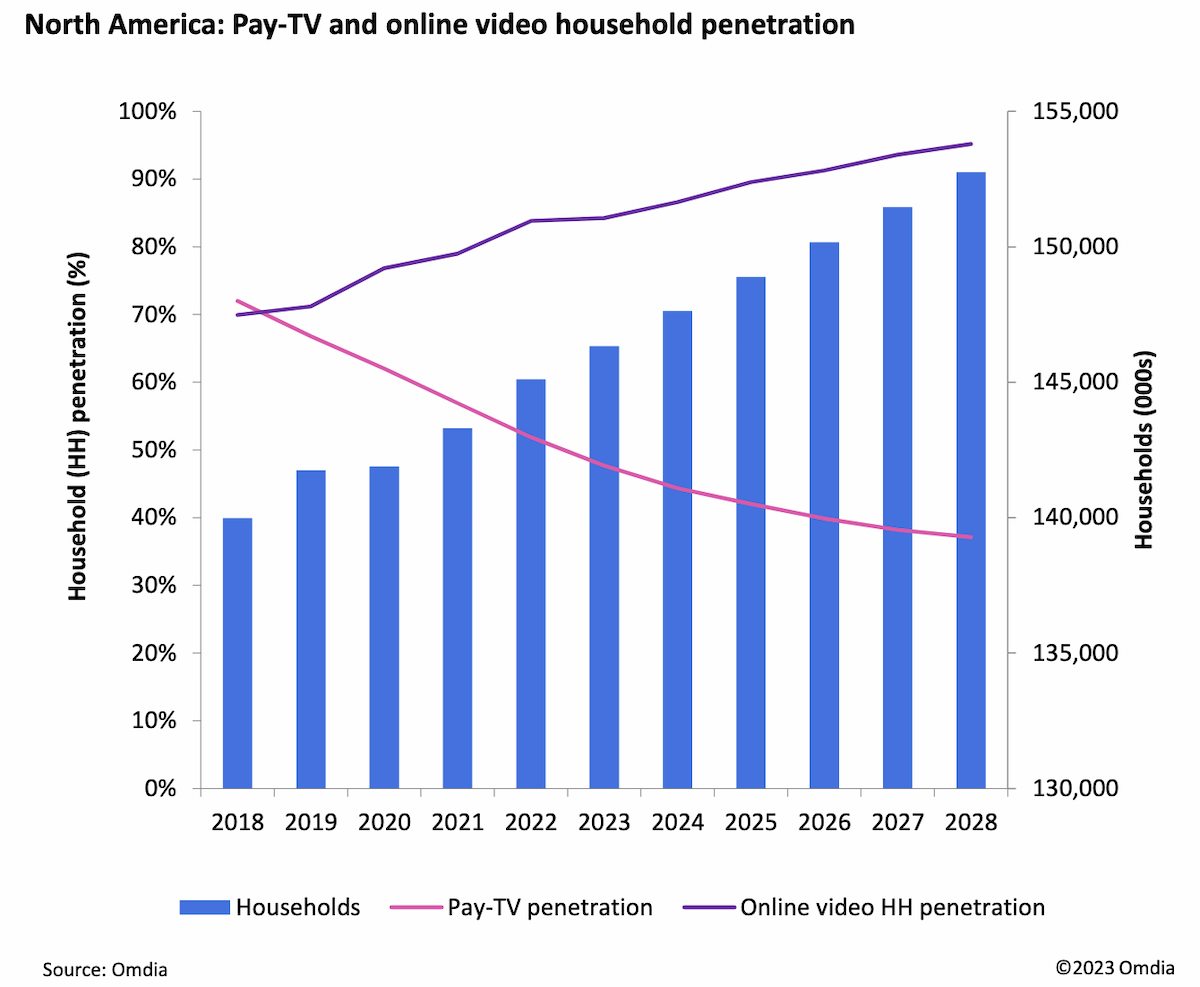

[Click to enlarge]

FAST (free ad-supported streaming TV) channels generated just over $4bn in ad revenue in 2022. The growth of connected TV drives this market and is building out a linear TV experience online similar to that of the traditional pay-TV experience. Native AVOD and SVOD services are integrating FAST channels into their experiences. Vix, Discovery+ and Paramount+ launched FAST channels in 2021, and Netflix and Disney+ each added hybrid advertising tiers in 2022.

Cost-of-living crisis

The average inflation rate in the US in 2022 was 8%. Rising costs of living force consumers to make spending trade-offs and encourage churn and return behavior. Despite inflationary pressures, the SVOD market grew in 2022, but the rate of service stacking grew, and more consumers began turning to free ad-supported offerings.

Churn & return

As new SVOD services quickly gained adoption and popularity in the US market, consumers are faced with juggling 10-plus “must-have” streaming services. From 2021 to 2022, “churn and return” behavior has only intensified with higher streaming costs and inflation pressures. Increased churning has also encouraged services to lean more heavily into aggregation and bundling opportunities because they prove to reduce churn.

Consolidation

Consolidation has increased significantly in 2022 and 2023. It allows services to grow pipelines of original content and to prove the value of increased pricing to consumers. Consolidation benefits consumers if it allows price flexibility with AVOD tiering or decreases the quantity of “must-have” services in the market. Too much consolidation, however, may decrease market competition, raise pricing too much, and therefore push consumers away.

The excerpt above is from Pay-TV & Online Video Report: North America – 2023, written by Omdia’s Sarah Henschel, principal analyst for Media & Entertainment. Omdia, like TBI, is part of Informa Tech. To read this in-depth report in full, click here (subscription required).