After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: Breaking down US studios’ moves into streaming

WandaVision

Omdia’s senior research manager Tim Westcott reflects on the transformative moves into DTC streaming by US studios and explores where the market is moving next.

All of the major studios – bar Sony which does not have one – have launched DTC services in the US and are targeting international roll-outs in 2021. These moves followed years of growth from streamers and marked the US studios’ attempts to assert themselves in the rapidly changing OTT market.

(Click to expand)

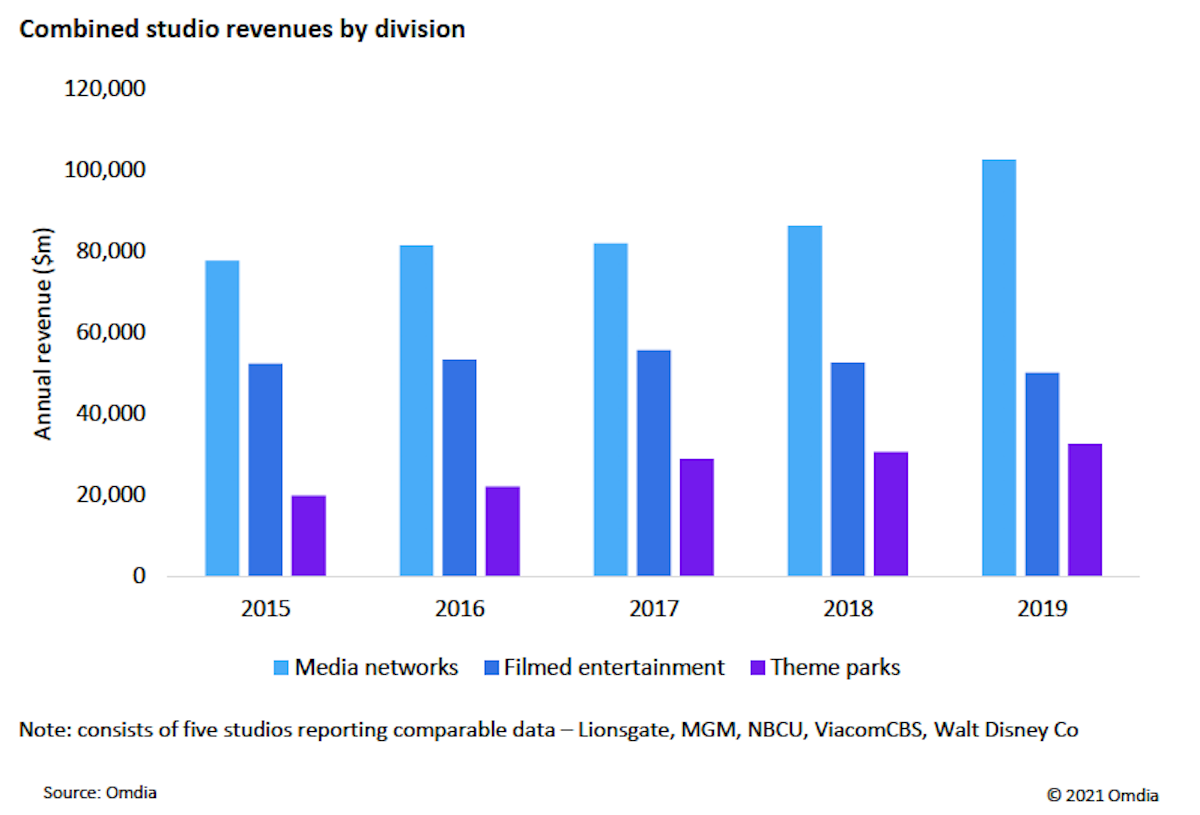

Ad & subs soaring importance

Media networks divisions (made up of advertising and subscription revenue) have increased in importance for the five studios analysed in this chart (21st Century Fox, Sony Pictures, and Warner Bros are not included because their reporting was less detailed, or not available over all five years).

In 2019, media networks accounted for 55% of combined revenue, compared to just under 22% in 2015. Filmed entertainment (theatrical, home entertainment, and TV licensing revenue) made up 27% of revenue in 2019 compared to 35% in 2015. Media networks revenue increased at a CAGR (Compound Annual Growth Rate) of 7%, and filmed entertainment declined 1%.

Only two of the studios – Walt Disney and NBCUniversal – operate theme parks divisions, which nonetheless accounted for 18% of combined revenue for all five groups in 2019. Broadcasting and cable networks accounted for 66% of Disney’s overall revenue in 2019. More than half of Disney’s studio entertainment division sales stemmed from theatrical, boosted by its acquisition of the 20th Century Fox studios.

The portfolio of linear channels and D2C services operated by the studios have been built up mainly via acquisition (Disney buying ABC and ESPN, Lionsgate buying Starz) or catalogue exploitation (NBC’s SyFy, Turner’s Cartoon Network). Most basic cable channels have been exported worldwide via pay-TV networks, with original programming output steadily increasing over the years.

However, it is in the international market that studios appear most likely to follow Disney by replacing linear services with their D2C brands.

(Click to expand)

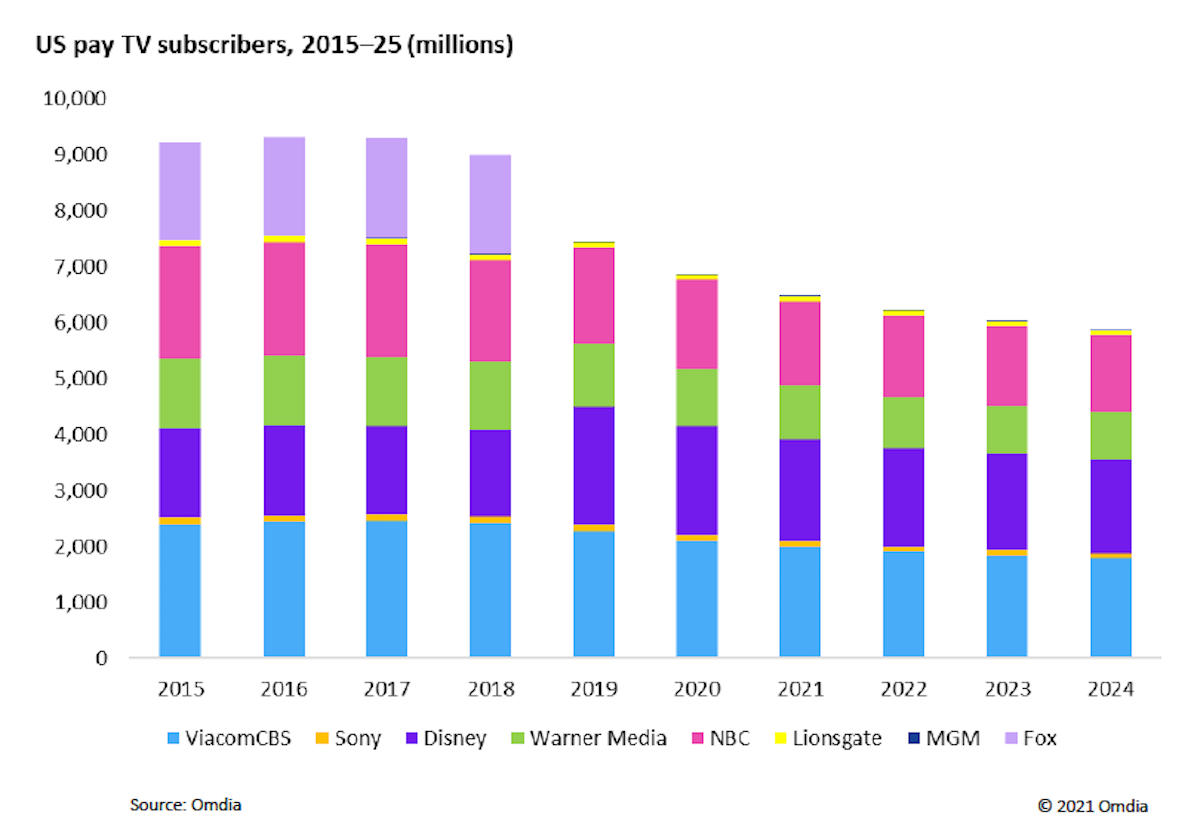

Ongoing linear decline

US pay-TV channel subscription numbers clearly show the impact of cord-cutting: most channel brands are seeing a steady decline, with the groups covered here shedding 2.4 million subscribers over the last five years (part of this decline is, admittedly, the exclusion of the Fox news and networks not bought by Disney). However, over the next five years, Omdia forecasts the loss of another million subscribers in the US for these groups.

Outside the US, the international channels market is still growing. This includes markets like India where the studios are prominent in operating channels (especially Disney, which added Star to its roster as part of the 21st Century Fox acquisition). However, these numbers are inflated by some channels with free-to-air distribution. Also, revenue is considerably lower than in the US, and certainly not of a scale to compensate for the decline in the US.

Walt Disney has already shut down linear channels in markets where it has launched its D2C service, Disney+. In the UK, the closure of its three Disney-branded channels followed its inability to secure the carriage terms it wanted from pay-TV operators Sky and Virgin.

While no other US studio group has gone as far as Disney so far, the international rollout of DTC services like HBO Max, Peacock, and Paramount+ seem to make a further culling of channel brands likely over the next few years – especially the weaker services with low audiences, and content which can be consumed on demand.

(Click to expand)

OTT’s power surge

Another perspective on the performance of the US studios’ channels stems from comparing their revenue from advertising and subscription with the leading global online players.

YouTube’s ad revenue was $13.4bn in 2019, up from $3.2bn five years ago, and more than any of the studios. Facebook’s video ad revenue was even higher, according to Omdia’s Advertising Intelligence, at $15.9bn. With the addition of the 21st Century Fox networks, Disney overtook NBC Universal, reporting $11.5bn in ad revenue.

Netflix has been outpacing the US studios with the growth of its worldwide streaming revenue, which grew to $19.8bn in 2019 from $6.1bn in 2015. NBCUniversal’s revenue of $22.3bn (which includes the Sky platform) were ahead of Disney’s $17.4bn. Warner Media was the next largest with $13.6bn. By launching their own streaming services, the studios would no doubt be happy to gain some dynamism for their subscription revenue – preferably at the expense of Netflix.

The excerpt above comes from Broadcaster Transformation – The Studios, an Omdia report written by Tim Westcott, Senior Research Manager, Channels, Programming and Advertising. In the coming weeks, we will dive into the DTC strategies employed by two specific US studios.