After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: Diving into advertising’s effect on content in 2023

Glass Onion

Advertising has become a key source of revenue as streamers look to fight subscriber fatigue, but what does 2023 have in store and what are the key trends? Omdia’s Matthew Bailey explains the story so far and picks out how content owners can benefit.

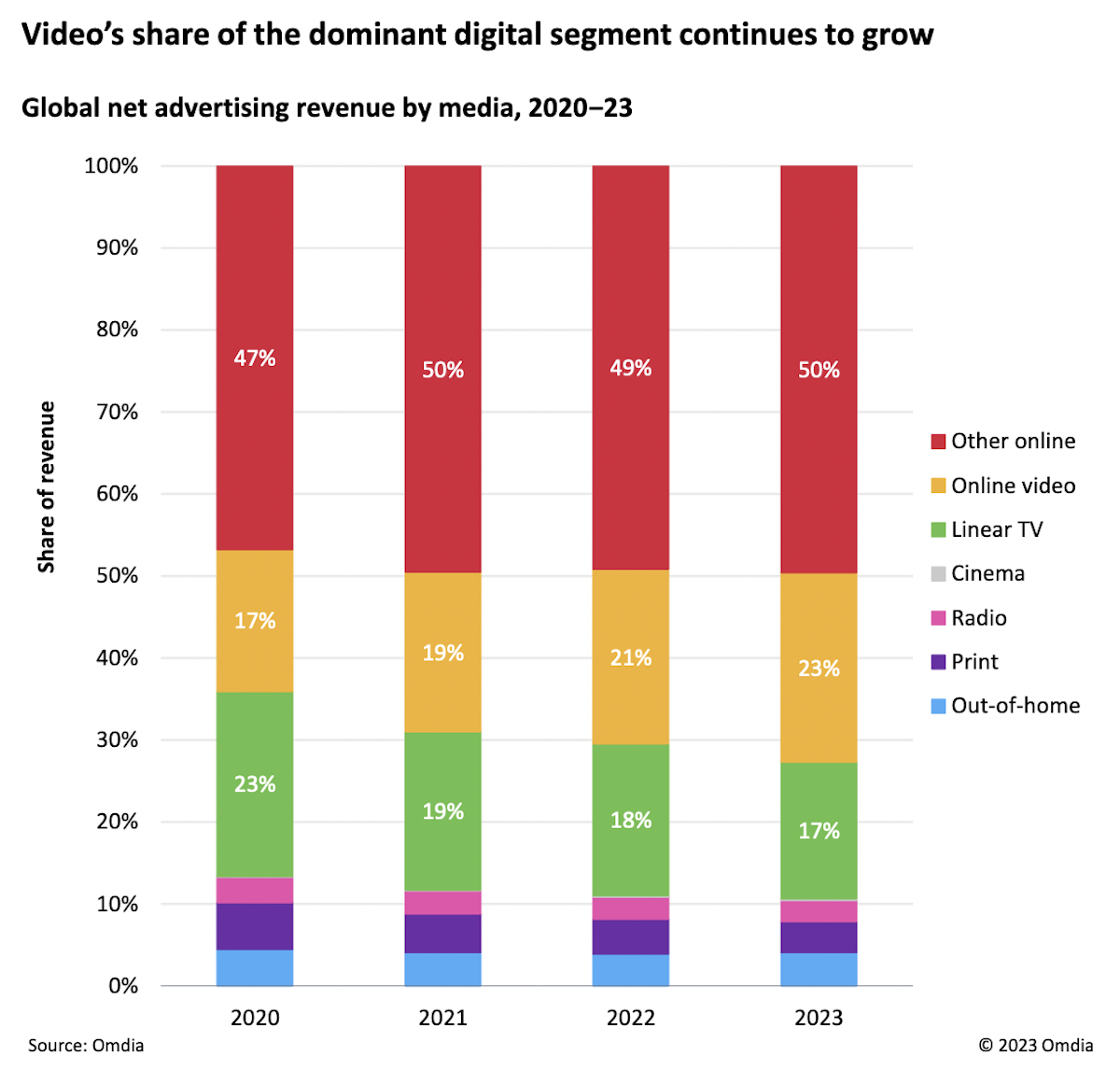

Digital’s march on advertising revenue has continued largely unabated over the past decade, with online advertising taking a 50% share of total global advertising revenue for the first time in 2021.

However, 2022 saw a large slowdown, or even decline, in the ad revenue of digital giants Google and Meta, leading to a loss of ad market share for online during the year.

Producers should experiment with short-form that can be distributed and potentially monetised through TikTok – branded content will be an especially important area to consider

Yet one area of online advertising that continued to grow its share in 2022 is online video advertising, and this will continue into 2023 when it will take 23% of total global advertising revenue.

Critically, this will be driven by both traditional TV players, which are increasingly pivoting to digital platforms and advanced TV advertising, and digital new entrants.

The latter includes mobile video powerhouse TikTok (already a key threat to Google and Meta) and connected-TV (CTV) manufacturers pivoting into advertising and free ad-supported streaming TV (FAST) in a bid to bolster profitability.

It also includes premium over-the-top (OTT) video players, such as Netflix, which are turning to hybrid monetisation models spanning both subscription (SVOD) and ad-supported (AVOD) video on demand.

Google and Meta still play a big role in digital video, but it is a segment where other players, and the vendors that support them, can not just compete but can thrive as the worlds of linear TV and digital ads collide.

Advertising superthemes for content owners

For content owners, FAST clearly offers potential but rights holders looking to enter the space should consider engaging point solutions from vendors. This will give them greater control over, and visibility of, monetisation while also enabling an omni-FAST platform distribution strategy.

[Click to expand]

Content producers should experiment with new types of short-form video content that can be distributed and potentially monetised through TikTok. Branded content will be an especially important area to consider because TikTok videos often blur the line between paid advertising and user-generated videos.

Content producers should also explore the implementation of dynamic product placement technology – or at least design content with this in mind. This could even involve exploring the applications of in-game ad tech in other areas of media and entertainment produced using game engines.

Game developers need to design premium games with advertising in mind. This will be especially important if they are intended to operate on a free-to-play basis or will be part of a subscription access offering.

Mid-to-low tier sports rightsholders should explore sports streaming in FAST environments. Such licenses will be less appealing to premium video providers but could grow their audiences and monetisation on free, ad-supported services.

The extract above is from 2023 Trends to Watch: Advertising Superthemes, written by Omdia’s principal analyst for media & entertainment, Matthew Bailey. To read more, click here (subscription req’d).