After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Weekly: Dialling down on distribution ahead of MIPCOM Online+

Apple TV+ acquired Cineflix Rights’ drama Tehran

This year’s pre-MIPCOM rush has felt like nothing else before it, not least because no one is counting down the hours before their plane, train or automobile whisks them off to the French Riviera for a few days of frenetic selling and networking – and a glass of rosé or six.

Despite this, there has still been a pre-market rush, as distributors attempt to put their programming front and centre on screens around the world as buyers descend virtually onto MIPCOM Online+.

This radical change is the latest evolutionary moment for the distribution industry, where pre-existing developments have been accelerated by the onset of Covid-19 and its myriad impacts on the wider content business. Many of these issues were brought into sharp focus in our Distributor’s Survey 2020: here are six key takeaways that shine a light on where the industry is heading.

Inflexible investments & intractable delays

Inflexible investments & intractable delays

Distributors have adapted rapidly to the scripted market over the past five years, as the growth of streamers and more recently the vertical integration of US studios impacted product available to sell. The result is that distribution outfits have transformed what they do: they are no longer simply sales companies, they are financiers, deal-makers and lynchpins to the whole scripted process in many cases.

Adept and nimble as they have been over recent years, however, the production hiatus over the past six months or so now means they too are facing deep financial hits, as their heavy investments to get shows off the ground offer little sign of being recouped within normal timeframes.

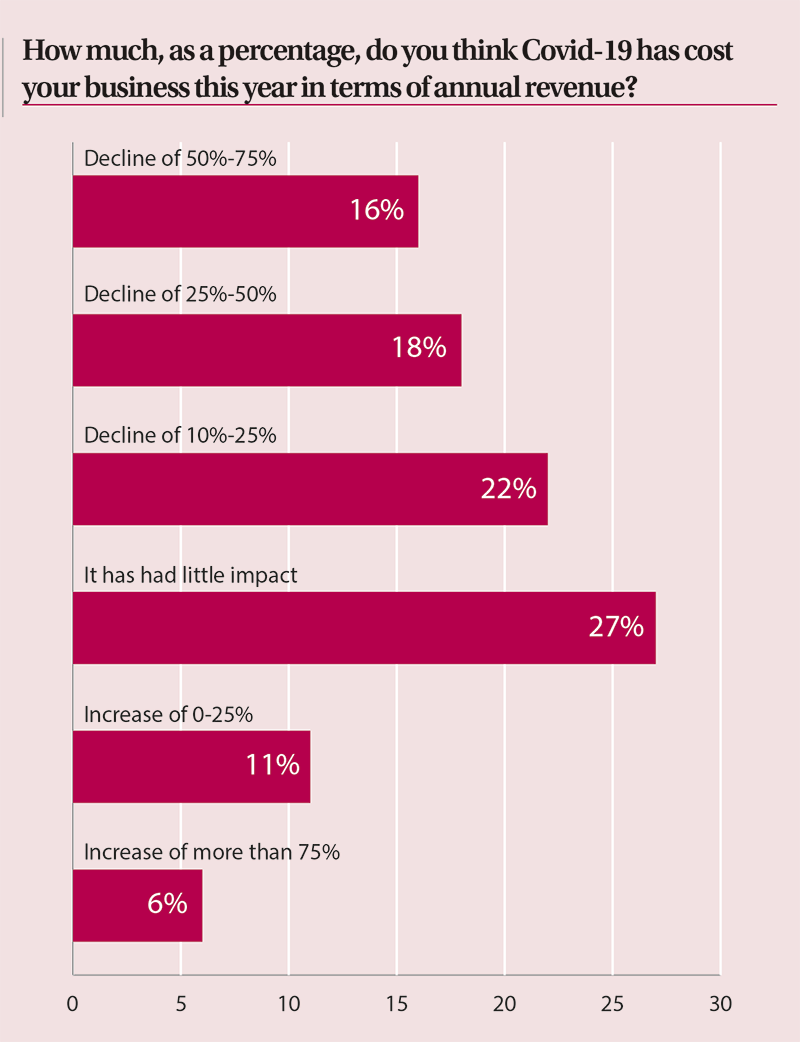

The issue is immediately apparent in this year’s results, with more than 50% of companies involved in the sale of scripted product reporting a decline in annual revenue in 2020 because of the pandemic. The severity of the hit is widespread with some fortunate to have shows wrapped just in time prior to lockdowns and others forced to pause production entirely. Almost 20% say they have seen a decline in revenue in excess of 50%, while another 18% say the reduction lies somewhere between 25% and 50%. Yet the picture is complicated. Almost a third of respondents report that the pandemic has had little impact on their revenues, while 11% say that they have actually seen revenues rise by up to 25%.

Happily Married

Priming the pipeline – if you have the product…

Covid-19 has coincided with the launch of numerous streamers, most importantly from the US studios. As touched on above, this means there is – and will continue to be – less supply for others as the likes of WarnerMedia and Disney plump up their OTT services with their own scripted series. But the effect of the pandemic is two-fold. HBO Max, for example, has found its roll-out plan scuppered as shows are unable to wrap production, meaning acquisitions are vital. Just today, the WarnerMedia streamer added UK drama I Hate Suzie to its slate.

Secondly, there are numerous incumbent and recently launched streamers – not forgetting the hundreds of broadcasters around the world – without their own production pipeline. For them, the US studios’ DTC move means less product available to buy – even if large swathes of the world were already moving slowly but surely away from American drama. The result is more competition on the buying side, at least for those holding the right IP. “It has led to some significant sales for us,” says Chris Bonney, CEO of rights at Cineflix Media, which struck one of the deals of the summer with drama series Tehran snapped up by Apple TV+. Other deals underline the potential of ambitious regional streamers too, with Happily Married being picked up by French SVOD Salto.

Outback Truckers

Keeping the wheels rolling

When lockdowns first landed outside of China, attention rapidly turned to unscripted content to fill the imminent gaps in schedules. Home-filmed cookery shows were commissioned, documentaries based on archive footage were hustled through production and innovative producers strapped cameras to dogs to ensure filming could continue.

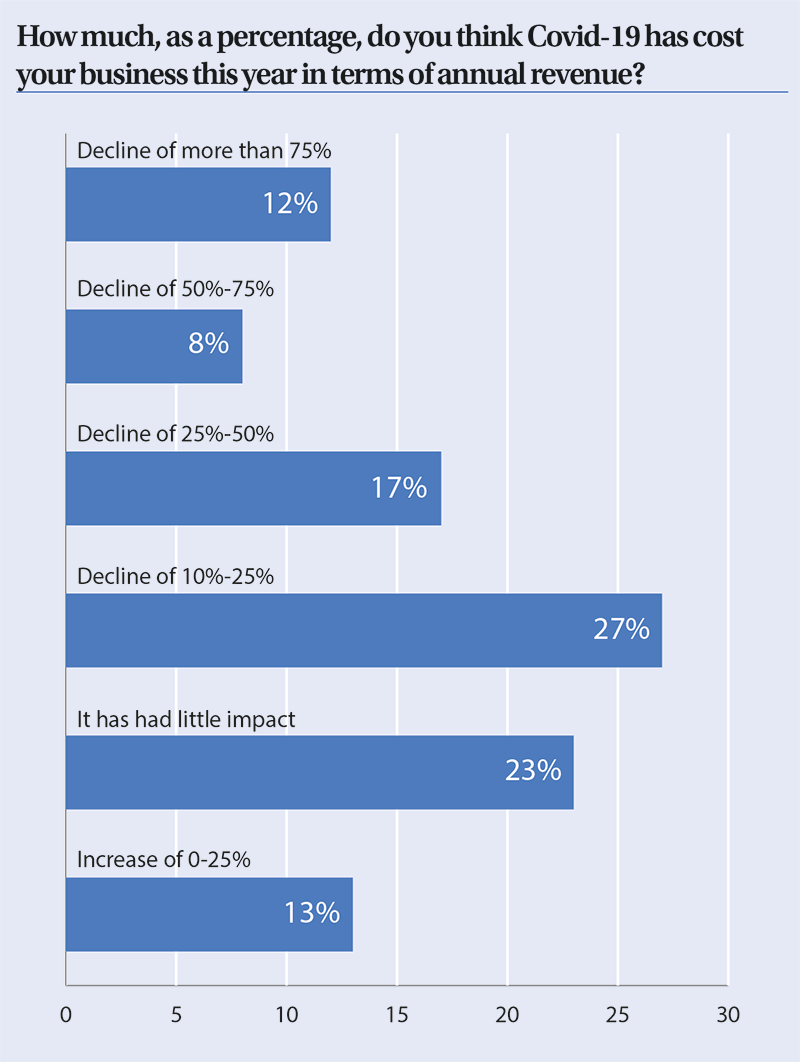

This innovation helped some, with almost a quarter of respondents working in unscripted saying that Covid-19 has had little impact on their annual revenues this year. A further quarter, however, said they had noticed a decline of between 10%-25% while more than a third said they have seen declines in excess of 25%.

A number of respondents added that many of the best-selling genres from their catalogues over the last few months had been male-skewing programming, which was used by broadcasters to plug holes where sports should have been shown. Stalwarts of the unscripted space remain too, however, with crime, specialist factual and history all cited as being major money-makers for distributors. Fiona Gilroy, content sales & acquisitions director at Flame Distribution in Australia, says that the slow-down of some productions opened opportunities for other content too, with her best-sellers including Outback Truckers.

Waiting for the lights to change

Waiting for the lights to change

For many in the sales game, opportunities have been taken but numerous respondents were quick to point out that while demand for unscripted product might have ticked up, the effect of Covid on advertising-supported networks has been immense, causing “a stranglehold” on broadcasters. Roger Vanderspikken, COO at Fred Media, points to the pressure on broadcasters’ budgets as being the biggest impact of the pandemic so far, and that is having a direct effect on future pipelines too as caution slows down the greenlight process.

This is highlighted by the more than 80% of respondents who say decisions on commissions – and deals – have been delayed, while the sheer unpredictability of how the pandemic will evolve means there are question marks over delivery timelines, leading to risk aversion. Unscripted was already facing a squeeze – something noted by Woodcut Media CEO Kate Beal in her column for TBI earlier this week – and the immediate future looks likely to offer little respite in the ongoing battle to get shows funded and into production.

Playing safer

Playing safer

The format industry was already facing considerable challenges prior to the effects of Covid-19, as mergers and acquisitions buffeted the smaller and more independent operators in the sector. The pandemic has not helped, with more than three-quarters of respondents saying that the effects of Covid-19 has left their businesses worse off.

Banijay Rights CEO Cathy Payne adds that there are numerous knock-on effects for the business, which will also be felt by those in the format sector. “The pause in production has affected pipelines and broadcaster schedules,” she says, “and in addition to this there is an increase in production budgets caused by the Covid production hiatus as well as Covid protocols needed once production resumes.”

Almost 30% of respondents have had to lay off staff as a result, but reflecting the trend across the content business, the vast majority believe their company and the market will improve. Although ad spend is now by and large rebounding for networks around the world – albeit from severe lows during the depths of the crisis earlier this year – the impact has been great and the effect on programming clear. Broadcasters are tending to look for safer bets and the result is causing format distributors to adapt their strategies.

“There is a reduction in risk from broadcasters willing to take on content,” says Siobhan Crawford, sales and acquisitions at the Netherlands-based Primitives, “and that means recommissioning existing brands is most common.” This focus on risk and commercial broadcasters with squeezed incomes is reflected in this year’s findings and it was occurring prior to the pandemic. Outside of the immediate repercussions of Covid-19, more than 70% of respondents said the greatest challenge for their businesses over the past 12 months had been falling ad spot revenues at networks.

But there are deals to be had and bibles to be sold. Dating, factual entertainment and reality formats remain among the best-sellers, but there has also been noticeable demand for scripted formats too, according to respondents.

Kids are alright

Kids are alright

Demand for animation remains high in the kids’ TV sector, which as a whole appears to have weathered the worst of the pandemic, with parents the world over turning to their television screens to help keep youngsters occupied during the height of lockdown.

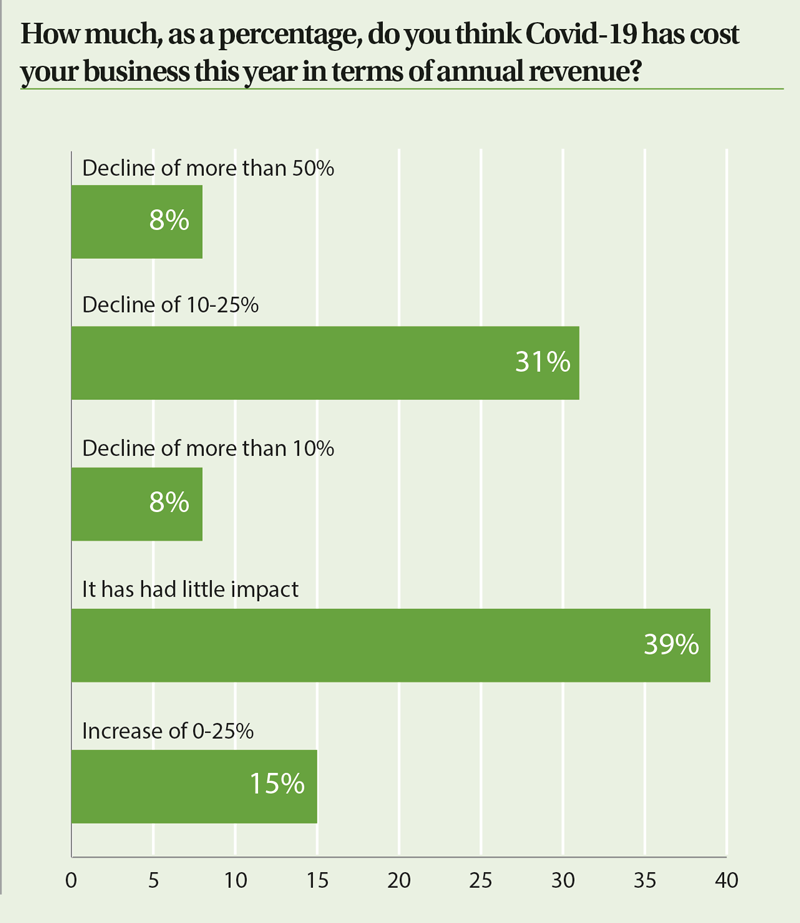

However, though some in the sector remain optimistic that things will improve in the coming 12 months, almost as many remain uncertain. Some companies have clearly been seeing out the storm better than others, with more than 38% of respondents in the sector claiming that Covid-19 had cost them little in terms of annual revenue, and only around 7% claiming losses of more than 50%.

In-fact, 15% of respondents said their revenue had actually increased by as much as 25% in this period, perhaps due to the increased demand for children’s programming as schools and nurseries were closed and youngsters spent more time than ever before switching on to be entertained.

Yet with broadcasters and platforms around the world tightening their purse strings, and in line with other sectors of the industry, it was not surprising to see that 92% of respondents say that their clients have delayed decision-making, either when acquiring or greenlighting shows. Expectations that business will improve over the next year were divided, meanwhile, with only 54% believing things will get better for their companies, and just the same percentage foreseeing an improvement in the market as a whole.