After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: Where next for UK broadcasters in a post-Covid world?

Aled Evans, senior analyst at TBI sibling Omdia, last week offered a snapshot of how the UK’s content business fits into the wider global landscape as part of the latest TBI Talks. Here, we reflect on his presentation and explore how a squeezed broadcasting sector might affect producers over the coming years.

Broadcasters and producers were faced with a rapidly shifting industry prior to Covid-19 but the pandemic has further complicated a landscape increasingly populated by fast-growing US-based streamers.

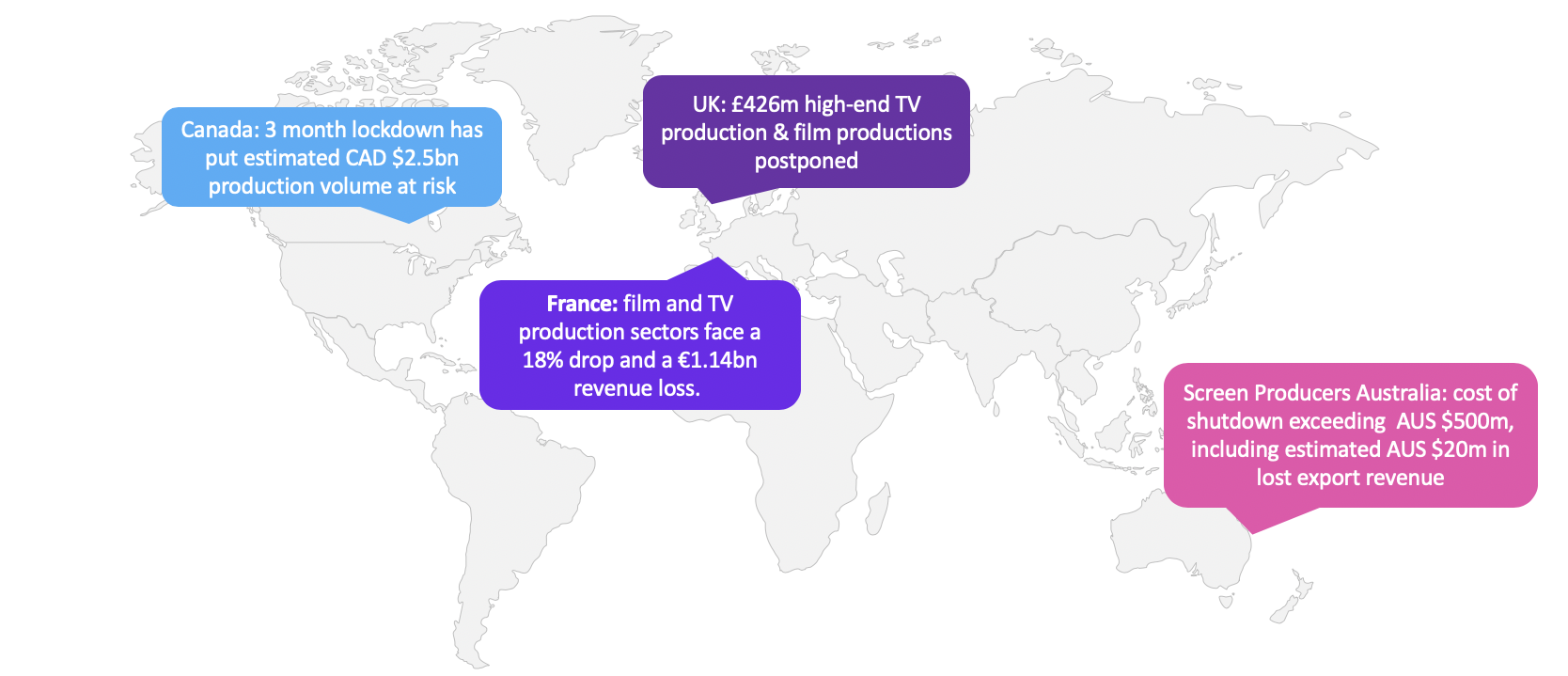

As the graphic above neatly demonstrates, the impact of Covid-19 on the global production business has been stark and widespread. Shows that were put on hiatus in mid-March are now only just beginning to return to production, with many series – particularly of the scripted variety – still on hold as suitable protocols are designed and implemented.

Like most countries, the UK production business has been struggling with the ramifications of the pandemic on its operations.

A much-needed insurance scheme was introduced last week following months of complex negotiations, with the hope being that the £500m ($650m) government-backed fund will help domestic film and TV productions struggling to get Covid-19 related insurance – and kickstart productions worth upwards of £1bn.

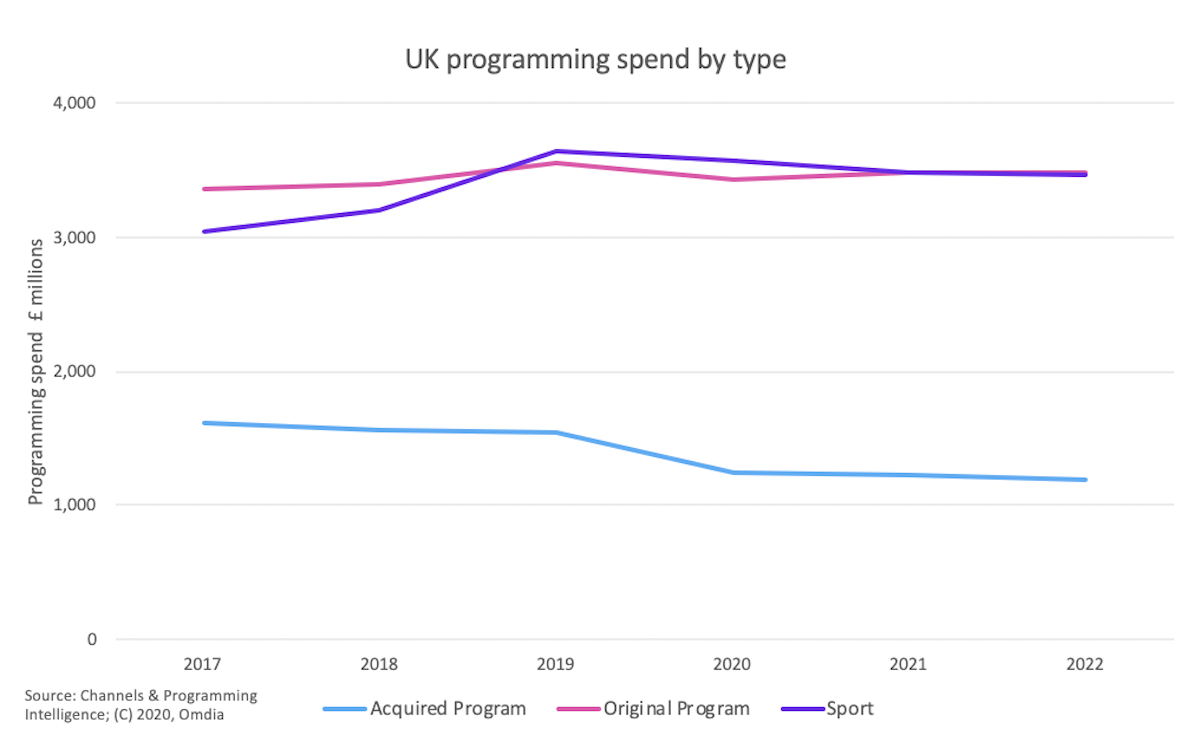

UK programming spend by type

While some producers, particularly of unscripted fare, have been able to get shows back up and running incredibly quickly, the longer tail effects of the pandemic on the broadcasters commissioning them remain to be seen.

As Evans points out, Omdia’s Channels & Programming Intelligence Service data suggests that broadcasters will see a drop in spend on originals in 2020 compared with 2019, with the figure then remaining relatively stable moving into 2021 and 2022.

Acquired programme spending is also expected to fall this year as the broadcasting landscape remains a challenge for operators facing considerable external pressures.

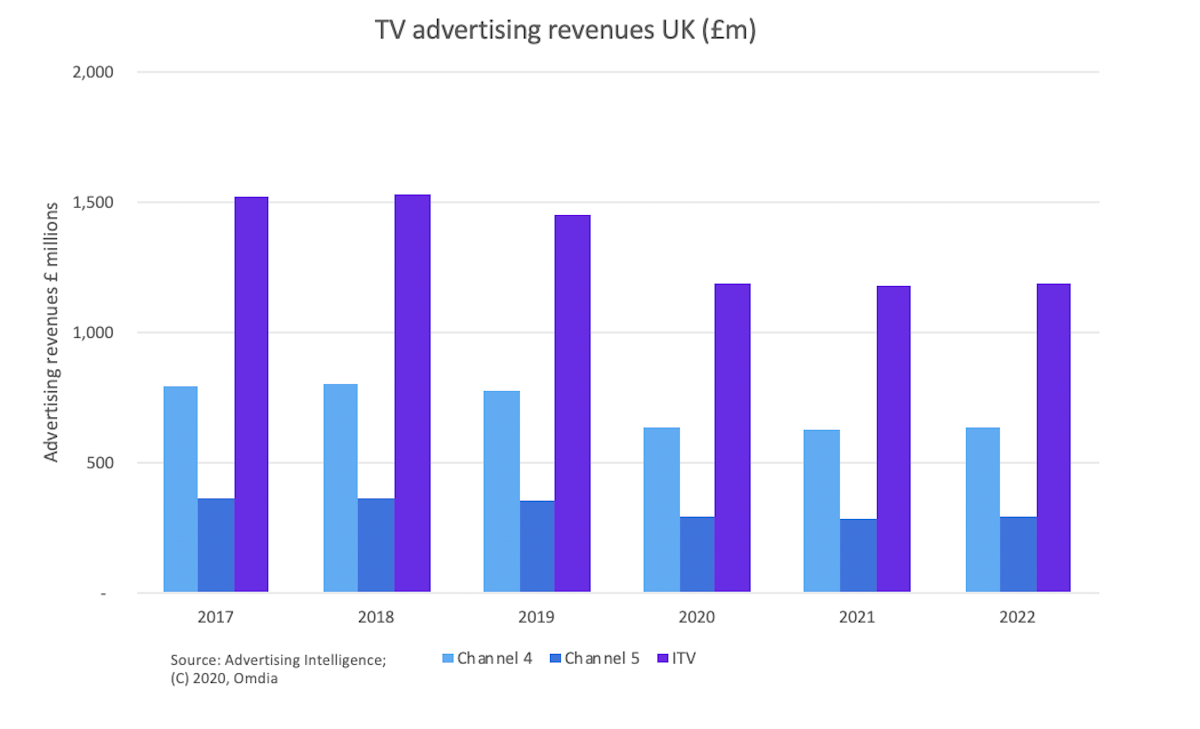

This trend – which reflects only broadcast spending and not streamers – dovetails with advertising data from Omdia’s Advertising Intelligence Service.

Both ITV and Channel 4 in the UK have been hit hard by the pandemic, with advertisers rapidly pulling spending as the full extent of the pandemic emerged. ViacomCBS-owned Channel 5 is also feeling the effects of a squeezed market as brands postpone marketing campaigns.

Both ITV and Channel 4 in the UK have been hit hard by the pandemic, with advertisers rapidly pulling spending as the full extent of the pandemic emerged. ViacomCBS-owned Channel 5 is also feeling the effects of a squeezed market as brands postpone marketing campaigns.

Western Europe programming spend by type

ITV and C4 have made a slew of cost-cutting measures including furloughing staff and slashing programming spend, but it is worth noting that the trend of falling advertising revenue has been apparent for the past five years.

Indeed, Omdia’s figures suggest spending in the UK linear TV advertising market has fallen from £4.29bn in 2015 to £4.12bn in 2019. That spend will only decrease in 2020, and little if any growth is expected across the major players over the next two years.

The UK’s position, following several years of original programme spending growth, is now comparable to a wider trend in Europe, where Western European programme spending on both acquired and originals is expected to continue its downward trajectory.

To hear Evans’ presentation and the full TBI Talks sessions – including BBC entertainment chief Kate Phillips and Argonon CEO James Burstall discussing everything from insurance to Strictly Come Dancing – click here.