Online video advertising forecast to lead M&E revenue by 2028

Maria Rua Aguete

Online video advertising is expected to become the top source of media and entertainment revenue by 2028, according to data revealed by research powerhouse Omdia at the Connected TV World Summit in London yesterday.

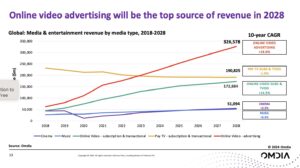

According to Omdia, online video advertising, growing at 18% CAGR over a 10-year period, will reach $327bn by 2028. That compares with online video subscriptions and TVOD revenue – together growing at 14.5% CAGR – of $173bn.

Pay-TV subscriptions and TVOD will meanwhile decline at 1.9% CAGR, but will still be a greater source of revenue than SVOD, with sales totalling $191bn by 2028.

According to Maria Rua Aguete, research director at Omdia, the number of SVOD services is now more or less fixed, with no new major streaming services expected to launch. On the contrary, it is likely that there will be consolidation in the sector (with speculation currently focused around the future of Paramount).

SVOD is still growing, but at a much slower rate than previously, according to Omdia.

Source: Omdia

Net additions globally amounted to only 108 million last year, the lowest in five years. While net adds are expected to bounce back to 148 million for the current year, Omdia expects the rate of net additions to decline thereafter.

This is partly due to the number of SVOD services per home declining. While the number of streaming services per home has actually increased this year, the rise is entirely due to the uptake of free services, including SVOD, social video, FAST, other free TV services and AVOD.

According to Omdia, the number of free services taken by the average home stood at 6.2 last year, compared with two SVOD services.

YouTube remains the most popular video service measured by monthly usage in all markets studied by Omdia, but there are variations across markets in the popularity of other services.

While Netflix is the number two service in the US, Instagram Reels takes this slot in Brazil.

In European markets meanwhile the popularity of over-the-air broadcast and public service broadcaster streaming services is notable. In the UK, BBC iPlayer takes the number two slot, followed by Netflix, free-to-air TV and streaming-centric broadcaster Channel 4.

In France, free-to-air broadcast takes second place, followed by pubcaster streaming service France.tv, Netflix and commercial broadcaster TF1’s streaming service.

In Germany, public broadcast streamers take the number two and three slots, while in Spain free-to-air TV takes that position, followed – as in Brazil – by Instagram Reels.