After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Distributor’s Survey 2023 – Part 1: Scripted

From FAST growth to pre-financing shows and navigating a consolidated market, the 2023 survey reflects the ability of the distribution industry to adapt to change. With more than 40 responses from sales companies around the world, join us as we discover this year’s key trends.

It has been a year of transition for many in the TV industry. On the buyers’ side, it has been tough: US studios have been coming to terms with the realities of streaming; commercial networks have been adapting to a squeezed advertising market; and public broadcasters have been ducking and diving as they try to stretch budgets. For those on the other side of the transaction, consolidation and risk aversion are very real concerns, but growth areas such as FAST and the ever-increasing importance of distributors in financing are seen as offering considerable potential in a business that has always had to adapt quickly.

Scripted: Crime pays

Crime and thrillers have driven the scripted sector over the past 12 months, with FAST replacing increasingly cost-conscious global streamers as the main growth area looking ahead

It has been a tumultuous year for those in the scripted industry, with the once happy-go-lucky global streamers pulling the plug on spending and nixing numerous shows in the process.

In the US, the writers and actors strikes created simultaneous opportunities and challenges for distributors, as domestic networks and streamers look for offshore product to fill growing gaps.

Outside of the US, a similar trend is growing as buyers eschew delayed American dramas in favour of looking for more local fare or just shows that will be delivered on time.

This shift is not necessarily new of course, but the lack of competition from the US does mean more opportunity for distributors to get their shows onto screens. And with the strikes only just over, the lag effect for buyers is real.

“The strikes are causing delays in the US scripted content pipeline,” says Cineflix Rights CEO Tim Mutimer, ahead of the WGA forging a new deal with the AMPTP in late September, but he points to his company’s “diversified” slate with shows from the UK, Australia and Canada, which are not impacted. “We are also anticipating that delays in the pipeline may mean buyers taking another look at existing oven ready IP,” Mutimer adds, with his comments echoed by others including Federation’s Guillaume Pommier and ZDF Studios Robert Franke.

Certainly, this year’s Survey suggests that distributors in the scripted sphere have enjoyed a buoyant 12 months, with every respondent claiming that annual revenue had increased and 63% reporting a rise of between 10-19%. A slowdown is evident when comparing to last year’s figures, however, when almost a third of respondents in 2022 reporting a revenue rise of 30% or more.

Further, revenues in 2023 did not necessarily translate into profits, reflecting the effect that the increasing costs of scripted is having on distributors. Just over 45% of companies saw profits remain the same year on year, while 29% claimed an increase of 0-9% and 25% reported a rise of 10-19%.

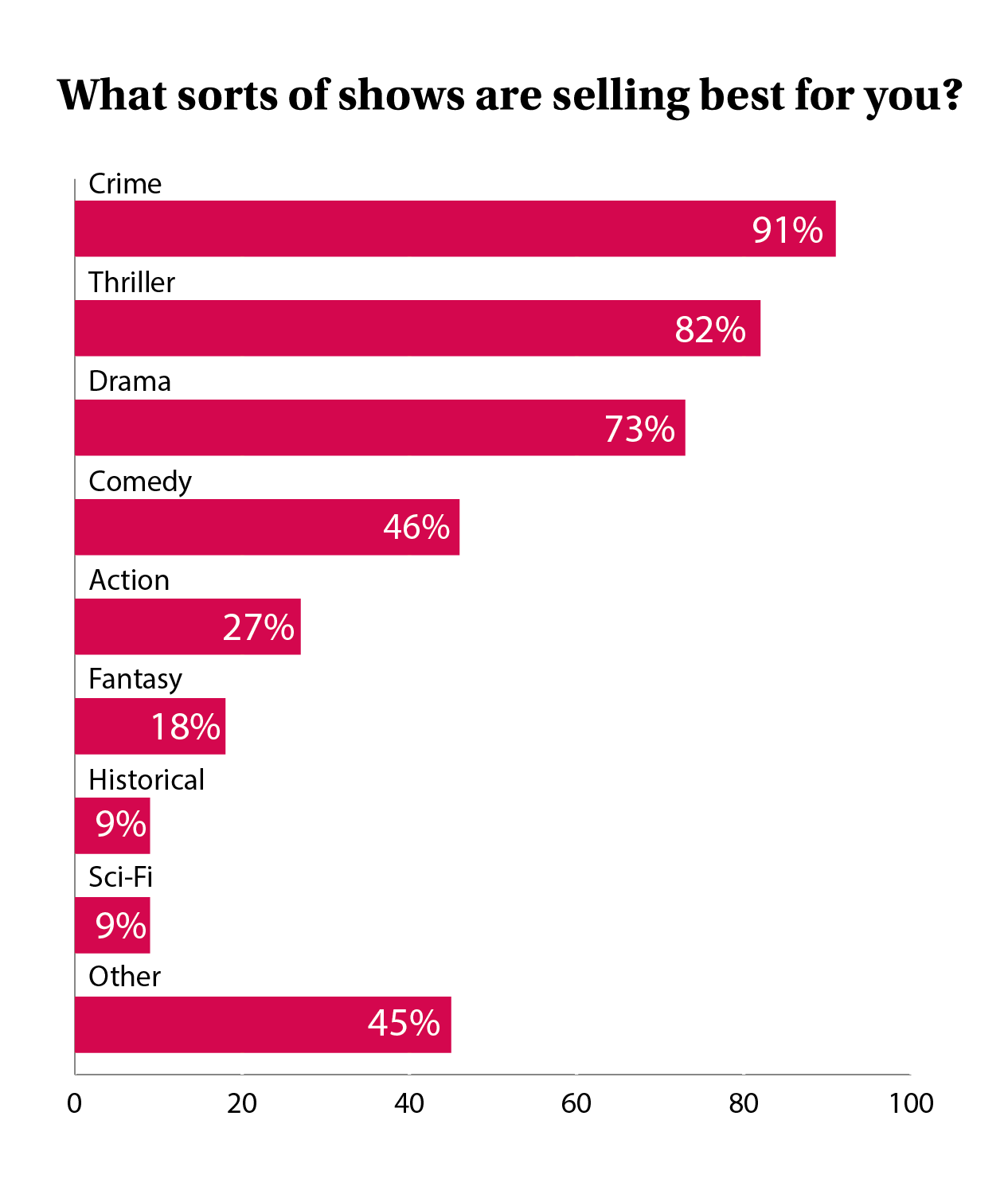

Calling all crime

Fuelling growth this year has been the surging popularity of scripted crime programming: 91% of companies said this genre was among their best-sellers, with thrillers (82%) and relationship dramas (73%) also among the key series travelling internationally.

Comedy and action shows have also performed, named as best-sellers by 46% and 27% of respondents respectively, but romance, mystery and science fiction all underperformed with only 9% of respondents citing the latter as being a key genre.

Comedy and action shows have also performed, named as best-sellers by 46% and 27% of respondents respectively, but romance, mystery and science fiction all underperformed with only 9% of respondents citing the latter as being a key genre.

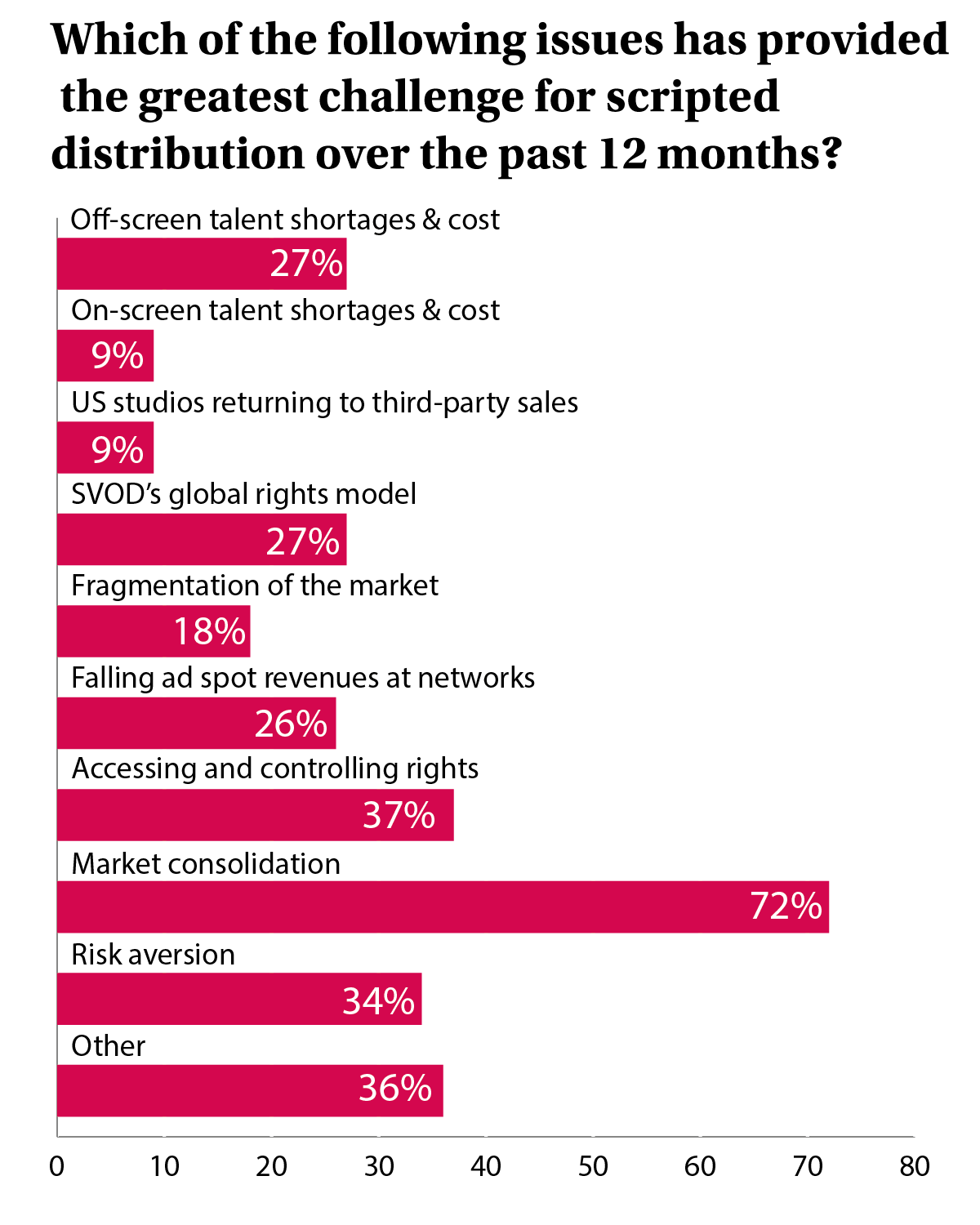

And while almost all companies said their catalogues had got bigger since last year, the issue of market consolidation remains upper most in distributor’s thoughts. Just over 72% of respondents said increased M&A action had made life tougher, with the connected issue of accessing and controlling rights cited by 37% of respondents (who were allowed to answer more than one challenge to their business). Further, 72% are financing scripted series earlier than ever to secure their piece of content.

Other major challenges include risk aversion (34%) and falling ad revenues (26%), along with off-screen talent cost (26%).

Navigating the SVOD stream

Among the most notable themes to have come away from the 2023 Survey is the wholesale shift in expecting growth from global streamers such as Netflix, Max and Paramount+. While 65% of respondents last year said they expected this group of buyers to grow in number in 2022/23, only 9% responded similarly this year, reflecting the ongoing belt-tightening that the industry has seen from players ranging from global operators such as Disney+ to regional operators including Viaplay.

While questions remain over just how profitable FAST will be outside of the US, it remains the sector expected to deliver the most growth in terms of buyers over 2023/24, with 91% of companies taking part in the Survey expecting this largely nascent sector for many parts of the world to expand further.

Yet while the US has embraced FAST and is monetising this emergent sector, much of the world remains several years behind in terms of uptake. This is reflected in this year’s Survey, with 54% of respondents reporting that FAST accounts for around 10% of all revenue, with only 7% claiming a return of between 10-25% of annual revenues.

Away from FAST, there seems to be little expectation of any major shift in buyer numbers, although 24% of respondents are expecting acquisitions execs from regional streamers to also grow in number (respondents could pick more than one group). Less than 8% of respondents believe buyers from pay TV will increase in number.

Expectations

There is optimism that the market will improve, however, with 82% expecting growth and countries including the US, the UK, Australia and Spain among those offering most demand, with regions such as Central and Eastern Europe and the Nordics also cited.

“We are currently facing lots of headwinds with the downturn in the advertising market, consolidation and cuts at the major streamers and studios, the writers’ and actors’ strikes and inflation impacting budgets. However, we are anticipating an upturn, if slow, when these issues start to resolve themselves,” said Mutimer.

“We are currently facing lots of headwinds with the downturn in the advertising market, consolidation and cuts at the major streamers and studios, the writers’ and actors’ strikes and inflation impacting budgets. However, we are anticipating an upturn, if slow, when these issues start to resolve themselves,” said Mutimer.

Staffing levels also look likely to remain largely steady, with 73% reporting no planned changes over the coming 12 months, up from 65% last year, although consolidation will likely see the overall number of roles available slimmed down.

The industry is also seemingly settling back into the more traditional cycle of events, with 74% saying they expect to attend the same number of events in 2024 as they did in the pre-pandemic world of 2019.

MIPCOM remains the industry flagship event, with more than 90% of distributors saying it is a must-attend, while Content London has also become a mainstay for the scripted industry and came second in the rankings. LA Screenings, NATPE Budapest and Asia TV Forum made up the top five places (respondents could pick more than one event).

While travel has largely recovered, online sales platforms are seeing their popularity wane, with 91% reporting no use. Artificial Intelligence, meanwhile, is also being experimented with but Banijay Rights chief Cathy Payne summed up most respondent’s opinions by admitting that while it “provides enhancements and efficiencies in a whole range of processes, it’s important to point out that individual human creativity, development and performance will always lie at the heart of our creative industry.”