Exclusive: TBI Distributor’s Survey 2023 – Part 4: Kids

From FAST growth to pre-financing shows and navigating a consolidated market, the 2023 survey reflects the ability of the distribution industry to adapt to change. With more than 40 responses from sales companies around the world, join us as we discover this year’s key trends.

It has been a year of transition for many in the TV industry. On the buyers’ side, it has been tough: US studios have been coming to terms with the realities of streaming; commercial networks have been adapting to a squeezed advertising market; and public broadcasters have been ducking and diving as they try to stretch budgets. For those on the other side of the transaction, consolidation and risk aversion are very real concerns, but growth areas such as FAST and the ever-increasing importance of distributors in financing are seen as offering considerable potential in a business that has always had to adapt quickly.

Kids: Steady Growth

Children’s content distributors have been expanding their catalogues and increasing their profits over the past 12 months, but changing studio strategies may mean fresh competition in the market

A strong children’s content offering remains vital for global streamers and local broadcasters alike, though depleted budgets and shifting strategies have caused some turbulence in the sector over the past year, TBI’s Distributor Survey has found.

The US studios’ move from locking in their content on D2C services back to the old model of third-party sales does mean further competition, but revenue and profit appears to be steadily growing for these firms (mostly, see below) while maturing AVOD and FAST channels are providing new distribution avenues.

Profit and loss

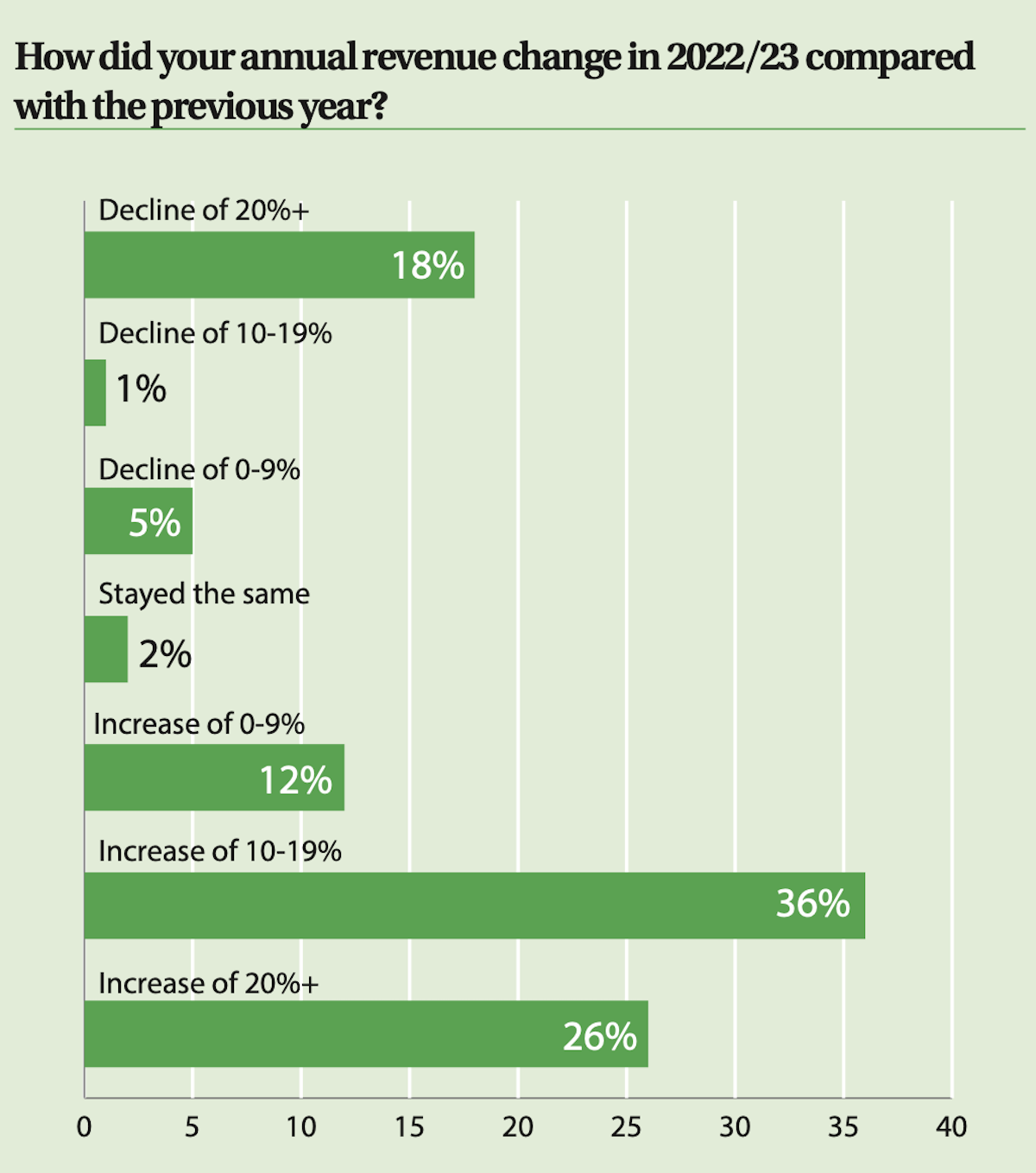

For the most part, kids content distributors reported a healthy 12 months, with three-quarters of all those surveyed reporting that both revenue and profits had risen over the past financial year.

A little over a quarter of respondents (26%) had seen revenue and profits increase by 20% or more, with a further 48% reporting rises of up to 19%. However, it wasn’t all positive news, as a further 18% of respondents said that these figures were down by more than 20% on last year.

Click to expand

This is a step backwards from the results recorded in last year’s Survey, which found that demand for kids’ content had increased revenue and profits for all respondents by around the same percentages as this year, demonstrating roughly consistent growth were it not for the outliers.

While kids’ content clearly remains in high demand, this inconsistency can probably be attributed to several factors, but perhaps most likely the financial strains being felt across the sector and the buyers now playing it safe with their acquisitions.

Indeed, risk aversion was identified as the greatest issue facing kids’ distributors, with 63% of respondents identifying it as one of the greatest challenges of the past 12 months.

Other hurdles highlighted by respondents include market consolidation and the global rights models of streaming services, as well as delayed payments from these clients.

It’s telling then, that looking to the year ahead, a growing number of Survey respondents – 38% in total – are expecting to see declines in revenue of 20% or more, far more than the 18% drops seen over 2022/23. For those predicting revenue growth, the rate of increase expected is lower than last year.

Nevertheless, 77% reported that they have expanded their catalogues in the past year, while 64% said they believe the market will improve in the coming months.

Sharing their reasoning, respondents highlighted the opportunities created by streamers and broadcasters having less budget to spend on original content, the end to structural changes at major commissioners over the past 12 months and optimism that digital ad revenue will increase as audiences continue to shift to new methods of consumption.

“We finally feel that all the streamers have finished their reorganisation and they’re settled in place,” says Monica Levy, co-chief of distribution at Federation Kids & Family, whose sales catalogue includes Spellbound, Theodosia and Find Me In Paris. “We expect the channels will need content and we will be here with our great shows.”

Old competitors

Animation continues to be in higher demand than live action children’s programming, with 76% of respondents reporting that it is selling best. That is no surprise, but it is an increase on figures from last year’s Survey, when around two-thirds of distributors said that animation was more greatly sought.

The US, UK, France and Germany were all named as the biggest buyers of children’s content, while distributors also highlighted a growing demand from the Middle East, as well as steady business from the Nordics and Central and Eastern Europe.

Despite grabbing a generous number of headlines over the past few months, the Hollywood strikes have not had much of an impact of kids’ content distribution and most respondents don’t seem to be expecting any big knock-on effect.

Click to expand

However, some did share their belief that US streamers in need of content will soon turn to distributors from other countries in the coming months as they seek fresh titles for their services.

Keeping the US in mind, 73% of respondents said that they are expecting the US studios to make more product available over the next 12 months than in the previous year.

As one respondent, Sophie Prigent, head of sales for Paris-based Grizzy & The Lemmings and Mystery Lane distributor Hari, noted: “This means new strong competitors will enter the market, taking share in an already crowded space.

“We don’t expect to be significantly impacted because we distribute only our own IPs, for which we have a premium production outfit, and the trust of our partners who wouldn’t consider our content less qualitative or less of an audience-driver.

“That said, output deals with entire slots filled with studio content would be more of an issue as we can’t create airtime that isn’t available anymore.”

New sales avenues

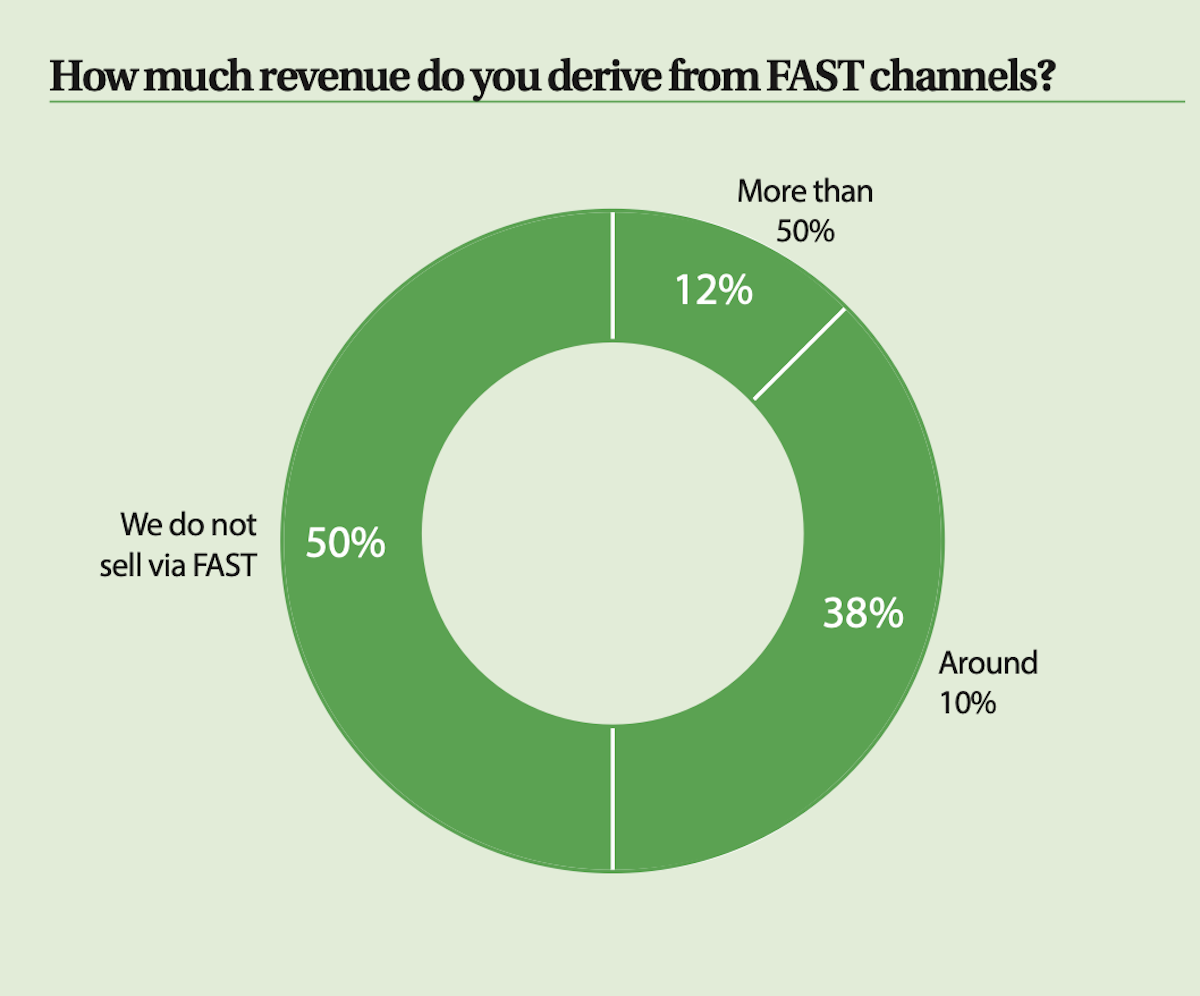

The emergence of FAST is of growing importance to kids’ distributors (read more about this on page 2), with an eyebrow raising 12% of respondents revealing that more than 50% of their revenues come from FAST. A further 38% said they receive around 10% of their revenue from these services but that still leaves 50% who indicated that they do not sell via FAST at all. However, as more services crop up – something 88% of respondents expect to see in the coming year – new distribution avenues will increase further opening up.

AVOD, meanwhile, is bringing in 10% revenue or more for 77% of kids’ distributors, with 26% revealing that AVOD services contribute more than 50% of their revenue. And it was a fairly even split when it came to windowing, with 51% of firms selling more windows than they were last year.

Claudia Scott-Hansen, principal at Cookbook Media, highlighted that: “AVOD platforms are picking up where linear & SVODs are not supporting shows (for example, limited launches, no promotions or reduced episodes).”

Prigent at Hari, meanwhile, added: “It really depends on the accessibility and popularity of the partners we work with. When thinking about pan-regional players, their penetration sometimes varies from one market to another. The combination of several windows is what really matters. That said, AVOD & FVOD are increasingly significant also because they provide immediate data.”

MIPCOM remains the most important market for children’s distributors, with every respondent marking it as a must-attend event. However, MIPTV is seen as less vital, with only around half of the respondents rating it one of their most important markets, trailing Kidscreen (88%) and Annecy International Animation Festival (63%).