TBI Tech & Analysis: Unpacking how streaming revenue will reach $569bn by 2028

Global online video services will continue to make massive revenue gains over the next five years, but it’s a different picture for pay-TV, reveals Omdia analyst Adam Thomas, as he delves into the numbers for the years ahead.

Last year was a highly significant one for online video. The sector’s “mood music” changed from the vigorous chasing of subscription growth to belt-tightening and searching for profitability—a mood change initiated by the unprecedented subscription losses experienced by Netflix in 1H22.

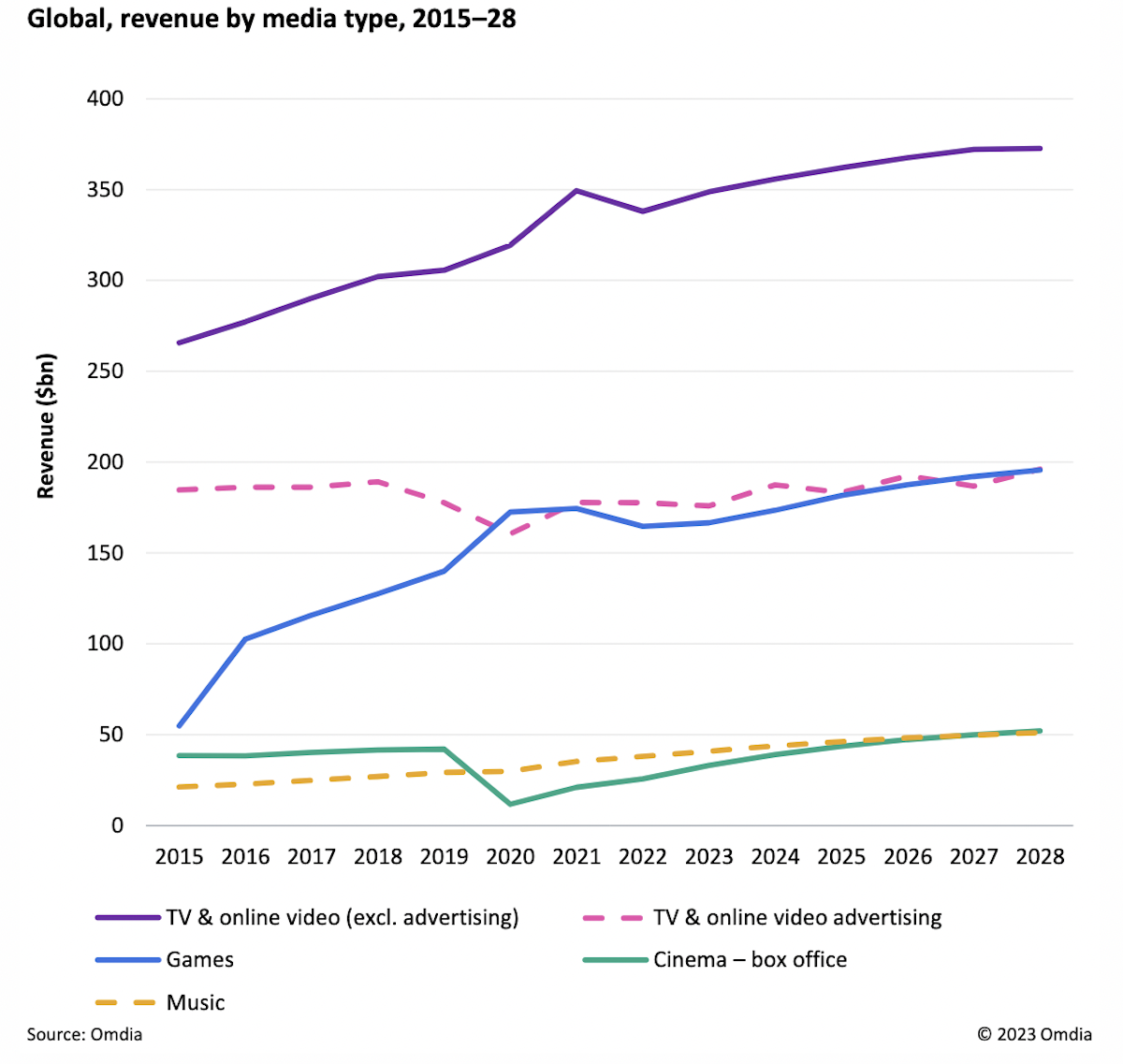

Against this backdrop, combined global revenue for the traditional TV and online video sectors totaled $516bn in 2022. Omdia is forecasting that figure to grow to $569bn in 2028, representing a CAGR (compound annual growth rate) of 1.7%. These numbers include advertising revenue from premium AVOD/FAST services but exclude social video advertising (e.g., YouTube, Meta, TikTok) and other types of online video advertising (e.g., in-banner video or CTV UI video advertising).

Of the individual components making up the TV/video total, the swiftest growth comes from ad-supported online video, with revenue of $24.6bn in 2022 growing at a CAGR of 14.3% to $55.1bn in 2028. Looking at the paid-for services most closely featured in the multisubscription research, it can be seen that online channel (SVOD) services generated $85.5bn in 2022, a figure Omdia forecasts to reach $129.2bn in 2028 (a 7.1% CAGR).

Traditional pay-TV subscription and on-demand revenue is forecast to decline from $197.6bn in 2022 to $177.5bn in 2028.

To put the figures quoted above in a wider media context, games revenue is forecast to increase at a 2.9% CAGR over the forecast period compared with 5.1% for the music sector and 12.6% for cinema box office revenue.

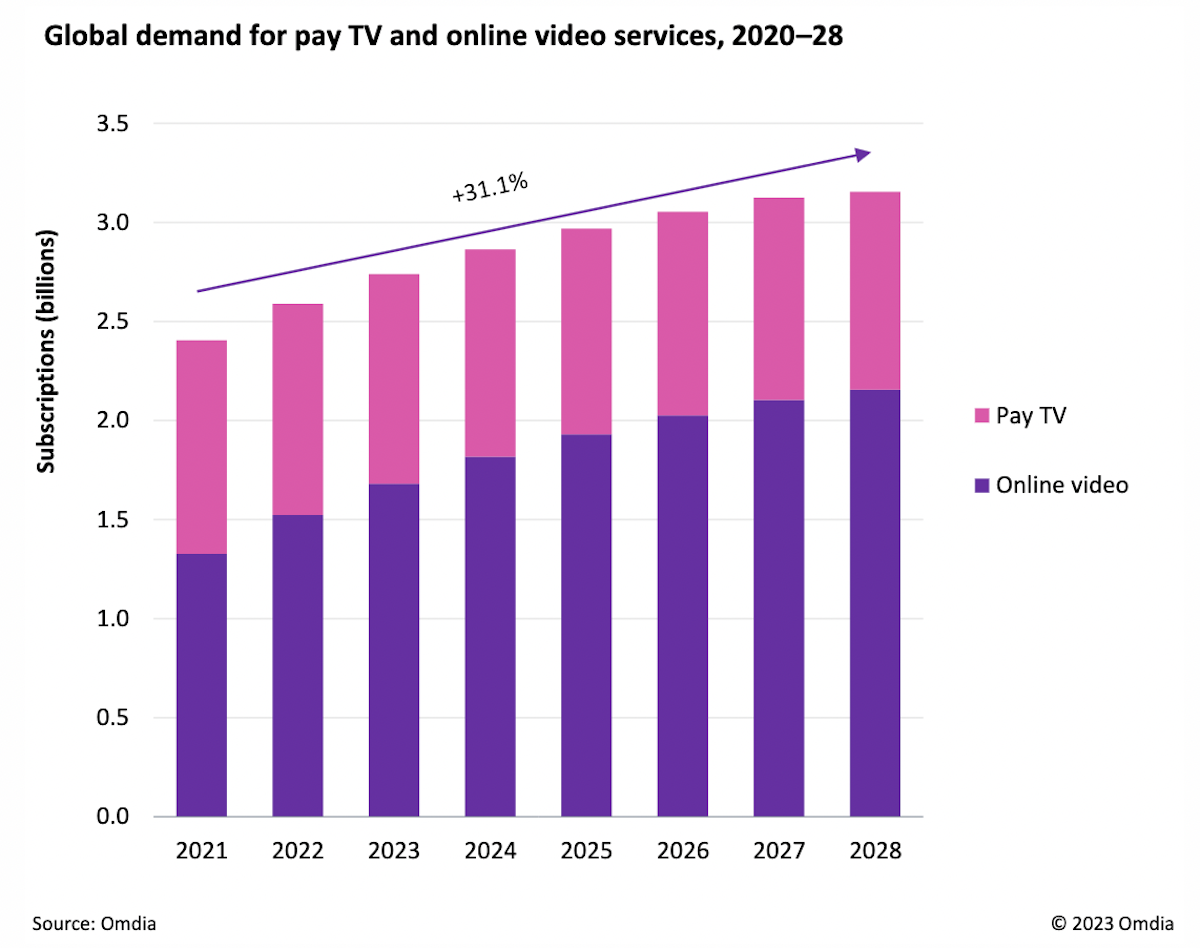

Online video subscription numbers to grow

In 2021, there were 2.4 billion online video and pay-TV subscriptions worldwide. That total increased to almost 2.6 billion in 2022 and is on track to end 2023 at a figure well above 2.7 billion. Despite moves to focus on profitability rather than growing subscription scale, Omdia sees no imminent end to this growth trend, with the public remaining keen to consume TV and video. Omdia’s current forecast is for ongoing significant increases to take the total over 3.1 billion by the end of 2028.

Over the 2021–28 period, TV/video combined subscription numbers will increase by more than 31%, but all the growth will come from online video. Pay-TV subscription numbers will decrease by 7.4% during that period (from 1.079 billion to 999 million), and online video subscriptions will increase from 1.327 billion to 2.156 billion, a 62.5% increase.

This picture of ongoing subscription growth for online video is a positive one, but it is tempered by the reality that the growing proportion of lower-ARPU online video subscriptions means that the revenue growth being generated is lower than would have been experienced if traditional pay-TV ARPU levels had been maintained.

Pay-TV is in decline, although significant differences are experienced by platform, with cable-TV subscription numbers falling by 8.5% during 2021–28, while satellite TV’s fall by 7.3% and IPTV’s increase by 10.6%

The exceprt above is taken from Omdia’s ‘Multisubscription TV & Video Forecast Report: 2015–28’, which is available to read in full here (subscription required). Adam Thomas is senior principal analyst for TV & Online Video at Omdia, which is part of Informa, as is TBI.