After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: Behind Netflix’s sub-Saharan Africa growth

With MIP Africa kicking off today, Omdia’s research analyst Samuel Nkwam explores how Netflix is seizing the opportunities for growth in sub-Saharan Africa.

As market saturation occurs in many developed regions of the world, sub-Saharan Africa is seen as the last frontier for OTT video growth, given low current penetration rates, a favorable demographic profile, expanding smartphone adoption, and deepening mobile payment infrastructure.

Subscriptions are concentrated in a few major markets, namely South Africa, Kenya, and Nigeria, with South Africa being the most important market in the sub-Sahara region for online video. These countries accounted for 85.9% of total SVOD subscriptions in the region in 2022, driven by higher household broadband penetration rates, larger consumer purchasing power in these nations, and sizeable domestic markets.

The OTT video market opportunity has not only lured in the larger international platforms such as Netflix but has spawned an increase in indigenous operators too. Aggressive content localization, new pricing structures and payment options, and decisions from the multinational platforms to adopt loss-leading strategies in the pursuit of new OTT subscribers in emerging markets, have all been key factors in the recent rapid growth of online video in Africa.

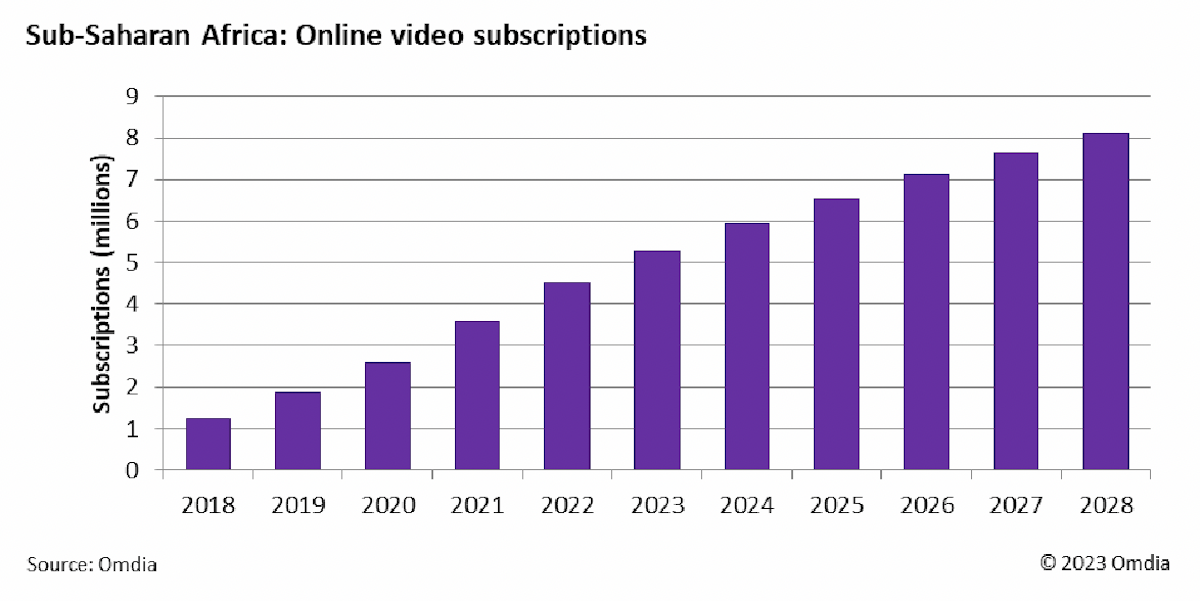

Online video subscriptions in sub-Saharan Africa grew 259.5% between 2018 and 2022, and Omdia is forecasting that subscription numbers will rise at a CAGR (compound annual growth rate) of 10.4% to over 8.1 million by end-2028.

Netflix numbers

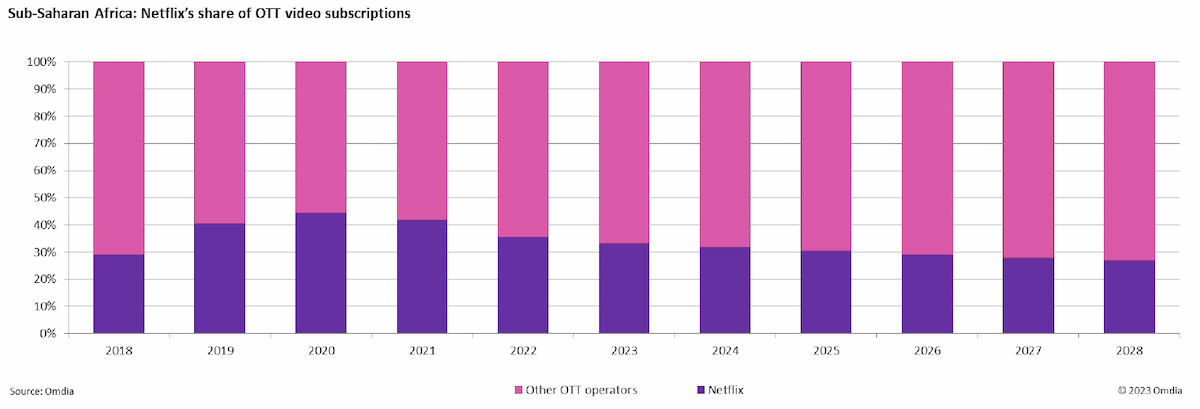

Netflix subscription numbers in sub-Saharan Africa rose by 6.8% between 2021 and 2022, reaching almost 1.6 million by the end of the year. Subscription revenue exceeded $135m in 2022, an increase of 13.7% from 2021. However, increasing competition saw the company’s share of total OTT video subscriptions fall from 41.8% to 35.6% during the same period. Netflix has set its sights on the fast-growing OTT opportunity in the region, having invested over $175m in sub-Saharan Africa since 2016, creating 12,000 jobs in South Africa, Nigeria, and Kenya alone.

Netflix has faced mounting pressure from shareholders due to stagnating subscriber growth in its more mature markets, but it has seen rapid growth in Africa and is second only to Showmax in terms of subscriptions in the sub-Sahara region. Following its launch in sub-Saharan Africa in 2016, Netflix subscriptions had risen to almost 1.6 million by end-2022 and Omdia is expecting subscriptions to rise at a CAGR of 5.5% to 2.2 million by 2028. This is below the overall market, forecast to increase at a CAGR of 10.4%, as new and smaller operators are expected to capture a bigger portion of Netflix’s market share of future subscriptions.

South Africa, Nigeria, and Kenya are key markets for Netflix in the region, representing over 87% of the service’s regional subscriber base in 2022. Netflix offers a mobile-only tier across several markets in Africa and launched a completely free tier in Kenya in September 2021, due to payment facilitation obstacles.

As many pay-TV operators in the region such as MultiChoice and StarTimes have been forced to raise prices due to spiraling inflation, Netflix has bucked the trend by implementing a slew of price cuts across several markets in Africa in 1Q23, as competition from established players and newer OTT platforms heats up in the region. Omdia forecasts that Netflix subscription revenue will exceed $172m by 2028.

The exceprt above is taken from Omdia’s ‘The Growth of Netflix in Sub-Saharan Africa’ report, which is available to read in full here (subscription required). Samuel Nkwam is research analyst for TV & Online Video at Omdia, which is part of Informa, as is TBI.