After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: Why M&A activity doubled in two years

Little Fires Everywhere

The global TV industry is streamlining, with a sharp uptick in M&A activity over the past 12 months. Mark Layton digs into the numbers to see who is spending the most, where and on what.

In the past 12 months it has felt like barely a week has passed without an acquisition deal of one kind or another in the headlines – from production powerhouses recruiting small firms to expanding rosters to media giants sending out global shockwaves as they slam together, up-ending old regimes.

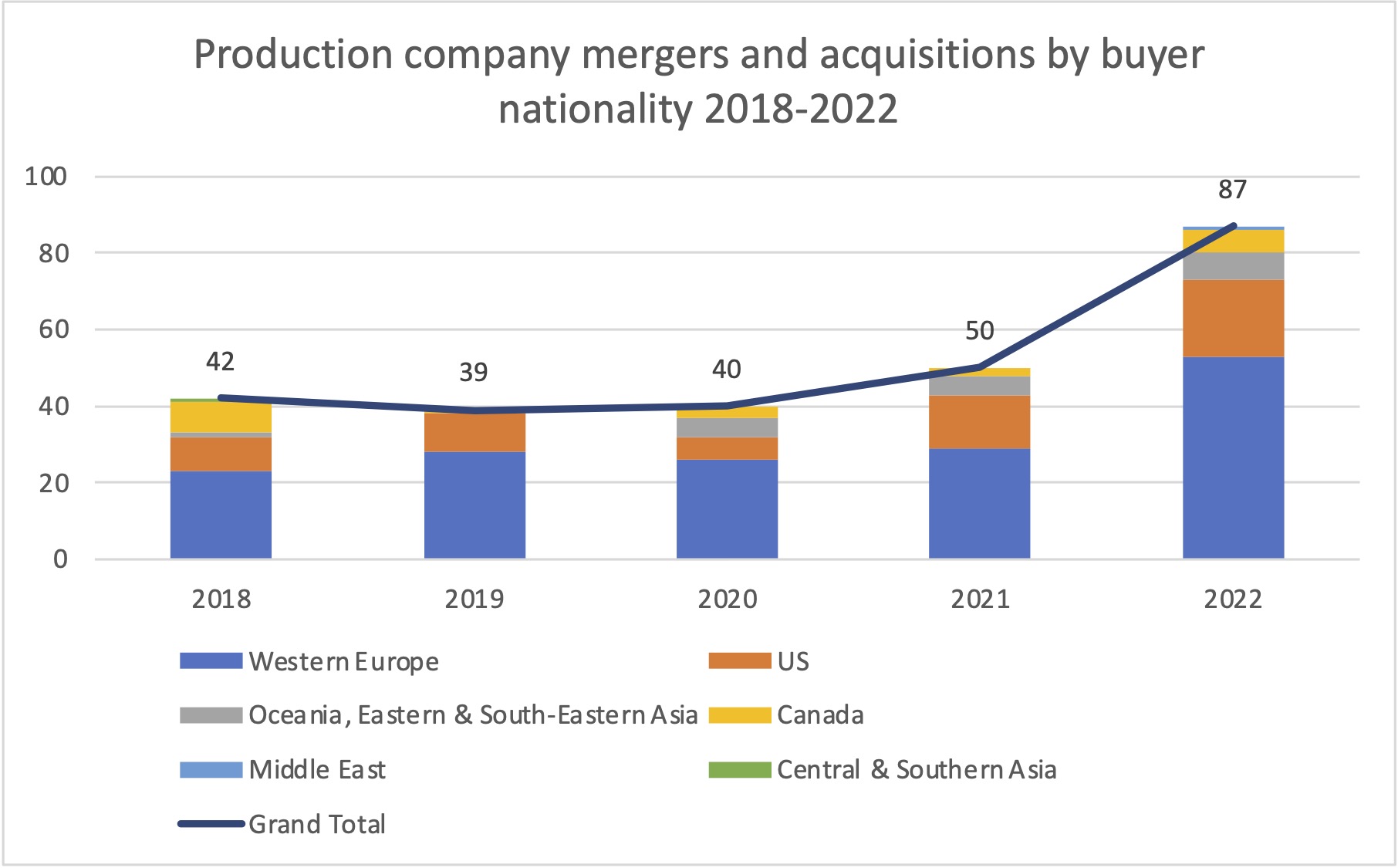

If you need some hard statistics to tell you what you already suspect, then yes, 2022 was the biggest year for TV production mergers and acquisitions for several years – since 2017, in fact, with 87 deals tracked by TBI’s sister research firm Omdia over the 12 month period.

All this activity marked a sudden jump from the 50 deals recorded in 2021 and 40 in 2020 and, for the most part, it’s been taking place in western Europe, with France overtaking the UK as the leading nationality of company buyers. Paris-headquartered Banijay’s acquisition of Australian producer and distributor Beyond International is just the latest major deal to emerge from the company in recent months.

In total, there were 53 M&A transactions with western European companies as the buyers in 2022, compared to 20 from the US, in the same period. Of these, the UK has consistently been the most targeted country for M&A deals, with 24 companies acquired during the year, compared to 17 based in the US and six apiece in France and Italy.

In total, there were 53 M&A transactions with western European companies as the buyers in 2022, compared to 20 from the US

Banijay Group has been the most active in building its portfolio of production companies. The acquisition of Big Brother and Deal Or No Deal firm Endemol Shine from Walt Disney and Apollo Capital Management in 2020 made the French company the largest producer outside the US major studios by revenue, though other French outfits, such as Asacha Media Group, Mediawan and Newen Studios have also been busy in the acquisition market over the past five years.

Private equity companies have also taken an interest in the sector and have been prepared to put their chequebooks on the line in a big way. In France, Asacha Media Group, has been backed by Oaktree, while Blackstone is one of the major investors in Candle Media, which has snapped up companies including Reece Witherspoon’s Little Fires Everywhere producer Hello Sunshine and UK-based Moonbug Entertainment, the CoComelon firm, which it snapped up in a $3bn deal in 2021.

While western Europe is making the biggest number of deals, these big price tags have tended to be attached to US-based acqusitions numbers, with Amazon’s deal to get its hands on MGM Studios from Anchorage Capital last year valued at $8.5bn.

Click to expand

Meanwhile, NBCUniversal’s acquisition of DreamWorks Animation in 2016 was valued at $3.8 bn, while Hasbro paid $4.6bn for Entertainment One in 2019 to speed its transformation from a toy company – although the firm seems ready to divest itself of the Yellowjackets firm just a few years on.

As to the why of all this M&A activity, one of the key drivers has been the increase in original programming commissions by streaming platforms, in particular Netflix. Many of these companies are now trying to bring about a major change – such as an increase in scripted production or to secure more creative talent.

According to Omdia, the coming year may see a change in this behaviour, as industry giants Warner Bros. Discovery and Disney have both announced plans to cut back on programming investment to rein in losses on their D2C platforms.

The research group says to keep eyes, once again, on western Europe – in particular on BBC Studios and Fremantle – both of which have set ambitious growth targets and may be the most acquisitive groups in the next few years.

These figures were sourced from the TV Production Company M&A Tracker, available as part of Omdia’s Digital Content & Channels Intelligence Service.