TBI Tech & Analysis: Forecasting Eastern Europe’s pay-TV staying power

Click to expand

Online video is growing much faster in Eastern Europe than pay-TV services, but the latter is still dominating the market – and will do for some time to come. Omdia’s Matthew Evenson, research analyst, TV and video, and Irina Kornilova, practice leader, TV and video, dig into the numbers.

Continuing the trend seen over recent years, online video saw greater growth than pay-TV in terms of both subscriptions and revenue. However, it remains far behind pay-TV, which continues to show significant resilience in the face of increased competition from an array of new local and global players.

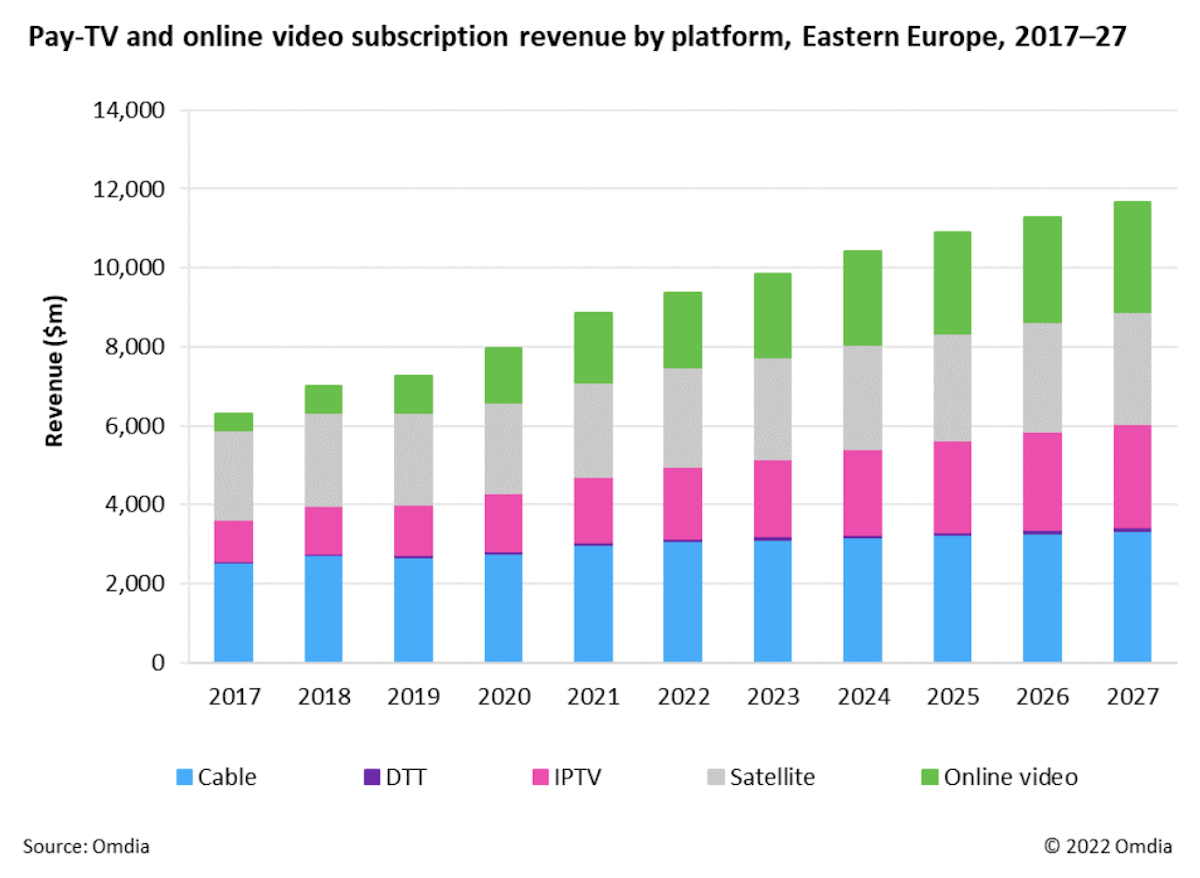

In 2021, pay-TV accounted for 74.3% of all video subscriptions, dropping below the 75% mark for the first time from equivalent 2020 and 2019 figures of 77.8% and 83%, respectively. For the financial year 2021, pay–TV revenue in Eastern Europe totalled $7.22bn, up 7.7% on 2020’s total of $6.70bn. In contrast, total online video revenue for the region grew 32.6% from $2.46bn to $3.26bn.

Although online video continues to catch up with pay-TV, the latter still accounted for 68.9% of total market revenue in 2021. This figure will drop as online video revenue continues to make gains. However, pay-TV’s resilience will see it retain a 65.7% share of total market revenue in 2027.

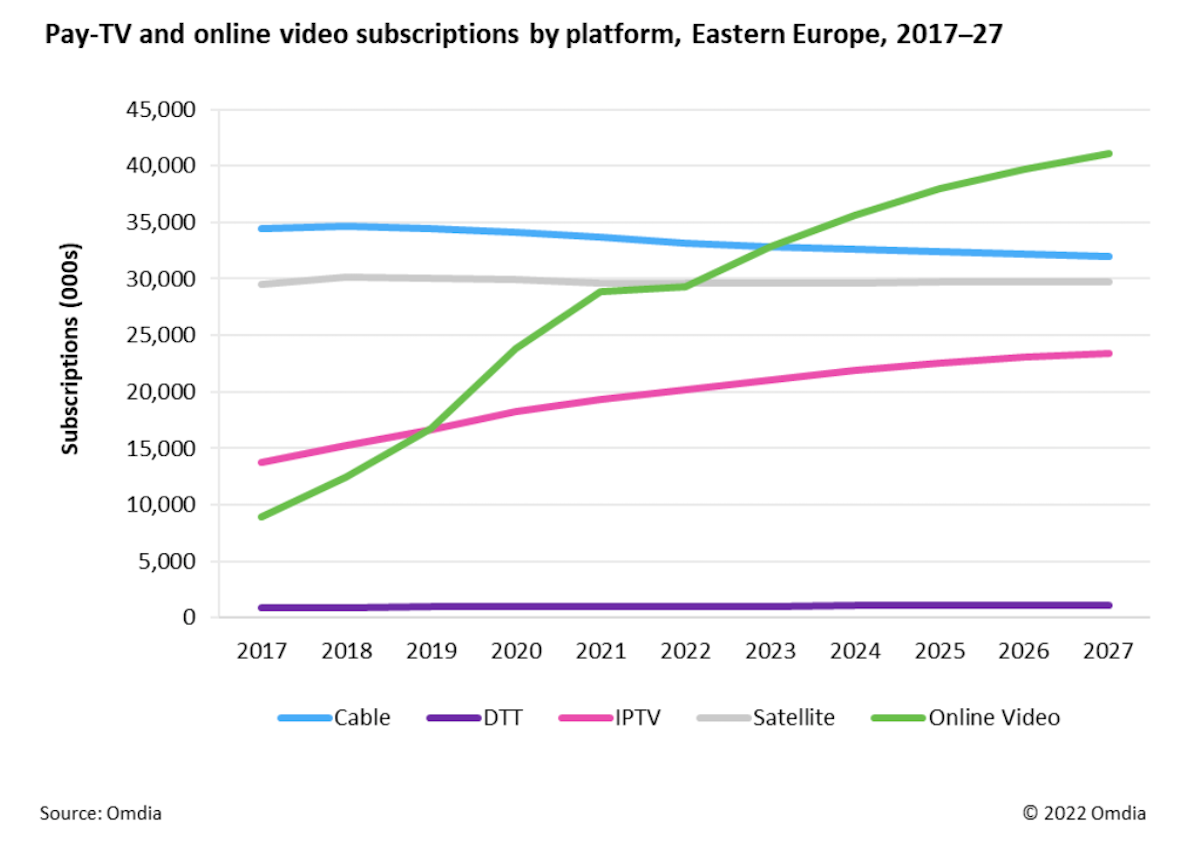

Subscription growth, as with revenue, is stronger in online video than in pay-TV. A year on from the main period of isolation due to the coronavirus pandemic, online video subscriptions grew 21.4% in 2021 versus 41.8% in 2020. Even with this slow down in growth, online video subscriptions reached almost 29 million in 2021—more than double the number of subscriptions three years prior in 2018 (12.46 million)

Click to expand

IPTV in the lead

As in 2020, cable TV remains the largest individual viewing platform in terms of the number of subscriptions in 2021, with more than 33.7 million across the region, down

1.3% from 2020.

The number of cable–TV subscriptions will continue to decline through the forecast period by 5% between 2021 and 2027 to just less than 32 million.

IPTV is the fastest–growing pay–TV platform, with subscriptions growing 5.9% in 2021 to almost 19.4 million. Subscriptions will reach more than 23.4 million by 2027, but IPTV will still sit behind satellite and cable.

The number of online video subscriptions continues to grow after reaching almost 29 million in 2021, an increase of 21.4% on 2020. It is currently forecast to surpass cable as the single largest viewing platform by 2024, and subscriptions are forecasted to cross the 40 million mark by 2027.

Video subscription revenue growth reflects the growth seen in subscriptions. A 27.7% growth in online video subscription revenue in 2021 helped to push total market

subscription revenue to $8.87bn in 2021, up from $7.97bn in 2020.

Despite the fall in subscriptions, cable–TV subscription revenue rose to $2.98bn, up 7.1% on from $2.78bn in 2020. The year saw a return to growth for satellite

subscription revenue after a minor decrease in 2020, rising 4.7% to $2.41bn.

Of the pay–TV platforms, subscription revenue for IPTV grew the strongest, up 13.9% to $1.66bn in 2021. IPTV also had the highest subscription ARPU of $7.33 per month in 2021. Despite the growing presence of new and existing online video services, ARPU for all pay–TV platforms grew in 2021 with increases of between 5.5% and 8.5% from 2020.

The extract above is from Pay TV & Online Video Report: Eastern Europe – 2022, from Omdia’s Matthew Evenson and Irina Kornilova. To find out more, click here.