TBI Tech & Analysis: Picking out pay TV patterns in North America

Pay TV in North America is a market in decline, yet revenues remain higher than those of online video subscriptions. Sarah Henschel, principal analyst for media & entertainment at research firm Omdia, tells TBI what to expect next.

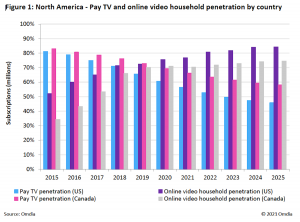

Rewind six years, and the pay TV penetration rates in the US and Canada both stood stood above 80%.

By the end of 2020, the trend of decline had seen rates fall to 61% in the US and 69% in Canada, as viewers migrated to online services.

In North America, there were 298.1m SVOD subscriptions at the end of 2020 or, to put it another way, a 35% increase year on year. Pay TV subscriptions, meanwhile, declined 7% and as online subscriptions boom, revenues struggle to match traditional pay TV.

Pay’s revenue raising capability

However, while the number of online video subscriptions are about 3.5 times greater than the number of pay TV subscriptions in North America, revenues have yet to converge.

However, while the number of online video subscriptions are about 3.5 times greater than the number of pay TV subscriptions in North America, revenues have yet to converge.

As seen in the chart to the right, online video subscriptions surpassed pay TV

subscriptions back in 2016, yet online video revenue will not cross pay TV within the forecast period.

Subscriber growth in 2020 came both from new additions and a reduction in churn for streaming services like Netflix, Amazon, and Disney+.

With school closures, there was a particular spike in demand for children, family, and educational content; brands offering this type of content benefited the most.

At the same time, suspended sports seasons created a gap in sports content availability, which disadvantaged sports-focused subscription providers across both pay TV and online video segments.

However, summertime sports leagues later adapted to safety restrictions and found ways to host shorter or adjusted seasons.

Unlike other regions, North American sports and ESPN are part of basic and extended basic cable packages, keeping basic pricing propped up high. This creates greater implications for higher cord-cutting and the desire for consumers to build their own content packages with virtual pay TV or just SVOD services.

Cinema closures also created an opportunity to test unconventional windowing strategies in VOD and SVOD. With this opportunity came the flexibility to not be held to exhibitor relationships but also the pressure to earn revenue in a year where cinema losses will be significant.

As studios grappled with this issue, their new direct-to-consumer SVOD assets became new first-run options for film and TV content. Disney+, HBO Max, Paramount+, and Peacock have all tried or slated title tests because of this.

Dialling down pay TV

Looking further head, by 2025 it is expected that US pay TV penetration will decline to 46% and online video household penetration is expected to reach 84%.

(Click to expand)

Across the board, Covid-19 and stay-at-home orders throughout 2020 expedited consumer behaviour trends. Growth in online delivery and online retail spiked as consumers learned to lean on online platforms for groceries, contact with friends and relatives, and entertainment within the home.

Any industries that relied on technology and connectivity blossomed, whereas in-person consumption and activities plummeted.

Applying this to media, consumers more quickly leaned into existing trends like cord-cutting and adding SVOD subscriptions to their household. They dabbled further in advertising video services and opted for digital electronic sell-through (EST) and VOD over physical video.

While online video penetration is almost synonymous with broadband penetration, online video household penetration in the US and Canada reached 76% and 71%, respectively, in 2020. Canada typically lags a bit behind the US in terms of penetration rates because regulations often favour larger media conglomerates that continue to prioritise pay TV.

As mentioned, pay TV penetration in the US and Canada was 61% and 69%, respectively, by the end of 2020. By 2025, that rate is expected to fall to 46% in the US and 58% in Canada.

However, as consumers move away from pay TV subscriptions, their content needs must be supplemented with multiple over-the-top (OTT) subscriptions to match the quantity of content available on linear.

Sarah Henschel is principal analyst for media & entertainment at Omdia, which like TBI is part of Informa. The excerpt above is from Pay TV & Online Video Report: North America – 2021, an extensive report into the state of the sector. To read in full, click here.