After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Weekly: Navigating the changing world of buyers

The Mandalorian

Streamers dominate the headlines with big budget originals, but delve deeper and it’s spending on acquisitions that has soared over the past decade, to the tune of $38bn in 2020.

This is just one of the findings from The New Buyers report, which TBI has gained exclusive access to. Here are five key takeaways that underline the wide-ranging opportunities and changing nature of the current content landscape.

Acquisitions adding up

Global investment in acquired content from English-language markets has been growing steadily for the past decade, doubling in spend since 2011 to reach $38bn in 2020, and making up more than a third of spending on non-sport content.

This trajectory is only expected to continue, with acquired programming predicted to top originals spending at some point within the next five years, according to The New Buyers report, which was commissioned by funding & distribution firm Drive and compiled by WorkShare Consulting.

While competition between the major players is identified as the primary driver, there are other factors too, such as the rising per-hour costs of production in countries such as the UK, while total spend has remained the same – further underscoring the value of finished tape.

With an increasing number of traditional media companies entering the VOD space – with the launches of the likes of Discovery+, Paramount+ and HBO Max to name a few – the importance of acquired programming will continue to rise, with subscribers on the whole spending most of their viewing hours consuming library content. VOD numbers, the report found, had risen by 32% over the past four years, from 2,270 in 2017 to 3,015 in 2020.

Disney is among the major players to have made big investments in acquired content, doubling its spend over the last five years, in what is predicted to be a lasting change to its content strategy. With tentpole originals – shows like The Mandalorian and Loki in the case of Disney+ – bringing in new subscribers for the moment, the coming decade will see maturing VOD services turning their focus to customer retention via the library content viewers enjoy. Worth also noting that in 2020, only two of the top 10 Netflix shows (in terms of minutes watched) were originals – The Umbrella Academy and In The Dark).

Niche’s mainstream appeal

Niche’s mainstream appeal

As noted above, the number of VOD services has soared over recent years and niche streamers are now superserving their respective fans a smorgasbord of tightly focused programming – be it about royal families or dogs.

On a broader level, it appears the landscape of traditional linear channels – spanning from large, generalist channels to niche, very specific ones – is now being seen in the world of OTT. Thematic and niche services have shown “strong growth over the past few years,” the report notes, adding that as service aggregation continues, the “fragmented end of the industry composed of small services may grow proportionally faster than the rest.”

While many of these services may merge or close, the prediction is that yet-to-launch services will ensure that the “small player end of the market remains dynamic and responsive”.

Netflix & chill, and repeat…

The shift to streaming content has been largely dominated by subscription-backed services, most notably Netflix, and that on-demand viewing trend is going one way. In the UK, for example, the number of homes signing up to an SVOD surpassed those taking pay-TV in 2019. Now, SVOD homes are greater than pay-TV ever achieved, even at its peak.

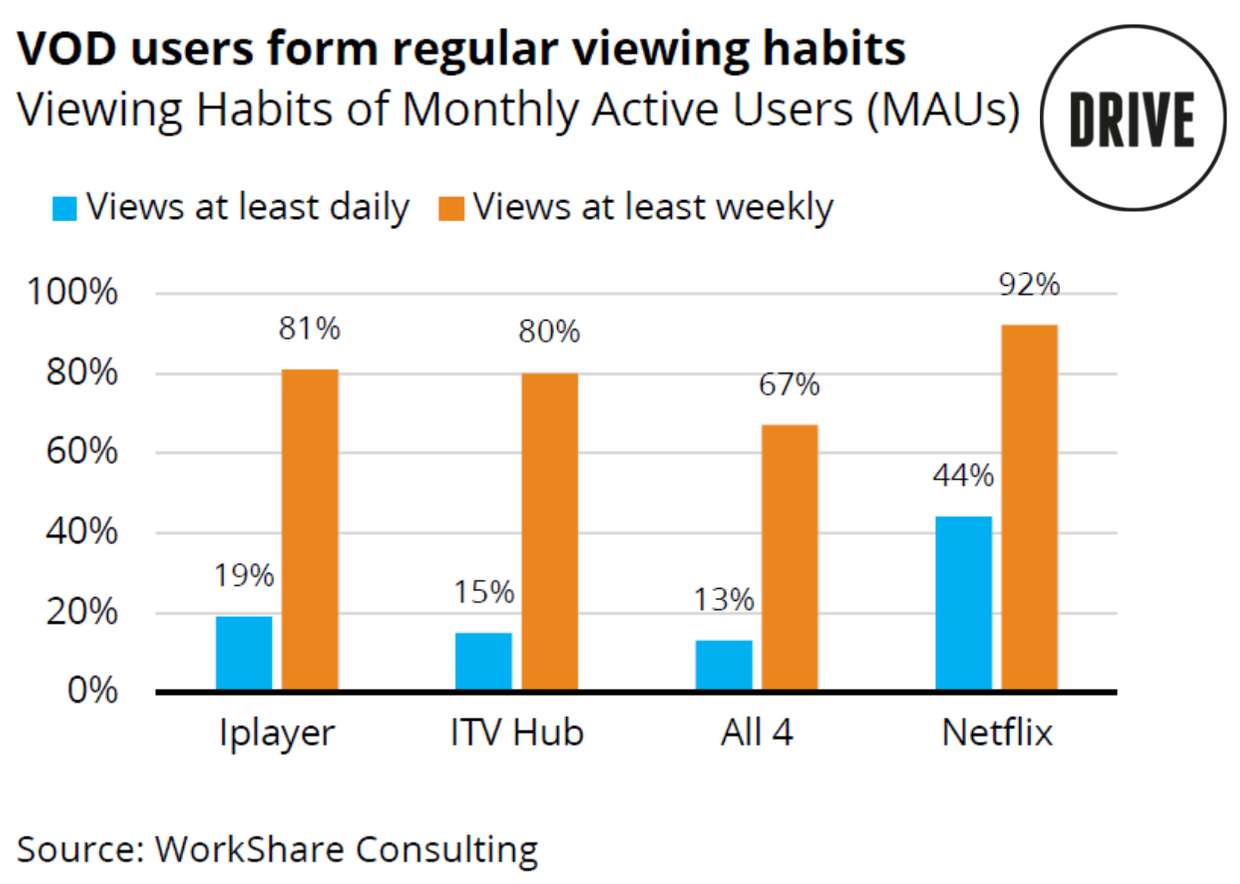

What is now emerging, however, is the habit-forming qualities of an SVOD such as Netflix, over the streaming services offered by once linear-focused broadcasters, such as the BBC or ITV in the UK. “There is a notable difference in the daily viewing of iPlayer and Netflix, despite the fact that weekly views are similar and monthly reach is roughly the same,” the report points out.

… but AVOD makes more revenue

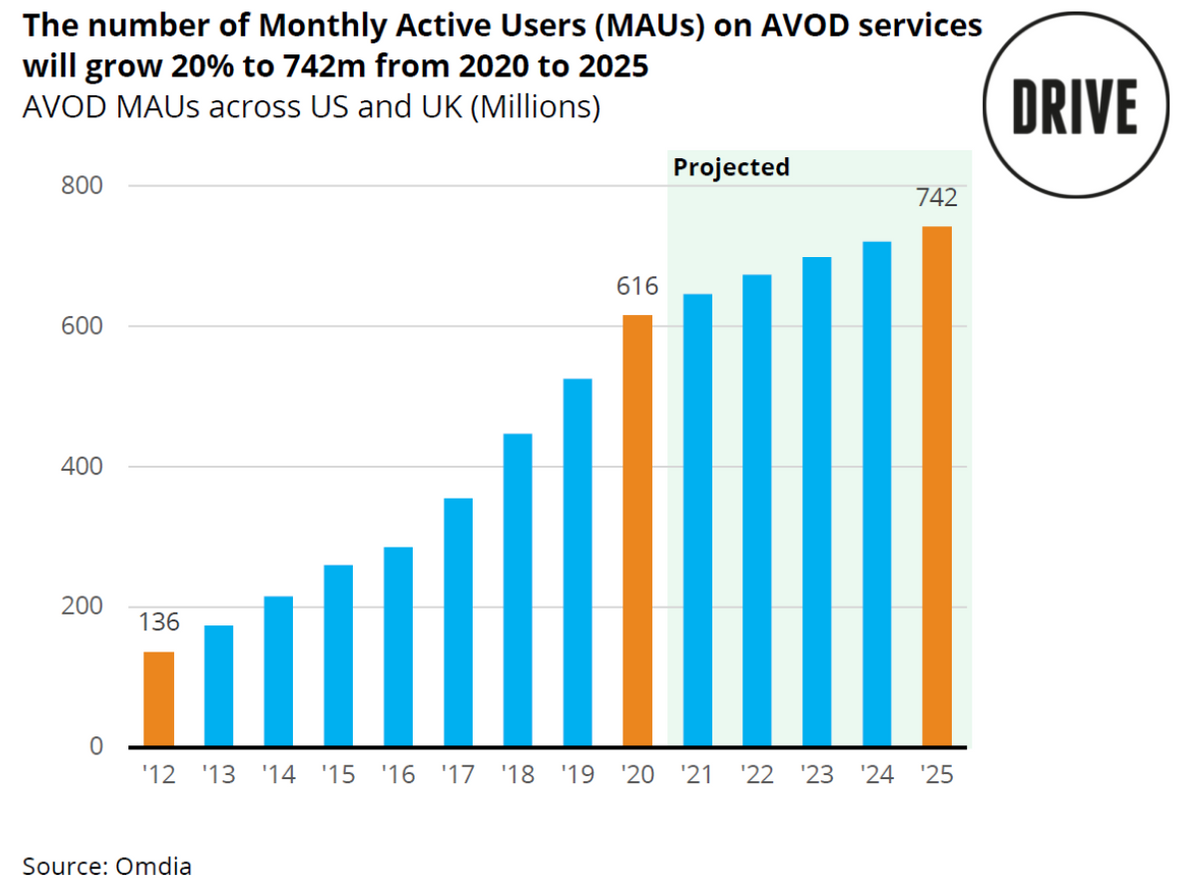

Yet it is the relatively recent emergence of AVOD that seems to be a better revenue generator, something that has been true for years but which is now extending its lead. In the UK and US, AVOD ‘Monthly Active Users’ (MAU’s) has passed 600 million across the various ad-supported services available, but more importantly those watching seem happier to watch commercials as they might on an ad-funded linear service.

The result is bigger gains for AVOD firms. Roku, for example, has been using this growth to expand rapidly and move into ‘originals’ (of a sort) after acquiring Quibi’s library, while the trend is also neatly highlighted by YouTube. Its revenue has roughly doubled in two years, growing from $11bn in 2018 to $19.8bn in 2020. Viewing, meanwhile, is estimated to have grown at a “much more gentle” rate of 15-20%, the report notes.

Escape & comfort rule

Much was made during the latter half of 2020 about the pandemic’s effect on viewing habits, mainly the demand for content that took audiences out of their locked down bubbles.

The report highlights this, with animal, children’s and comedy programming all experiencing a sudden surge in demand in the UK during Q2 2020, while politics and BLM protests stoked interest in US-related shows.

More recently, demand has emerged for competition and celebrity series, while Coronavirus themed or related programming peaked in Q2 2020, where for that quarter it represented nearly 8% of all commissions.

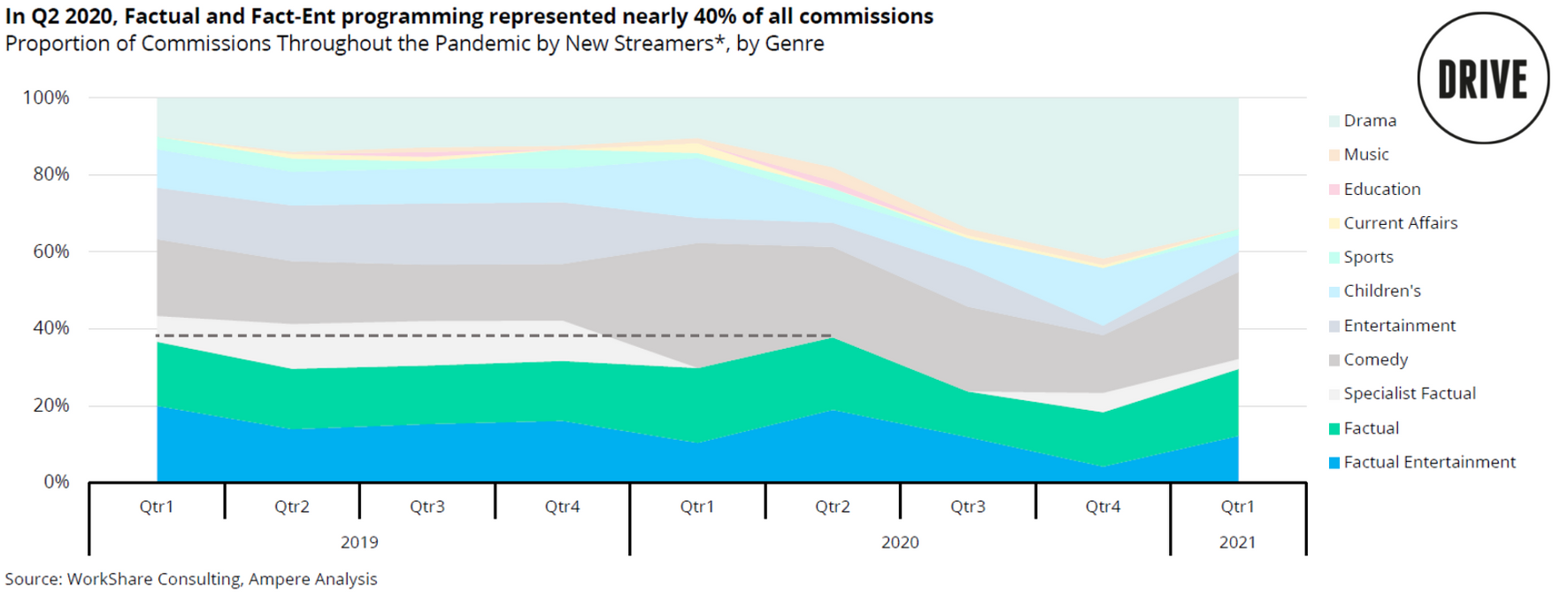

The report also details the peaks and troughs experienced by producers last year, as the pandemic hit, with drama particularly affected by restrictions. Factual and factual ent producers, however, were better able to navigate the regulations and in Q2 2020, these genres represented nearly 40% of all commissions.