After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: Unpacking the $70bn+ online video ad market

Last week, we explored the huge potential of the global video advertising market, with revenues expected to hit $120bn by the end of 2024. Now, we take a deeper dive to find out how the sector is changing in specific countries with analysis from research powerhouse and TBI sibling, Omdia.

As we have already discovered, global online video ad revenues will grow from $70bn in 2020 to reach $120bn by the end of 2024, providing huge opportunity for those operating across the sector.

Driven by the post Covid-19 online video consumption surge that is here to stay, video (including in-stream and out-stream), will account for 52% of online display advertising revenue by the end of 2024, growing from 47% in 2020. Here, we explore the potential in four markets.

(Click to expand)

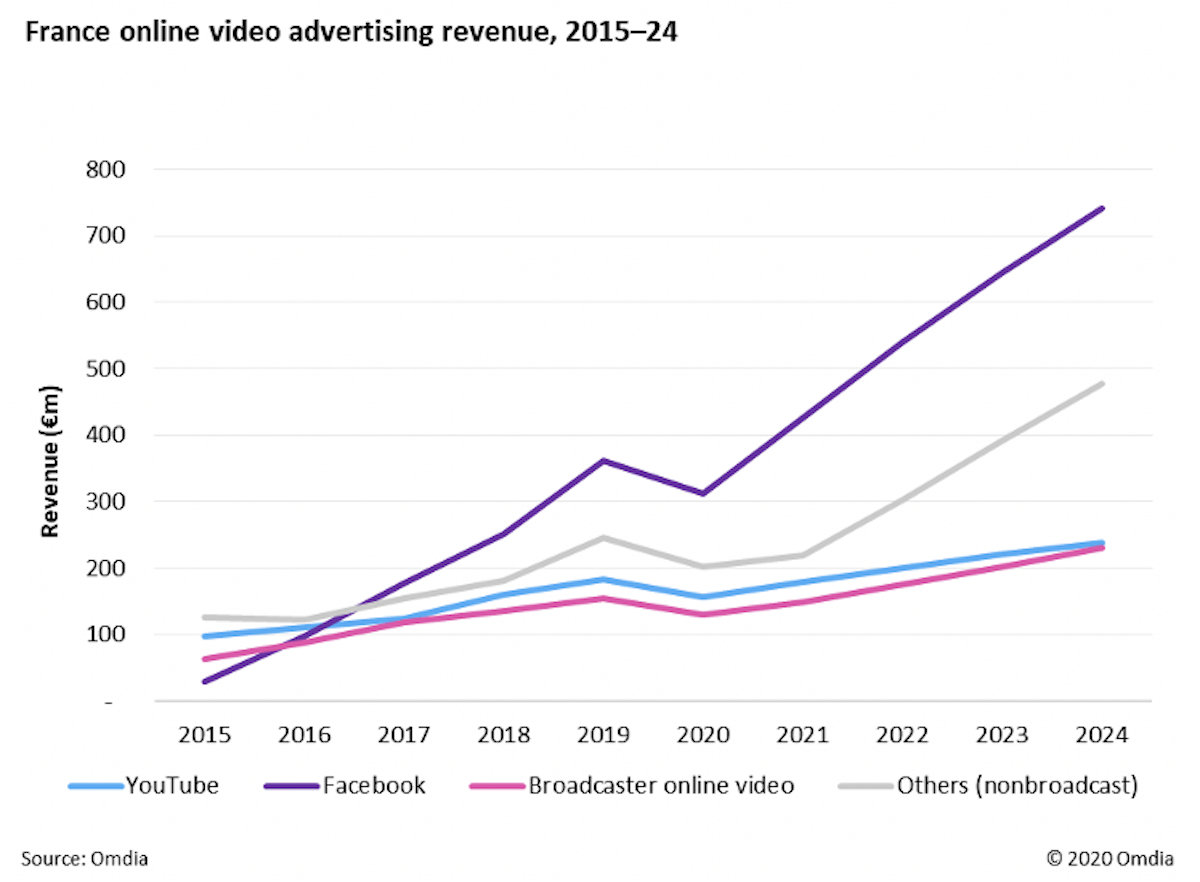

French broadcasters braced

Omdia estimates that broadcast video on demand (BVOD) generated €130m ($157m) in ad revenue in France during 2020, contributing 16% of the country’s €800m total online video ad revenue.

TF1 was the market leader with revenue of €66m, despite a fall from the year before. The company’s ad-supported service, MyTF1, had 27 million registered users in 2019, when the service recorded 1.8 billion video views (up 24% year on year). Rival M6’s service 6Play had 27 million registered accounts in 2019 and 110 million videos viewed per month, up 10% year on year.

In 2020, 59% of France’s online video ad revenue was generated by Facebook and YouTube. This share grew from 52% in 2017. Both YouTube and Facebook are forecast to grow more strongly than French broadcaster BVOD services. Omdia forecasts that broadcaster share of the online video advertising market will decrease to 14% in 2024.

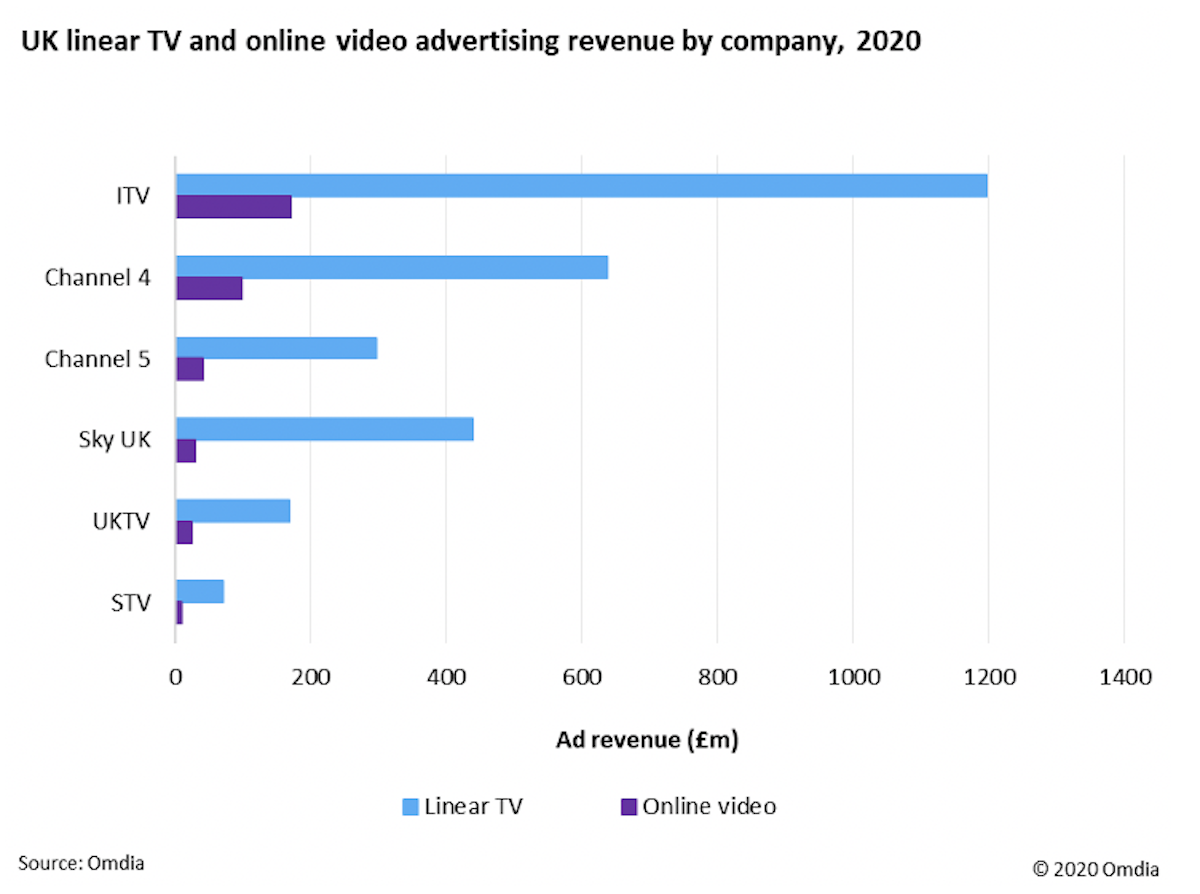

UK’s growing appetite

In 2020, 53% of the UK’s online video ad revenue was generated by YouTube and Facebook, reflecting the duopoly’s increasing dominance of the market: this figure stood at just 43% in 2017.

(Click to expand)

Broadcaster online video ad revenue accounted for 15% of the market in 2020, representing £424m ($580m) of the total online video ad revenue market of £2.8bn. Omdia forecasts that broadcasters’ share of online video advertising will drop before expanding toward the end of the forecast period as broadcasters bolster their digital ad offerings in the face of increasing OTT competition.

The importance of online video to UK broadcasters shifted up a gear in 2020. Channel 4 stated in the autumn of 2020 that digital advertising accounted for 14% of its overall revenue in 2019 and should account for 17% by the end of 2020. ITV also announced a major restructure, which elevated its on-demand services (including the ad-supported ITV Hub) within the company structure. The broadcaster said that on-demand viewing also allows for more targeted advertising, and it sees this as an opportunity for ad revenue growth. ITV reported in September 2020 that ITV Hub had 32.1 million registered accounts, up 7% from 2019.

The BBC iPlayer also has an impact on the UK broadcaster online video market too. While the BBC is publicly funded and receives no advertising revenue, the iPlayer service can be credited with helping to drive growth and adoption of long-form online video in the UK.

(Click to expand)

Indian innovation

India will generate INR65bn ($890m) in online video revenue by the end of 2020, according to Omdia. The market is dominated by YouTube, which controlled 34% of the market by the end of 2020.

This is followed by Facebook at 9% and Star India at 7% during the same period. The market is rather fragmented with other players taking 44% of revenue in 2020. These include a bunch of homegrown AVOD players such as MX Player, JioTV, and TVF and social platforms such as Twitter.

Facebook’s share of the country’s video revenue will swell to 12% by the end of 2024 as a result of its vast investments in a populous market that boasts 800 million unique mobile users. Omdia estimates that India accounted for 13% of Facebook’s global monthly active users but only contributed 0.5% of the company’s global online video advertising revenue in 2020.

This indicates plenty of room to grow in a market driven by small businesses, which is the key segment of Facebook’s advertisers. The company’s $5.7bn investment in digital technology company Jio Platforms also underlines its ambition to push WhatsApp payment in the market to create a seamless social video and e-commerce mobile experience.

Star India, the operator of Disney+ Hotstar, generated INR4.2bn ($58m) from its online video operations in 2020. This represents 4.1% of the group’s TV advertising revenue, a share that will grow to 9.3% by the end of 2024 according to Omdia’s estimates. Sony Pictures’ SonyLIV commands a sizeable INR1.8bn ($25m) online video ad revenue, about 6% of the network’s TV advertising revenue. Zee Network operates Zee5, which Omdia estimates made INR347m ($5m), or 1% of its TV advertising revenue, in 2020.

(Click to expand)

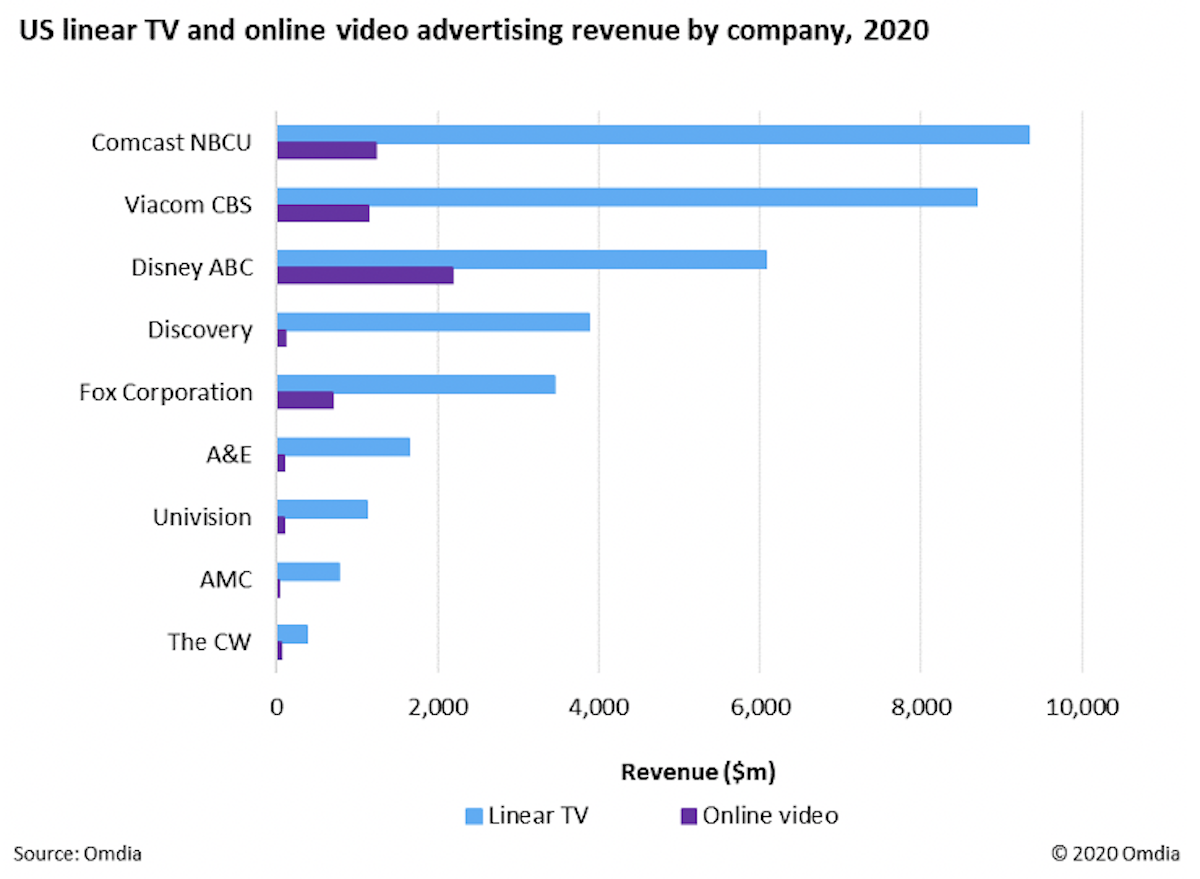

US goes next generation

While YouTube and Facebook made up 42% of online video advertising revenue in the US in 2020, their combined share will decline by several percentage points in the period to 2024 as new social platforms and a new generation of AVOD services gain traction.

The broadcaster segment will expand its market share from 14% to 18%. Growth will almost exclusively come from the new generation of AVOD services, which were launched or acquired by major US channel groups in 2019–20. Omdia expects Hulu, Peacock, Pluto TV, and Tubi (owned by Disney, Comcast NBCU, Viacom CBS, and Fox respectively) to grow in size to be comparable to flagship broadcast networks in terms of revenue within the next five years. For example, Disney’s Hulu and TV Everywhere services (e.g., Disney Now) will bring in over 33% of total ad revenue across the conglomerate’s linear TV and online properties.

The excerpts above come from Omdia’s extensive recent paper, ‘Global Online Video Advertising Report, 2020’, which provides an in-depth exploration and analysis of the market in an array of countries.

It was written by: Kia Ling Teoh, senior analyst for TV, video & advertising; Matthew Bailey, senior analyst for digital content & advertising; Tony Gunnarsson, principal analyst for TV, video & advertising; and Marija Masalskis, senior principal analyst for TV, video & advertising. Omdia is the global research powerhouse which, like TBI, is part of Informa.