After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: Exploring TV revenue raisers as streaming surges

Traditional TV markets are, at best, in slow-growth mode with the reality often being stagnation or decline, writes Adam Thomas, senior principal analyst at research powerhouse – and TBI sibling – OMDIA.

Covid-19 is serving to further promote an already flourishing online video sector to even greater heights, putting even more pressure on the traditional sector – yet there are some potential revenue raisers that could help to level the playing field. With this in mind, here are six key developments to watch into 2021.

(Click to expand)

Instability & acceleration…

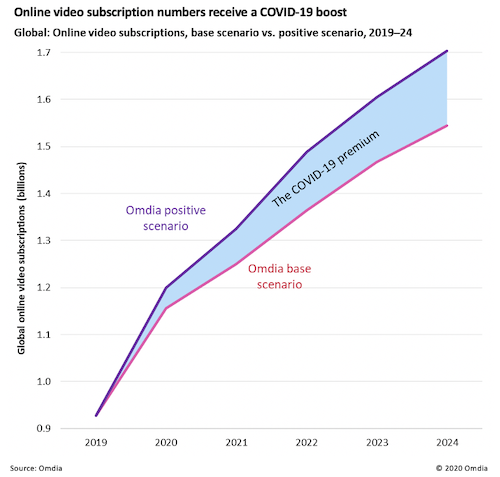

The Covid-19 pandemic has provided a further boost to an already positive trajectory for online video services. Netflix alone added 26 million subscriptions in the first half of 2020, while Disney+ has racked up more than 60 million subscriptions since its launch in late 2019. The banking crisis of 2007/08 and the global economic recession that followed represent the most obvious recent parallel to the current crisis. Periods of instability often have the effect of accelerating change that is already underway. During and after the financial crash, online video subscription numbers grew very swiftly, the global subscription total more than doubling in 2009.

… delivers more demographics

Of course, the scenarios are very different. Online video was then growing from a much lower base. Omdia’s forecasts have already been updated to account for the impact of the pandemic. But as its after-effects linger on, so more and more people will come to embrace next-generation services as being, in the overused phrase, ‘the new normal’. New demographics will be attracted into the sector, some sort of tipping point may occur, and even more impressive growth could take place. In this more positive (for online video) scenario, an extra 75 million online video subscriptions will be added in 2021, taking the global total to 1.325 billion. By 2024, an additional 158 million subscriptions will be added, giving a global total of 1.703 billion.

(Click to expand)

Taxing problems…

For more than a decade, there has been a search for effective tax measures that can be imposed on the largely unregulated global video players. The motivation behind such moves is to level the playing field with legacy companies and so slow down the amount of disruption. At work, however, are three interrelated issues. The first is that major international players (such as Netflix) and other digital service providers are commonly not subject to VAT or other sales taxes in the countries in which they operate. The second issue is whether the digital giants should make contributions to the creation of local content.

… and a $500m revenue-raiser

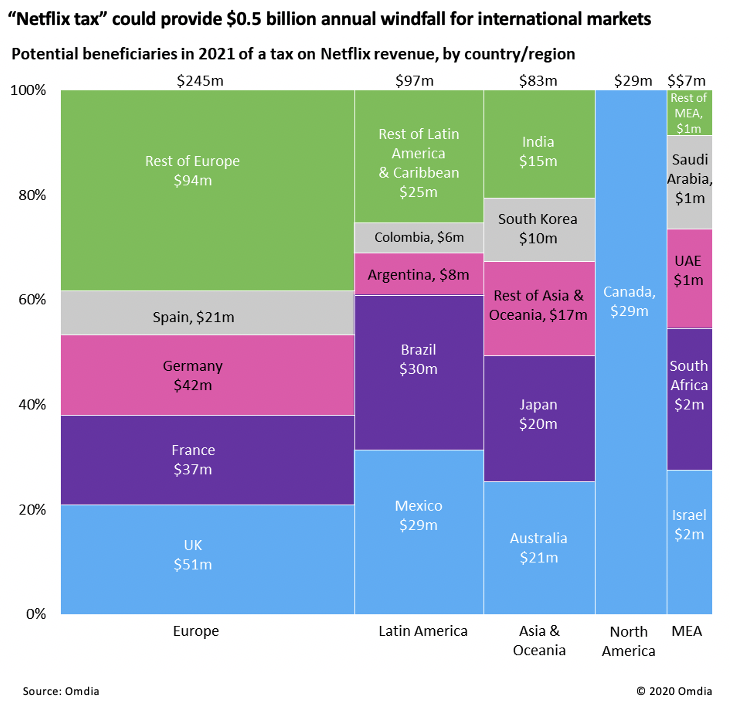

Finally, and this is the focus of this analysis, comes the issue of corporate sales taxation, with international digital players, again, not paying this tax in most of their operating territories. A proposal gaining favor has been to impose a corporate tax rate of 3% on the sales that these companies generate in each country in which they operate. The OECD is attempting to negotiate a mutually satisfactory international resolution, and Omdia expects the OECD efforts to be successful in 2021. Using Netflix as an example, if the tax was successfully applied, some $500m in revenue could be raised each year, funds that could be ploughed back into local businesses so providing some compensation for the favourable terms on which international players have so far operated.

(Click to expand)

The $10bn retransmission plug…

A key feature of the US TV market is the presence of extensive retransmission fees paid to the major free TV networks by pay-TV services for permission to carry their channels. They are worth around $10bn per year for the networks. The US is unique in terms of the size of these fees, although other countries (such as Brazil) also generate significant revenue in this way. But such countries are in the minority, and with TV advertising income stagnating, the charging of retransmission fees by other broadcasters around the world could help to fill the revenue gap.

… and overcoming roadblocks

In many countries, however, there are regulatory issues to overcome. In Canada, for example, the charging of retransmission fees is not permitted after a 2012 Supreme Court ruling. But market dynamics are much changed in the past eight years, so the timing now seems right to revisit regulatory roadblocks in Canada and elsewhere. A concerted lobbying effort with a convincing case could see attitudes change and retransmission fees in place by 2021. Negotiations to levy the fees would need to be managed carefully on a market-by-market basis, according to the ability of pay-TV operators to afford the fees. But there are numerous companies with major pay-TV operator interests making billions of dollars in profit each year, seemingly giving them some scope to afford retransmission fee payments.

Adam Thomas is senior principal analyst for TV, video & advertising at research powerhouse OMDIA, which like TBI, is part of Informa. The excerpts above are from his recent report, 2021 Trends to Watch: TV and Online Video Super Themes.