After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

Conclusion: Condensed thinking

TBI’s 2019 Distributor Survey has illustrated both the opportunities and the ‘glass-half full’ outlook of many distributors, but also the differing challenges facing those operating across scripted, unscripted, formats and kids.

Across all four sections of TBI’s 2019 Distributor Survey, there were a couple of key takeaways that keenly highlight just how the business of selling programming is rapidly changing regardless of sector.

Firstly, the bout of M&A that has been hitting most parts of the business – from Hasbro buying Entertainment One, to Disney acquiring Fox’s entertainment assets and NBCUniversal incorporating Sky – is now being reflected in distribution.

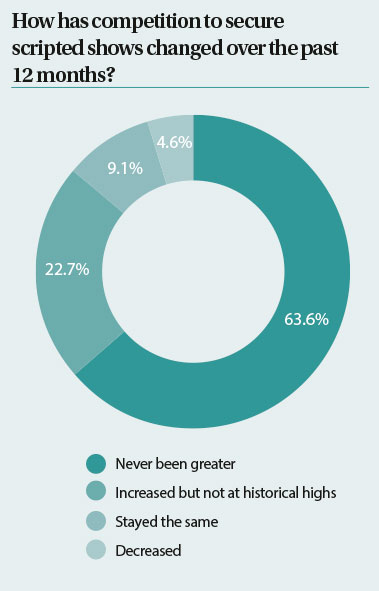

Most obviously, it means some distribution banners are disappearing from markets altogether as a result. But delve deeper and there is also an impact on independent sales outfits, which had perhaps once been able to secure programming for unconsolidated firms for their own catalogues.

Click to enlarge

With vertical integration now the name of the game for huge swathes of the content business, the impact on distribution is clear. Securing product is becoming tougher across almost every sector, with mid-sized distributors seemingly at most according to respondents. Financing shows and moving up the chain are now key aspects for most distribution outfits.

Secondly, it is clear that the impact of SVOD on distribution is still being keenly felt. And it is a fluid situation, with further changes likely as the influx of new US services enter the market and stretch their tentacles around the world, taking rights with them. More buyers are being reported across the scripted, unscripted, formats and kids business, but there is also that underlying competition for product to sell them, highlighting the inherent tension of the current distribution landscape. And for most sectors, the network business – be it free to air or pay – is not paying more for its product, meaning it is the newer OTT entrants who are driving disruption but also offering potential for growth.

All of this is playing into the wider business, not least the way shows are marketed to buyers and the events deemed important to attend. MIPCOM remains the stand-out event for the global TV business, with more than 80% of scripted distributors considering it a must-attend occasion. The same is true for those in the formats business (87%), unscripted (92%) and kids (86%), and while its sibling event MIPTV is considered less important, its place on the circuit remains relatively buoyant. More than 40% of scripted respondents consider it must-attend, and just over 62% of those working in formats agree, along with 64% of unscripted firms.

But competition is clearly kicking in and genre-focused events are vital, with myriad markets and conferences now dotting the distributor’s calendars. For scripted and format-focused folk, NATPE Miami, LA Screenings and Asia TV Forum all score highly, while unscripted and kids distributors highlight Realscreen and Kidscreen as must-attend events for their respective genres. It is in some ways representative of the wider TV and distribution business as a whole: competition is hotting up.