After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI DISTRIBUTOR SURVEY 2016, part I

TBI has surveyed distributors around the world to tap into the issues impacting their business, having drilled into the kids and scripted businesses in-depth in previous surveys. Our exclusive data, gleaned from distributors all sizes, covers their business in 2015. Topics include genres of programming moving fastest, the effects of the streaming platforms on international sales, industry consolidation, Brexit, and the relevance (or otherwise) of the big programming markets, among other issues.

TBI has surveyed distributors around the world to tap into the issues impacting their business, having drilled into the kids and scripted businesses in-depth in previous surveys. Our exclusive data, gleaned from distributors all sizes, covers their business in 2015. Topics include genres of programming moving fastest, the effects of the streaming platforms on international sales, industry consolidation, Brexit, and the relevance (or otherwise) of the big programming markets, among other issues.

Big issues

Asked about the issues that most impacted their businesses in recent time, distributors repeatedly cite the emergence of SVOD, regional economic problems, and windowing in an increasingly fragmented landscape.

Much has been made of Netflix demanding global rights to supply programming to all of its international services, but cable channels are also demanding more. Cineflix Rights boss Chris Bonney says: “The continued expansion of the big brand cable channels across multiple territories means that they require greater global rights in their commissioning deals.”

Much has been made of Netflix demanding global rights to supply programming to all of its international services, but cable channels are also demanding more. Cineflix Rights boss Chris Bonney says: “The continued expansion of the big brand cable channels across multiple territories means that they require greater global rights in their commissioning deals.”

Privately, other distributors also bemoan the extended payment terms being demanded by some of the big players and channel groups. Many sources say Netflix does not pay out production fee for around three years after a contract is signed.

As ever, macro-economic conditions are top of mind, with several distributors mentioning challenging conditions in specific territories or regions. Isabelle Graziadey, head of sales at French indie distributor Terranoa, says the biggest issues are “the economic crises in Latin America and Russia” and that “southern Europe is still slow.”

She adds that consolidation among the big players is making it “harder for independents to find their place in the market”.

Other independents agree consolidation makes life tough. Asked about the greatest challenge, Javier Martinez at Spain-based producer and distributor Phileas, says: “Consolidation of the big groups. They are strengthening their position in the market, and have more power against the small, or independent, companies.”

Several country-specific themes have emerged. In Canada, regulatory change and ongoing consolidation at a broadcaster and cable channel level is a concern for content sellers.

Tinnopolis-owned Passion is based in the UK, and its head of sales, Elin Thomas, says top-level changes are also problematic “Here, we are seeing tighter budgets at broadcasters impacting on content production which clearly affects us as a distributor,” she explains.

Tinnopolis-owned Passion is based in the UK, and its head of sales, Elin Thomas, says top-level changes are also problematic “Here, we are seeing tighter budgets at broadcasters impacting on content production which clearly affects us as a distributor,” she explains.

For BBC Worldwide’s president, global markets, Paul Dempsey, the way the production sector is evolving means distributors need to get involved in different ways. “International players increasingly want to get involved much earlier in the cycle which necessitates a different type of expertise from distributors,” he says.

For BBC Worldwide’s president, global markets, Paul Dempsey, the way the production sector is evolving means distributors need to get involved in different ways. “International players increasingly want to get involved much earlier in the cycle which necessitates a different type of expertise from distributors,” he says.

While the death of DVD as a revenue stream is frequently cited as an issue, the Worldwide exec also highlights an area that could pick up some of that slack, noting a “rejuvenation of back catalogue through box set rights”.

Australia’s kids distributor ACTF, meanwhile, highlights a technical issue making life challenging for distributors in the digital world. “Broadcasters are all wanting delivery of differing digital file types,” a rep says. “Transcoding files to so many differing specs is expensive.”

Dramatic times?

Netflix original series Narcos

Most of the international distribution companies covered in the TBI Distributor Survey service multiple genres of programming. Over 70% of respondents sell drama content, 60% have finished unscripted programming, 63% formats and 66% factual.

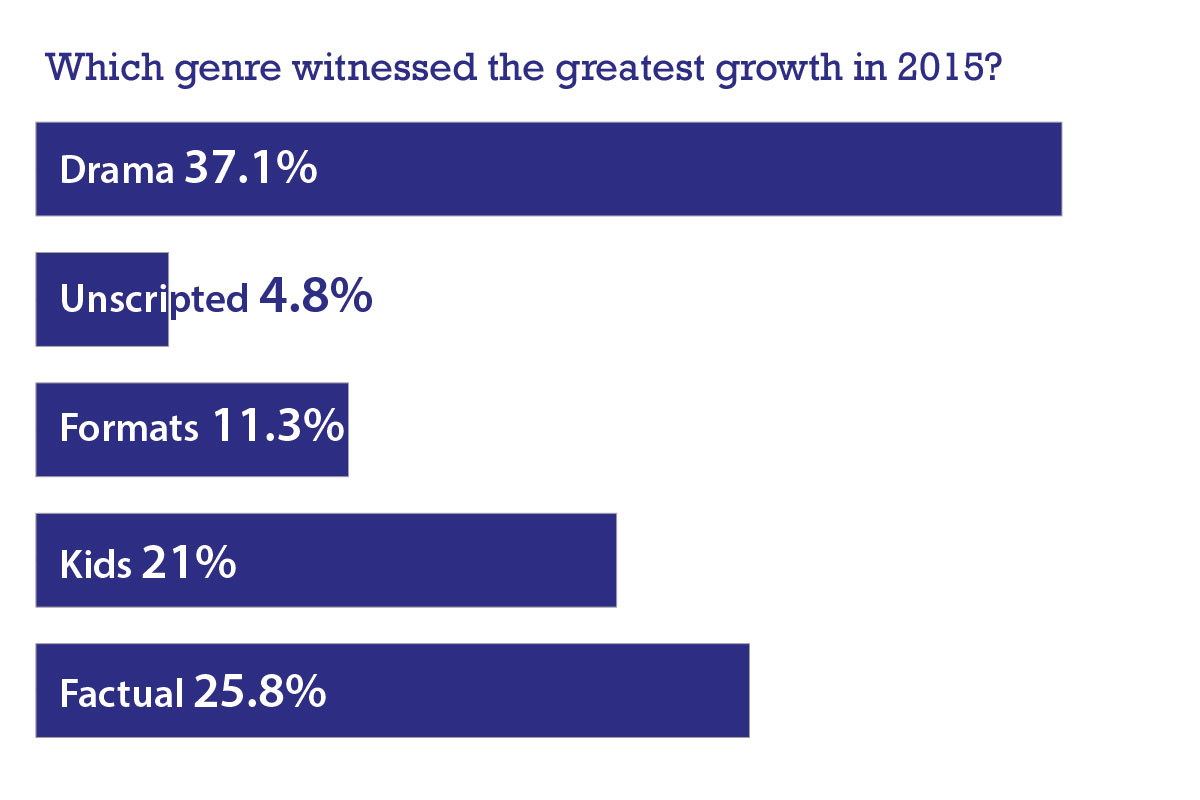

The key question is, which genre is moving fastest in the period surveyed (2015)? Does the golden age of drama mean scripted wins out, or are docs and entertainment gaining ground?

As drama reaches ever-greater creative heights, has ever-bigger budgets, and with more commissioning channels than ever, the distributors selling multiple genres of programme overwhelmingly say this was the single genre that experienced the greatest growth in 2015. Over one-third (37%) single out scripted.

Factual is second, with 25% saying it was the fastest-growing genre, ahead of kids (21%), formats (11%), and unscripted (4%).

Data-driven sales?

With an increasing array of tools available, and numbers beyond simple linear ratings, we asked whether distributors were increasing their use of data and big data insights to drive sales.

We received a mixed response. At the heavy adopter end of the range are the huge, global distributors, with many of the medium and smaller operations more inclined to go on gut feeling.

“Distribution is not just about selling the new product, but managing your on-going franchises to deliver a long and sustained multi-window sales life,” says Endemol Shine International boss Cathy Payne. “The data and analysis that we have access to as part of Endemol Shine is fundamental [to what we do].”

“Distribution is not just about selling the new product, but managing your on-going franchises to deliver a long and sustained multi-window sales life,” says Endemol Shine International boss Cathy Payne. “The data and analysis that we have access to as part of Endemol Shine is fundamental [to what we do].”

BBC Worldwide is similarly exacting, working with data firms Parrot Research and Affinio, and using of data and research to arm the sales team. “We have a very sophisticated way of selling which uses insight at its heart to understand how content can create value for customers,” says Paul Dempsey.

“Every sale needs reliable data and insight attached to it, from linear TV data through to SVOD viewing data, and so we have a dedicated team who work to support the sales team. We have created a range of tools for the team to analyse ratings data and market conditions.”

As well as overnights and consolidated ratings, numerous distributors say YouTube views are key stats – and are free. “Performance history, including social media stats, are regularly used as a sales tool, but actually it’s more about knowing and being passionate about your content,” says Karen Young, boss of indie distributor Orange Smarty.

The cost of getting the data needed to boost sales is cited as reason to not pay for services, as is the sense that buyers do not always want reams of data to convince them to sign off. “At the end of the day, the buyer either wants the show and thinks it will work for their audience, or they don’t,” notes Australia’s ACTF. “Throwing lots of stats and data at them about how well it performed in a particular territory doesn’t mean anything if they don’t think it will work well in their territory.”

If not directly helping sales execs, data is useful to hone marketing outreach, several distribs counter.

“’‘Big data’ is probably overplaying it given that there are a finite number of potential customers in the world,” says Red Arrow International in its submission. “But we are increasingly using data gathered across our marketing channels to refine and reshape our marketing effort, including quantitative web, email and social analytics. Qualitative surveys and client feedback is still proving important in this business, which is no surprise given that it is built on close customer relationships.”

Hot spots

Europe, despite its various economic woes, was by some margin the region that distributors single out by 34% of respondents as the fastest-growing in 2015. Diving deeper, western Europe was highlighted (11%) as the global hot spot through the year.

Shopping a programme or format to the US, still the world’s largest TV market, is often considered the Holy Grail, given the licence fees on offer and the potential to use a US deal to drive sales elsewhere. Distributors rank it behind Europe as a hot spot, with 15% saying it was the fastest growing territory for them in 2015. Further north, the growth was less prolific, with just 1% citing Canada as the fastest-grower.

Other notable hot spots in 2015 include Asia (13%) and Latin America (8%). The Middle East was a big region for some (6%), and Africa and Australia perhaps surprisingly tied with 5%.

TOMORROW: READ WHAT MARKETS DISTRIBUTORS VALUE MOST IN THE TBI DISTRIBUTOR SURVEY, PART II