After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: Unpacking sub-Saharan Africa’s pay-TV growth & OTT potential

With pay-TV subscriptions in sub-Saharan Africa growing in 2022, Omdia’s research analyst Samuel Nkwam reveals how the region is adapting to viewer demands and streaming potential.

With pay-TV subscriptions in sub-Saharan Africa growing in 2022, Omdia’s research analyst Samuel Nkwam reveals how the region is adapting to viewer demands and streaming potential.

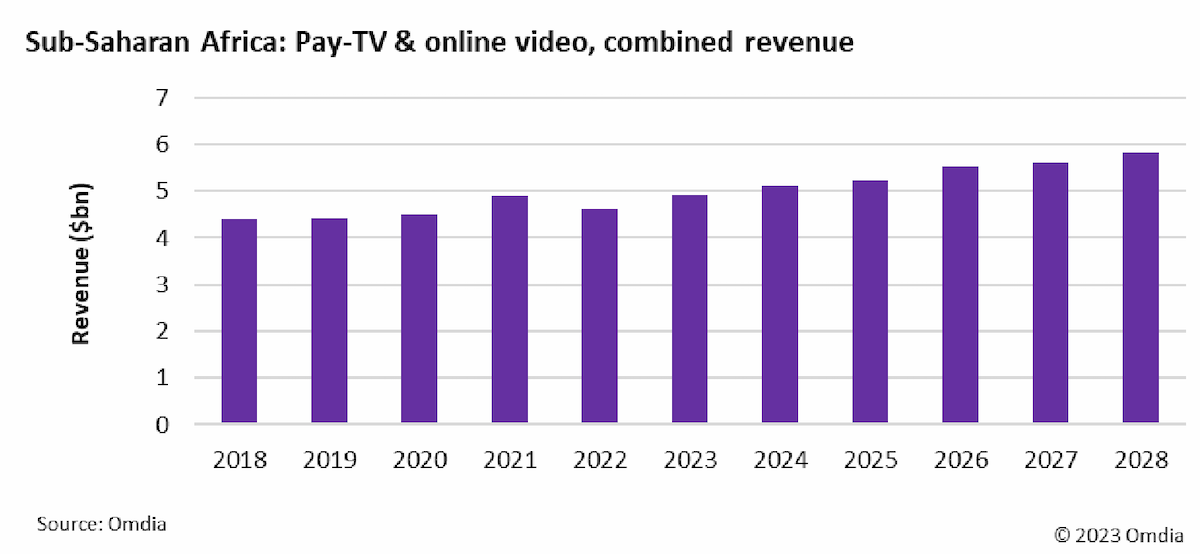

Pay-TV subscriptions in sub-Saharan Africa rose by 5.7% between 2021 and 2022, reaching almost 30.4 million by the end of the year.

However, following strong post-pandemic growth in 2021, pay-TV revenue dipped by 7.5% in 2022, as the Federal Reserve’s recent interest rate increases have put considerable downward pressure on local African currencies.

Sub-Saharan Africa is considered by Omdia to be a mobile-first market and OTT video adoption has continued to grow in the region, with subscriptions reaching almost 4.5 million, a 25.6% increase from end-2021, with revenue growing 29.5% to $294m over the same period.

Revenue & subscriptions

[Click to expand]

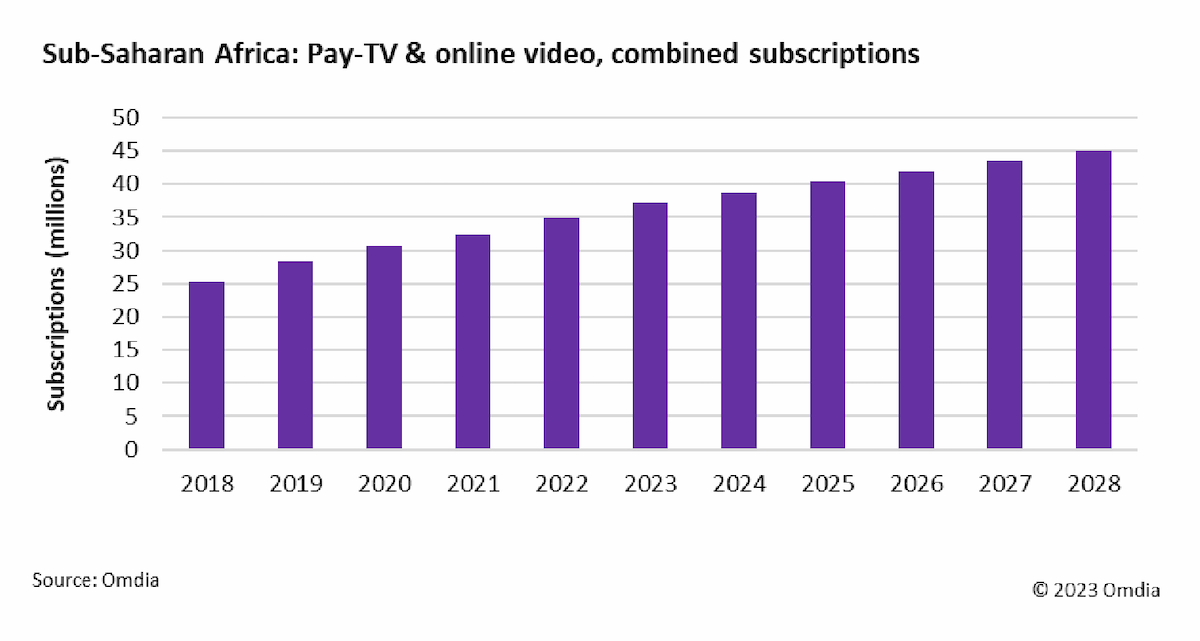

Pay-TV and online video subscriptions in sub-Saharan Africa reached a combined total of 34.9 million in 2022 and Omdia forecasts that this number will increase at a compound annual growth rate (CAGR) of 4.4% to reach just over 45 million by 2028.

Primary pay-TV penetration across sub-Saharan Africa stood at 43.9% in 2022, with South Africa and Nigeria leading the way with penetration rates above 50% in 2022.

The pay-TV landscape in sub-Saharan Africa is still highly concentrated and oligopolistic, with the three largest players ‒ MultiChoice Group, StarTimes and Canal Plus ‒ accounting for 84.3% of total pay-TV subscriptions in the region in 2022.

This market dynamic is a result of high barriers to entry resulting from high regulatory and licensing costs, embryonic digital infrastructure rollout, high upfront customer acquisition costs, and the limited availability of premium content, which is out of the financial reach of many upstart operators.

Smaller regional players do exist, such as Zuku and AzamTV, which operate in East Africa, and HD+ Ghana, which launched a new sports channel called Scooore in January 2023.

OTT subscription penetration in sub-Saharan Africa reached 5.7% in 2022, with online video subscriptions exceeding 4.5 million. As internet connectivity improves and price points come down, smartphone adoption is increasing and OTT operators continue to adapt their offerings to mobile-first markets.

Omdia forecasts that online video revenue in the region will increase at a CAGR of 9.6% from $294m in 2022 to $510m by 2028.

The exceprt above is taken from Omdia’s Pay TV & Online Video Report: Sub-Saharan Africa – 2023, which is available to read in full here (subscription required). Samuel Nkwam is research analyst for TV & Online Video at Omdia, which is part of Informa, as is TBI.