After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: All eyes on 2022’s M&A extravaganza

James Bond: No Time To Die

The past year has been one of the busiest for those working in M&A, as production groups seek scale to compete on the global stage. Omdia’s Tim Westcott picks out the key events and pinpoints who’s done what so far.

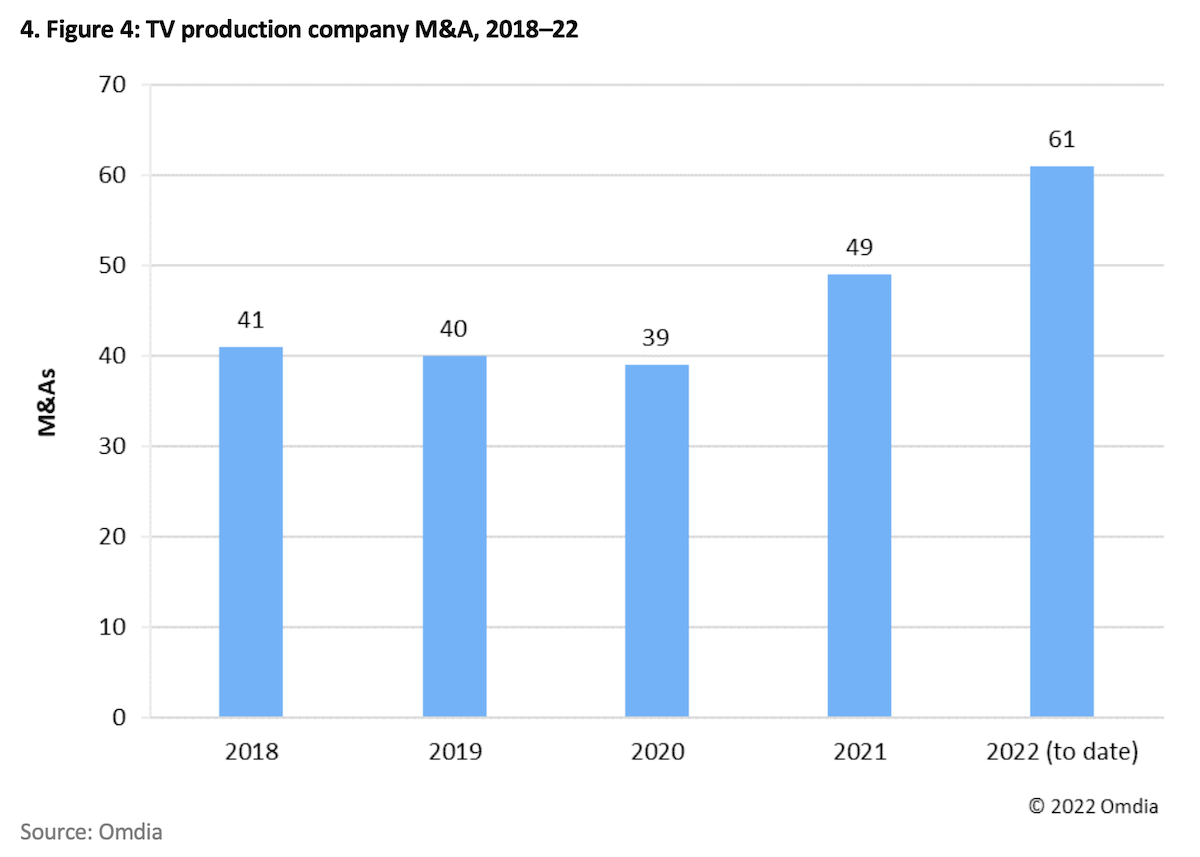

Omdia has tracked M&A activity among TV and online production companies over several years. These include full takeovers, startups, and minority investments.

After hitting a peak in 2017 when we tracked 111 deals, activity appeared to have plateaued but has regained momentum over the past two years.

Already in 2022, we have recorded 61 deals, up from 49 the year before. This includes Amazon’s $8.5bn acquisition of MGM Studios, completed this year, which is by a long way the biggest deal in this period.

France’s Banijay Group has been the most active buyer in this period, with its acquisition of Endemol Shine in 2020 standing out as a transformative deal that made it the largest production group outside the US.

This year alone, Banijay has added eight groups to its growing portfolio, most recently Australia’s Beyond International. In May 2022, Banijay floated on the Euronext stock market through a special purpose acquisition company called FL Entertainment and reported net debt of €2.2bn in its launch prospectus.

This year alone, Banijay has added eight groups to its growing portfolio, most recently Australia’s Beyond International. In May 2022, Banijay floated on the Euronext stock market through a special purpose acquisition company called FL Entertainment and reported net debt of €2.2bn in its launch prospectus.

Fremantle, owned by Luxembourg’s RTL Group, had been relatively inactive after a major acquisition spree in the last decade. The group has , however, returned to the M&A market recently, acquiring 12 Nordic production companies from NENT group last year and increasing its stake in UK scripted producer Dancing Ledge Productions, among numerous other deals.

Prior to some of those deals was a target set down by parent RTL Group, which requires Fremantle to grow its revenue to €3bn by 2025, which is likely to require further acquisitions.

France has overtaken the UK as the most active buyer over the last five years. Other than Banijay, this activity has stemmed from other companies building their international networks: Newen Studios, now owned by TF1, has done eight deals, while the private equity–backed Asacha Media Group has also built its footprint with deals in other European countries. Mediawan acquired the production interests of the Lagardère Group in a $114m deal in 2020.

UK companies remain active. ITV Studios has this year acquired natural history producer Plimsoll Productions, while All3Media merged its Maverick TV and Objective Media Group labels. Both BBC Studios and Channel 4 have followed a strategy of taking minority stakes in small or startup indies, often selling out when companies are sold on. BBC Studios was a backer of the drama producer Bad Wolf, which Sony Pictures has taken over in a £60m deal.

Newcomers to the M&A space include Candle Media, which has invested in Reece Witherspoon’s production company Hello Sunshine, children’s specialist Moonbug Entertainment, and the Israeli Faraway Road Productions. The North Road Company, owned by former Fox executive Peter Chernin, acquired five US factual production companies from Red Arrow Studios after the German company decided to scale down its international production network.

Netflix has also made some selective deals, backing a new production company started up by Black Mirror’s Charlie Brooker and Annabel Jones and acquiring the rights to the Roald Dahl estate. In July, Netflix agreed to acquire the Australian full-service animation studio, Animal Logic. This is a departure for the streaming giant, which has so far invested its massive programming budget with external suppliers.

The excerpt above is from World TV Production 2022, an annual report compiled by Omdia, which is part of Informa, like TBI. The report has been written by Tim Westcott, Omdia’s senior principal analyst for digital content & channels.