TBI Tech & Analysis: Plugging the US cord-cutter’s content gap with virtual pay-TV

As an increasing number of US viewers cut the cord and their access to linear services, Sarah Henschel, principal analyst, media & entertainment at Omdia, tells TBI that consumers are finding alternatives in VOD and virtual pay-TV offerings.

In the US, pay-TV subscriptions saw a 7% decline in 2021, ending the year with 69.7 million households with a traditional pay-TV subscription. Of the 125.1 million TV households in the US, 55.4 million will be left without a traditional linear experience.

After a consumer “cuts the cord,” they are left without the live and linear benefits of a pay-TV subscription. Historically, this meant that users were left with subscription video on demand (SVOD) services alone or would have to lean on subscriptions owned by friends and family to access anything on live TV.

Cord-cutting substitutes are adapting and leaning more and more into finding ways to supplement their services with live offerings. Consumers can now mix and match across online services to fill the needs pay-TV previously remedied.

Sports, reality, and news content are slowly finding ways to integrate into SVOD, advertising-based video on demand (AVOD), and virtual pay-TV offerings. In the US, most TVs are equipped with digital tuners; if consumers purchase an additional TV antenna, they can access over-the-air (OTA) local channel content via their TV connection. This is a US-specific phenomenon; international consumers have the antenna automatically equipped within their TV sets.

At the end of 2021, there were 13.6 million virtual pay-TV subscriptions in the US representing ~11% of TV households in the US. They are highly engaged households with a propensity to pay.

These consumers on average use 13.5 video services per household versus 7.4 for the average US household. Because virtual pay-TV services are internet-based and have no long-term contracts like traditional pay-TV, user interfaces/experiences (UI/UX) are received well and can adapt to changing customer needs. As digitally focused platforms, their interfaces can adapt more quickly than traditional services, and application updates can be pushed more frequently to be more user friendly.

Click to expand

Virtual pay-TV business models

While virtual pay-TV looks to offer affordable pay-TV to the consumer, the economics of the business model still operate in the same fashion as traditional pay-TV. Virtual pay-TV services still pay carriage fees to channel owners to license content and offer those channels in the platform.

Channel groups often bundle multiple channels together during negotiations to require carriers to take all or nothing. This forces virtual pay-TV services to pay high margin prices for licensing with little margin left over for in-house profits. This also explains why companies in the US that have done well have larger conglomerates backing them (Google and Disney) to offset operational costs.

According to carriage fee analysis done by Omdia in 2020, virtual pay-TV operators often pay a 20% premium for carriage fees compared to major traditional pay-TV players. With an average channel fee of $0.65, 75 channels cost an operator $46.48 per sub and $55.78 with a 20% markup. This example may leave only a $10 operating margin per sub.

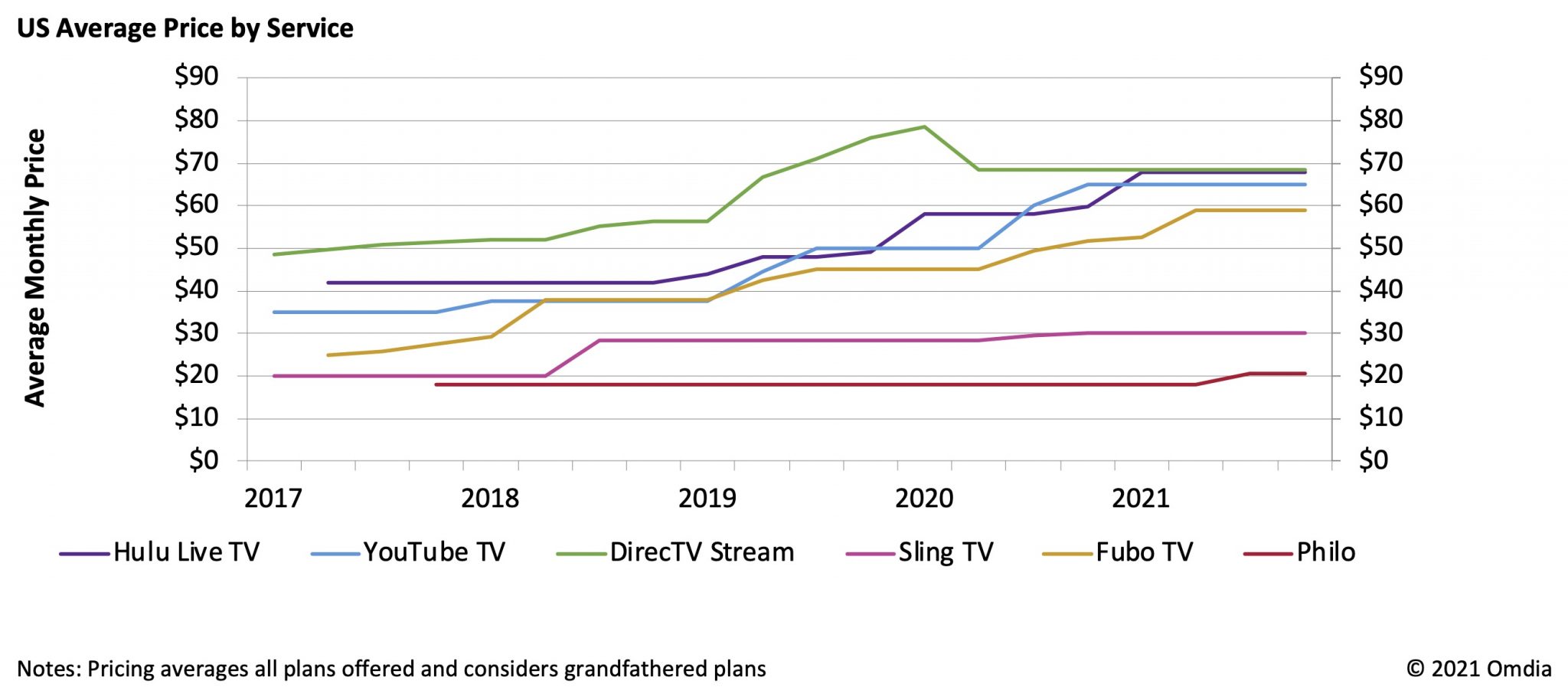

The tough nature of the virtual pay-TV business in the US has seen the failure of Stream, PlayStation Vue, and AT&T TV Now/DirecTV Now. The latter has morphed into DirecTV Stream but has faced many rebrands and price hikes. Pricing packages have increased in price so much that they closely match the prices of a traditional pay-TV package. Other than consumer spend on subscriptions, virtual pay-TV operators earn ad revenue. Negotiating higher owned ad loads is critical to maintaining profitability for these companies.

Sharing a subscription

When comparing Omdia’s Consumer Research – Connected Households and Users Database with subscriber data from our TV & Online Video service, we analyzed the number of users per subscription household by service. We saw that virtual pay-TV in the US has continued to have more users per subscription than each traditional pay TV, Netflix, and Amazon. In April 2021, virtual pay TV had 3.7 users per subscription on average while traditional pay TV had 2.3.

Click to expand

This higher proportion of users to subscriptions may be multiple households sharing one singular virtual pay-TV subscription. Unlike pay-TV, some virtual pay-TV services offer multiple profiles per subscription, which could encourage password sharing. Splitting a virtual pay-TV subscription across two households would also bring down the high cost of virtual pay-TV that consumers have been reluctant to get locked into.

YouTube TV is the driver of services with user over-indexing; in April 2021, YouTube TV accounted for 26% of total virtual pay-TV subscriptions, but 39% of total virtual pay-TV users. Virtual pay-TV users also typically skew younger than the average pay-TV and SVOD users, meaning they may be more tech-savvy and more likely to seek content post-cord-cutting. While password sharing and subscription sharing may initially seem like a bad trend for service growth, it has proven to be quite the opposite for YouTube TV. As a service, it has the most users per subscription, but that growth has allowed it to become the number one service in the US.

Although North America (more specifically the US) takes the single largest market share for virtual pay-TV globally, Western Europe is only slightly behind, with both regions taking around 30% global market share each in 2021. In non-US markets, virtual pay-TV can take a variety of formats, catering to all types of consumers at a different price points. Some highlights include:

- Replicating free-to-air TV: German offerings, including Zattoo and MagentaTV Plus, primarily offer free-to-air (FTA) linear channel access via OTT as well as a handful of premium channels as part of paid subscription offerings.

- Replicating premium pay TV: Sky’s NOW and Sky Ticket TV and Sport offerings provide premium linear channels only, without any FTA options.

- Replicating full pay TV: OSN’s latest OTT streaming offering fully replicates its traditional satellite pay-TV service across the Middle East and North Africa.

- Bundled TV channel offering: Most of Turkey’s virtual pay-TV subscribers are bundled at very low ARPU, with telco mobile and home internet packages. Most of these come from either Turkcell and Tivibu, peaking in the last couple of years with several million subscriptions each.

Outside of US, nearly 60% of virtual pay-TV subscriptions are bundled. Using owned virtual pay-TV services to enhance the value of telco mobile and broadband offers has drawn in substantial numbers of relatively low value bundled OTT video subscription users. Furthermore, 60% are from just five other markets, namely Germany, Turkey, Russia, the UK, and Italy.

Sarah Henschel is principal analyst for media & entertainment at Omdia, which like TBI is part of Informa. The excerpt above is from the Omdia insight report ‘Virtual Pay TV (vMVPD) Report – 2021.’ To read in full, click here.