TBI Tech & Analysis: Exploring Japan’s unique pay TV & streaming ecosystem

(Click to expand)

Jun Wen Woo, senior analyst for TV & Online Video at research powerhouse Omdia, delves into Japan’s fascinating content market and explores how pay TV and streaming fortunes have changed.

Japan is a unique market where traditional TV/video market sources like broadcasters and the physical video market remain relevant in the country despite fast growing broadband infrastructure and smartphone adoption.

However, the physical market continues to shrink and traditional broadcasters and pay TV companies are also moving towards the online video sector. The local online video sector is fragmented and M&A activity is anticipated in the short term.

(Click to expand)

Streaming surge

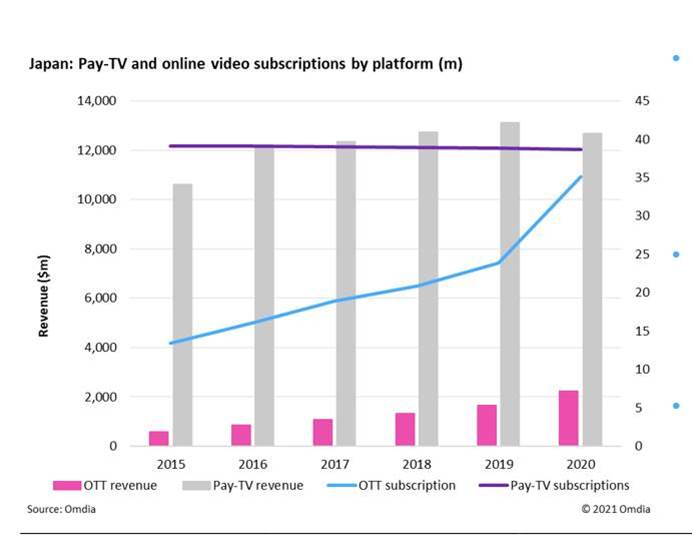

Japan’s online video subscription market is the second largest in the Asia Pacific after China. The total value of the online video subscription market in Japan reached $2.2bn in 2020, with year over year growth of 36% due to a significant increase in media consumption, as more consumers stayed at home during the pandemic.

Total subscription numbers increased from 24 million in 2019 to 35 million in 2020, led by Amazon Prime Video, Netflix, and local players U-Next and Hulu Japan.

Pay TV, meanwhile, generated revenue of $12.7bn in 2020, a drop from $13.1bn in the previous year, while subscriptions remained flat at 39 million. Pay TV penetration in Japan remains high at 72% of all TV household, as consumers continue to hold onto their cable subscriptions as many still perceive package media to be of a higher quality than the alternatives. Top pay TV operators in the market are J:COM, WOWOW and Sky Perfect.

Covid-19 has accelerated OTT subscription growth in Japan, even though average views for online video services will likely retreat back towards previous levels after the pandemic. However, Omdia expects a large proportion of online video subscriptions to be retained as a result of a change in consumer behavior, as well as cord-cutting. Omdia forecasts the total number of online video subscriptions will exceed pay TV subs in 2022.

(Click to expand)

Amazon leads the stream

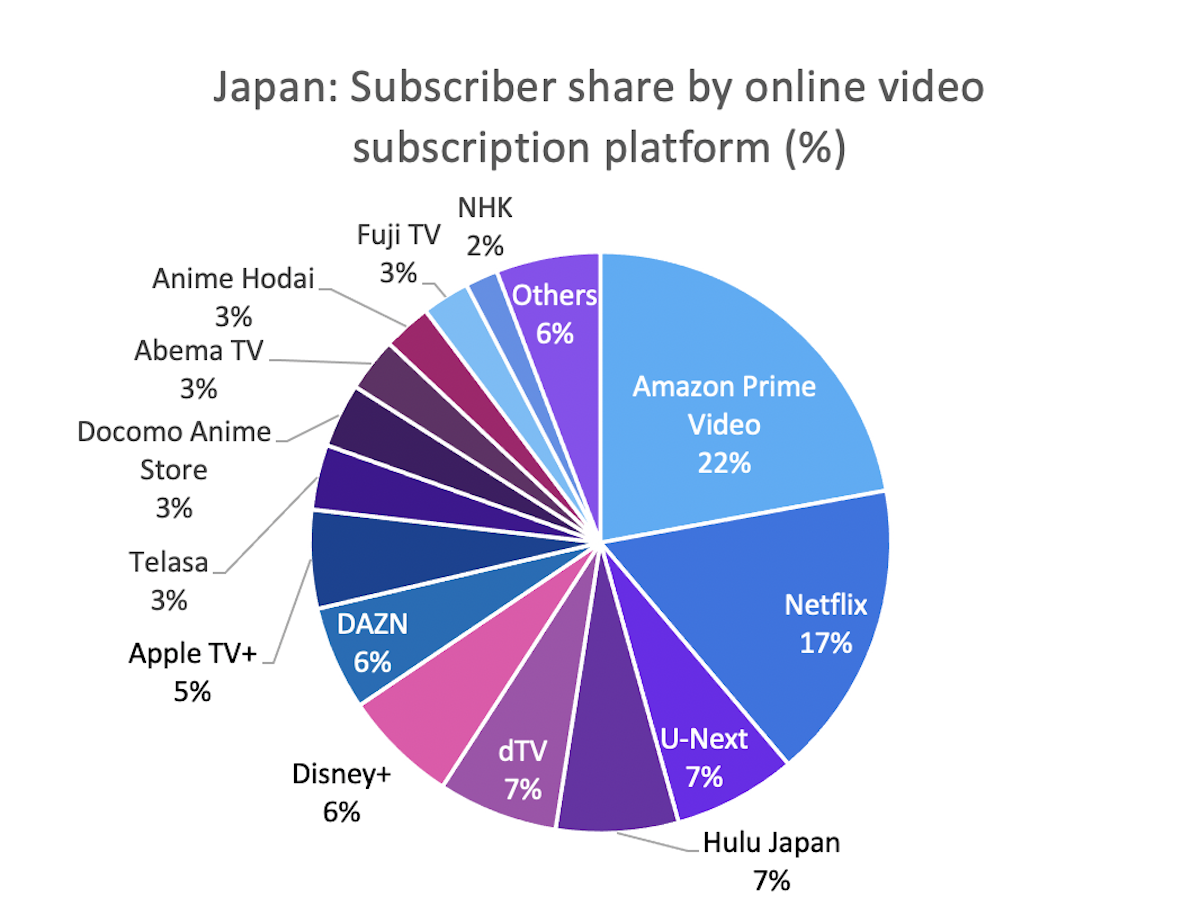

The online video on demand subscription market reached JPY244.9bn ($2.2bn) in 2020, up by 36% from 2019. The largest online video player in terms of subscriber numbers are Amazon Prime Video, followed by Netflix, U-Next and Hulu Japan.

The combined share of global giants Amazon Prime Video and Netflix has increased significantly in the past two years, from 29% in 2018 to 39% in 2020. Amazon Prime is popular in the market due to the overall platform benefits of a Prime membership; while growth in the Netflix subscription base correlates with its increased investment in local production.

The increasing popularity of global services like Amazon Prime Video and Netflix continues to put pressure on local players.

Among the local players, Avex’s dTV subscriber base has dropped by more than half since 2017, while Hulu Japan subscriber growth has noticeably slowed down. U-Next showed the most significant growth in 2020 among all of the local subscription services.

The current overcrowding of the market means consolidation in this sector is inevitable. Omdia expects there will be merger and acquisition activity among local players in the coming years as the market continue to develop.

(Click to expand)

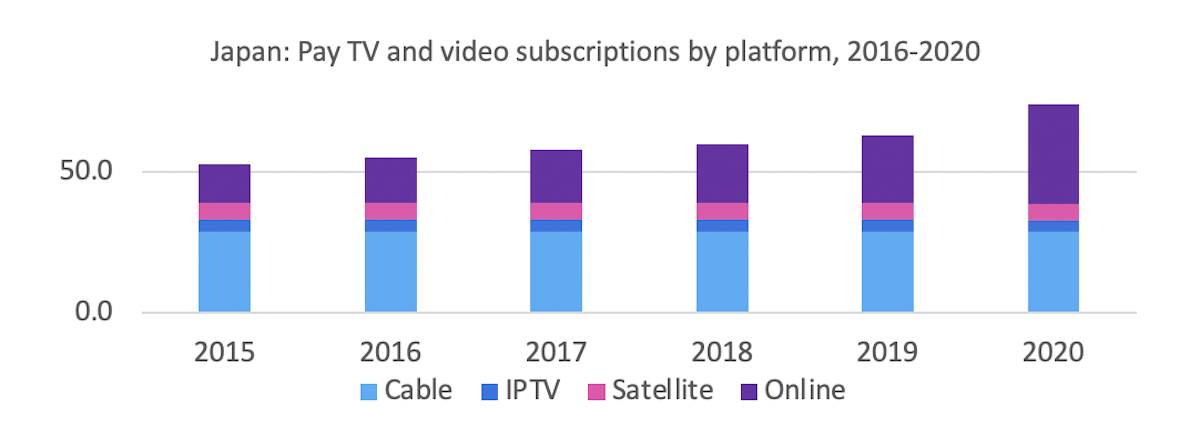

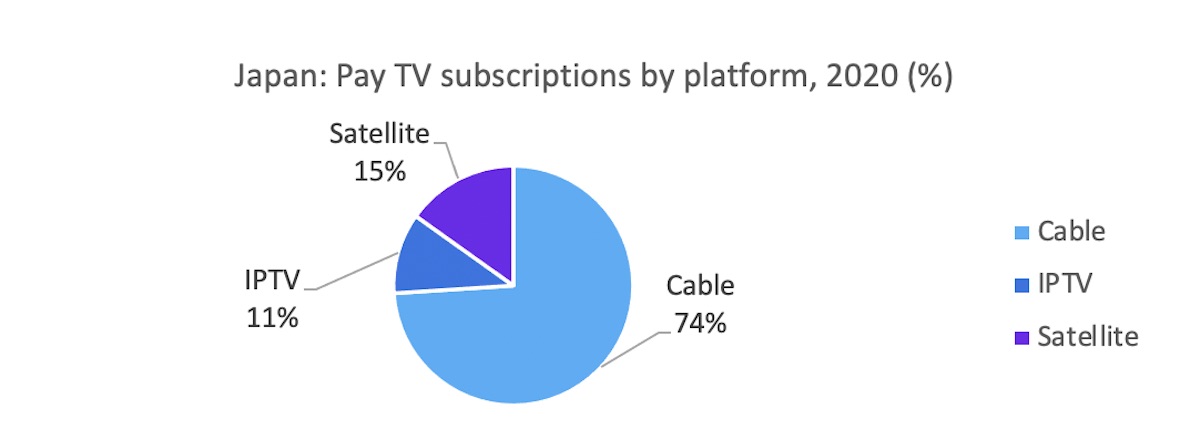

Pay on pause

In 2020, nearly three quarters, or 28 million, of all pay TV subscriptions in Japan were delivered via cable TV. Despite the increase in online video services, cable subscription numbers have remained stable with stagnant growth. IPTV subscriptions will continue to grow in Japan, supported by growing optical fiber network coverage in the country and Omdia expects there will be an ongoing decline in satellite pay TV subscriptions.

In Japan, the market leader J:COM captured 23% of pay TV revenue in 2020, ahead of Hikari TV (21%) and Sky Perfect (11%). Furthermore, J:COM not only operates as a cable pay TV operator but also as a channel in Japan, In 2010-2020, 90% of J:COM’s pay TV revenue came from direct subscription.

Total pay TV revenue remains high at $12.7bn, compared to online video revenue at $2.2bn in 2020. The total pay TV revenue figure is expected to grow at a slow compound annual growth rate (CAGR) of 1.1% – from just under $12.7bn in 2020 to $12.8bn in 2024.

The excerpt above comes from Japan: TV And Online Video Trends. This in-depth report was written by Jun Wen Woo, who is senior analyst for TV & online video at research powerhouse Omdia, which – like TBI – is part of Informa.