Pay TV outshines piracy in MENA

Piracy remains a major problem in the Middle East and North Africa, despite the many efforts to eradicate it. Digital TV Research principal analyst Simon Murray showcases the latest data and forecasts relating to piracy and the wider pay TV market in the MENA region.

Piracy remains a major problem in the Middle East and North Africa, despite the many efforts to eradicate it. Digital TV Research principal analyst Simon Murray showcases the latest data and forecasts relating to piracy and the wider pay TV market in the MENA region.

According to the latest Digital TV Middle East & North Africa report, there are 34.3 million Arabic-speaking free-to-air satellite TV homes in the region. Digital TV Research estimates that at least 10% of these homes also receive pirated premium satellite TV signals. This represents considerable revenue loss to the genuine players.

The legitimate side of the Arab-speaking pay TV business is becoming a two-horse race between beIN Sports/Al Jazeera and OSN, the latter of which has begun carrying premium channels of former rivals channels. Both operators are primarily delivered via satellite, although several cable and IPTV operators carry one or both of these packages.

Given that there are 725 free-to-air channels, premium pay TV operations in the Arabic countries were traditionally mostly confined to the expatriate populations. However, things are changing, with more Arabic content attracting local subscribers.

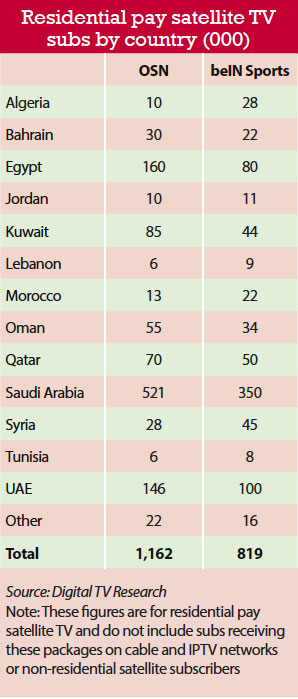

Digital TV Research estimates that beIN Sports had 819,000 residential satellite TV subscribers by 2015. This figure excludes non-satellite subscribers and non-residential satellite subscribers. Mostly delivered via satellite, the channels are also available on several cable and IPTV platforms such as Ooredoo in Qatar, Mobily in Saudi Arabia, and Etisalat and Du in the UAE.

beIN Sports offers 18 pay TV channels: the first 10 are in Arabic, and the next six form the Global package, which has two in English, three in French and one in Spanish. NBA and Fox Sports are available a la carte or as part of the Global package. There are also two FTA channels: beIN Sports and beIN Sports News.

beIN Sports offers 18 pay TV channels: the first 10 are in Arabic, and the next six form the Global package, which has two in English, three in French and one in Spanish. NBA and Fox Sports are available a la carte or as part of the Global package. There are also two FTA channels: beIN Sports and beIN Sports News.

beIN Sports Arabia, formerly called Al Jazeera Sport, has been aggressively signing up rights, including regional exclusivity for the European Champions League for three seasons until 2017/18 for a reported US$300 million and the 2014, 2018 and 2022 World Cups, the last of which Qatar will host.

In July 2013, the company acquired the exclusive Middle East and North Africa rights, covering 23 countries, to the English Premier League for the three seasons until mid-2016. beIN also holds the rights to Italy’s Serie A, France’s Ligue 1, Germany’s Bundesliga, Spain’s La Liga and the AFC [Asian] Champions League as well as NBA, US and French Open tennis and the Tour de France.

Pan-Arab satellite broadcaster Al Jazeera is owned by the Qatari government, with 20 channels on offer. Its Arabic channel is available in 50 million homes worldwide. Al Jazeera English is available in 220 million households in more than 110 countries.

beIN Sports was reported in the local press to have acquired a 53% stake in Turkey’s Digiturk for $820 million in December 2014. However, these reports await official confirmation from either party. This stake was a result of the Savings Deposit Insurance Fund of Turkey acquiring the assets of the Cukurova Group.

The loss of the English Premier League rights to beIN Sports was a major blow to Abu Dhabi Sports. The company had struggled to gain subscribers, reaching about 600,000 across its 20 channels in the previous deal. However, Abu Dhabi Sports regained some ground in December 2013 when it won the rights to UEFA’s qualifiers for Euro 2016 and the 2018 World Cup. The company also holds the rights to the Arab Gulf League; screening three matches a week.

Since September 2014, Abu Dhabi Media’s premium channels, including sports and new channel Abu Dhabi Drama+, have been exclusively available on OSN.

Digital TV Research estimates that OSN had 1.16 million residential satellite subscribers by 2015. This figure excludes non-residential subscribers and subs to the non-satellite platforms. This indicates strong growth as parent KIPCO stated that OSN had 858,000 subscribers at September 2013, and 734,000 by 2015.

Carrying 146 channels, including 38 in HD, OSN was formed from the merger of Kuwaiti-owned Showtime Arabia and Orbit Communications in July 2009 to create the largest pay TV platform in the Middle East.

OSN has appealed mostly to the expatriate community in the past. In August 2013, OSN acquired Pehla, which targets the 800,000 South Asian homes in the region and has rights to top cricket.

However, the company is now putting greater emphasis on attracting local subscribers. For instance, OSN has started carrying channels from former rival ART as well as premium channels from Abu Dhabi Media.

OSN is owned by Panther Media Group, which, in turn, is 60.5% controlled by KIPCO (Kuwait Projects Company) and Saudi Arabia’s Mawarid Group. KIPCO announced in June 2013 that it was planning an IPO for OSN, but these plans were postponed in November after the company secured a US$200 million loan.

OSN is owned by Panther Media Group, which, in turn, is 60.5% controlled by KIPCO (Kuwait Projects Company) and Saudi Arabia’s Mawarid Group. KIPCO announced in June 2013 that it was planning an IPO for OSN, but these plans were postponed in November after the company secured a US$200 million loan.

In August 2014, KIPCO rejected a US$3.2 billion bid from US private equity firm Hellman and Friedman for its stake in OSN, whose revenues were about US$500 million in 2013.

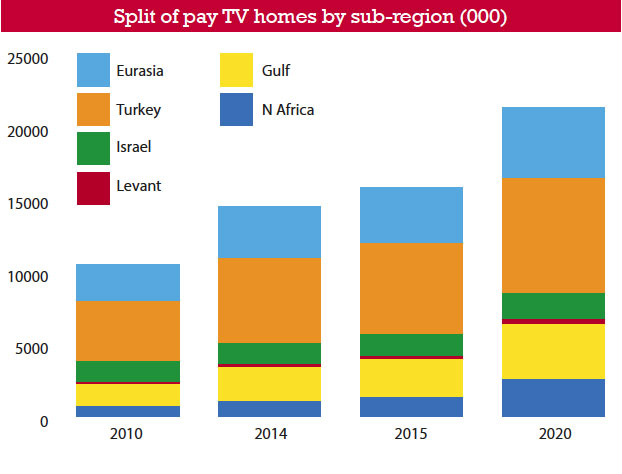

The number of pay TV homes across 20 countries in the Middle East and North Africa region will double between 2010 and 2020 to 21.3 million, with Turkey accounting for 37% of the total. According to the Digital TV Middle East & North Africa report, from the 6.84 million pay TV homes to be added between 2014 and 2020, 2.15 million will come from Turkey and 1.03 million from Egypt.

About 18% of TV households, analogue and digital, legitimately paid for TV signals by 2015. This proportion will climb to 24% by 2020. Qatar will record 72% pay TV penetration by 2020, with Georgia at 50%, Israel 71% and the UAE 52% also high. However, pay TV penetration will remain below 10% of TV households in Algeria, Jordan, Morocco, Syria and Tunisia.

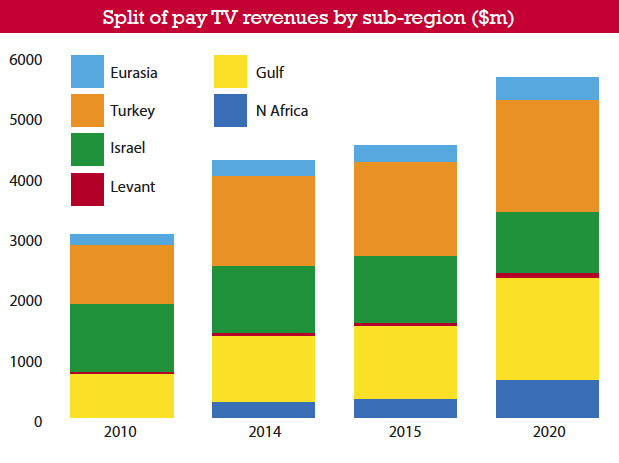

Legitimate pay TV revenues for the 20 countries covered in the Digital TV Middle East & North Africa report will grow by 75% between 2010 and 2020 to US$5.63 billion. Turkey and Israel are expected to contribute 51% of the region’s pay TV revenues in 2020; down from 65% in 2010. This leaves only US$2.77 billion for the remaining 18 countries in 2020, or an average of US$154 million each.

From the US$1.37 billion pay TV revenues to be added between 2014 and 2020, Turkey will supply US$362 million, Egypt US$227 million and Saudi Arabia US$367 million. Revenues in Israel will fall by US$108 million over this period due to greater competition and the conversion of subscribers to bundles, which means lower TV revenues per subscriber.

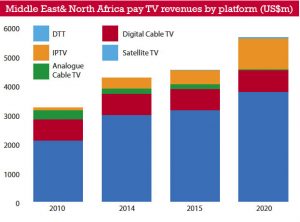

Satellite TV will continue to dominate pay TV revenues, taking two-thirds of the 2020

total, similar to the 2014 proportion. Satellite TV

revenues will be $3.8 billion in 2020, up by US$800 million on 2014 and $1.7 billion on the 2010 total.

Satellite TV will continue to dominate pay TV revenues, taking two-thirds of the 2020

total, similar to the 2014 proportion. Satellite TV

revenues will be $3.8 billion in 2020, up by US$800 million on 2014 and $1.7 billion on the 2010 total.

Turkey will account for US$1.57 billion of the 2020 satellite TV revenues, followed by Saudi Arabia with US$674 million. Saudi Arabia will take second place from Israel in 2015. Satellite TV revenues in Israel will start falling in 2016 as competition forces down ARPU.

Pay satellite TV penetration will climb from 6.9% in 2010 to 11.8% in 2020, with subscriber numbers doubling from 5.01 million to 10.32 million. Penetration in 2020 will reach 27% in Bahrain, 26% in Israel, 23% in Kuwait, 37% in Qatar and 26% in Turkey, but will be less than 5% in a further 10 countries.

About 55% of TV households, 43.35 million, watched free-to-air satellite TV signals by 2015. This proportion is not expected to change too much in coming years, although the number of FTA satellite TV homes will increase to 48.27 million. FTA satellite TV penetration varies considerably among the 20 countries: from 87% in Algeria to 3% in Israel in 2020.

Homes paying for IPTV will overtake cable subscriptions, analogue and digital together, in 2015. There will be 6.16 million IPTV subs in the region by 2020; triple the 2014 total. Turkey will have 1.63 million subscribers, five times as many as 2014, and will be the IPTV subscriber leader in 2020; ahead of Saudi

Arabia with 709,000 subs, Kazakhstan 623,000 and Egypt 737,000. However, Qatar will lead in

penetration terms, with 35%, by 2020, followed by the UAE with 33% and Georgia 24%.

Homes paying for IPTV will overtake cable subscriptions, analogue and digital together, in 2015. There will be 6.16 million IPTV subs in the region by 2020; triple the 2014 total. Turkey will have 1.63 million subscribers, five times as many as 2014, and will be the IPTV subscriber leader in 2020; ahead of Saudi

Arabia with 709,000 subs, Kazakhstan 623,000 and Egypt 737,000. However, Qatar will lead in

penetration terms, with 35%, by 2020, followed by the UAE with 33% and Georgia 24%.

IPTV revenues will grow tenfold between 2010 and 2020 – to $1.07 billion. The UAE will contribute US$233 million of the 2020 total, followed by Saudi Arabia with US$226 million and Turkey US$183 million.

Source: Digital TV Research Ltd

Note: North Africa = Algeria, Egypt, Morocco, Tunisia. Gulf States = Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, UAE. Levant = Jordan, Lebanon, Syria. Eurasia = Armenia, Azerbaijan, Georgia, Kazakhstan, Uzbekistan